Yahoo Finance

Yahoo Finance We're Hopeful That Universal Biosensors (ASX:UBI) Will Use Its Cash Wisely

We can readily understand why investors are attracted to unprofitable companies. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So should Universal Biosensors (ASX:UBI) shareholders be worried about its cash burn? For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

Check out our latest analysis for Universal Biosensors

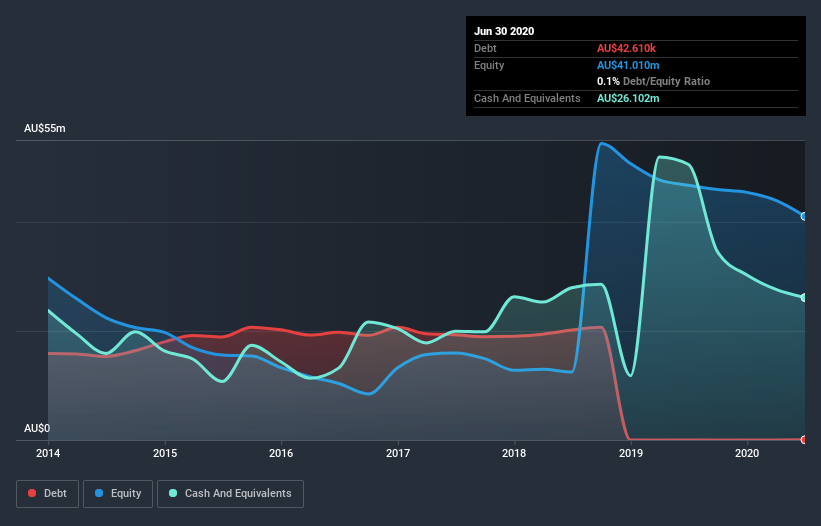

Does Universal Biosensors Have A Long Cash Runway?

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at June 2020, Universal Biosensors had cash of AU$26m and such minimal debt that we can ignore it for the purposes of this analysis. Looking at the last year, the company burnt through AU$10m. That means it had a cash runway of about 2.6 years as of June 2020. Arguably, that's a prudent and sensible length of runway to have. Depicted below, you can see how its cash holdings have changed over time.

Is Universal Biosensors' Revenue Growing?

Given that Universal Biosensors actually had positive free cash flow last year, before burning cash this year, we'll focus on its operating revenue to get a measure of the business trajectory. The bad news for shareholders is that operating revenue actually plummeted 93% in the last year, which is a real concern in our view. Of course, we've only taken a quick look at the stock's growth metrics, here. You can take a look at how Universal Biosensors has developed its business over time by checking this visualization of its revenue and earnings history.

How Hard Would It Be For Universal Biosensors To Raise More Cash For Growth?

Given its problematic fall in revenue, Universal Biosensors shareholders should consider how the company could fund its growth, if it turns out it needs more cash. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Since it has a market capitalisation of AU$55m, Universal Biosensors' AU$10m in cash burn equates to about 18% of its market value. Given that situation, it's fair to say the company wouldn't have much trouble raising more cash for growth, but shareholders would be somewhat diluted.

How Risky Is Universal Biosensors' Cash Burn Situation?

On this analysis of Universal Biosensors' cash burn, we think its cash runway was reassuring, while its falling revenue has us a bit worried. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Universal Biosensors' situation. An in-depth examination of risks revealed 3 warning signs for Universal Biosensors that readers should think about before committing capital to this stock.

Of course Universal Biosensors may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.