Yahoo Finance

Yahoo Finance What's in the Cards for Amarin (AMRN) This Earnings Season?

Amarin Corporation PLC AMRN is likely to report its fourth-quarter 2018 earnings soon.

Amarin’s earnings performance in the last four quarters was dismal, with the company missing estimates twice, meeting the same on one occasion and beating the same on the other,, delivering an average negative surprise of 12.92%.

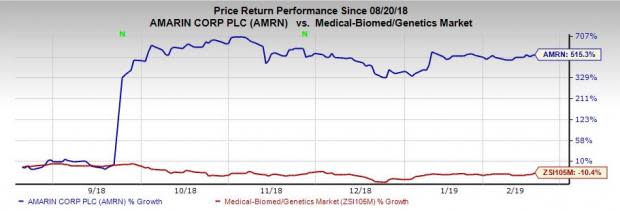

However, shares of Amarin have significantly outperformed the industry in the past six months. The stock has rallied 515.3% against the industry’s decline of 10.4%.

In the last reported quarter, Amarin delivered a positive earnings surprise of 33.33%.

Let’s see how things are shaping up for this announcement.

Factors at Play

Amarin is a pharmaceutical company focused on developing innovating treatments for improving cardiovascular health. The company’s sole marketed drug, Vascepa, is approved as an adjunct to diet to reduce triglyceride levels in severe hypertriglyceridemia patients.

The drug showed strong sales growth in the first three quarters of 2018. Sales grew sequentially in the last two quarters. Normalized prescriptions for the drug grew around 25% year over year in the first nine months of 2018.

Sales of the drug are likely to receive a boost with its approval in the United Arab Emirates in July 2018. Moreover, the settlement of a patent litigation with Teva Pharmaceuticals TEVA in May delayed generic competition for the drug to August 2029.

Last month, the company released preliminary results. Vascepa sales are expected to be in the range of $72-$76 million in the soon-to-be-reported quarter. The Zacks Consensus Estimate for Vascepa sales stands at $74 million for the fourth quarter, suggesting rise of nearly 38% from the year-ago period.

The company also earns fees from its licensed partners related to commercialization of Vascepa outside the United States. The Zacks Consensus Estimate for license revenues stands at $0.4 million for the soon-to-be reported quarter.

In September, Amarin announced top-line data from its cardiovascular outcomes study of Vascepa, REDUCE-IT. Data from the study showed that relative risk of major adverse CV events was reduced by 25% upon treatment with Vascepa compared to placebo. Follow-up data announced in November showed that the drug also met its secondary endpoints with statistical significance and confirmed its potential to achieve cardiovascular benefits.

Operating expenses for the company are likely to remain high in the fourth quarter due to costs related to REDUCE-IT study and initiatives to promote awareness for the drug. Moreover, the company is looking to file label expansion application for the drug to include cardiovascular outcomes study data. The company has expanded its sales force to support the expansion. However, extinguishment of debt is likely lower interest expense for the company.

Investors will primarily focus on the company’s expansion plan for Vascepa commercialization and its label expansion on its fourth-quarter earnings call.

Earnings Whispers

Our proven model does not conclusively show that Amarin is likely to beat estimates this quarter. This is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) to be able to beat estimates. But that is not the case here, as you will see below.

Earnings ESP: Amarin’s Earnings ESP is 0.00%. This is because both the Most Accurate Estimate and the Zacks Consensus Estimate stand at a loss of 5 cents. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: Although Amarin’s Zacks Rank #3 increases the predictive power of ESP, its 0.00% ESP makes surprise prediction difficult.

Note that we caution against stocks with a Zacks Rank #4 or 5 (Sell rated) going into an earnings announcement, especially when the company is seeing negative estimate revisions.

Amarin Corporation PLC Price and EPS Surprise

Amarin Corporation PLC Price and EPS Surprise | Amarin Corporation PLC Quote

Stocks That Warrant a Look

Here are two healthcare stocks that have the right combination of elements to beat on earnings:

Mallinckrodt MNK has an Earnings ESP of +5.36% and a Zacks Rank #2. The company is scheduled to report results on Feb 26. You can see the complete list of today’s Zacks #1 Rank stocks here.

BioDelivery Sciences International, Inc. BDSI has an Earnings ESP of +38.46% and a Zacks Rank #1.

The Hottest Tech Mega-Trend of All

Last year, it generated $8 billion in global revenues. By 2020, it's predicted to blast through the roof to $47 billion. Famed investor Mark Cuban says it will produce "the world's first trillionaires," but that should still leave plenty of money for regular investors who make the right trades early.

See Zacks' 3 Best Stocks to Play This Trend >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BioDelivery Sciences International, Inc. (BDSI) : Free Stock Analysis Report

Amarin Corporation PLC (AMRN) : Free Stock Analysis Report

Mallinckrodt public limited company (MNK) : Free Stock Analysis Report

Teva Pharmaceutical Industries Ltd. (TEVA) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research