Yahoo Finance

Yahoo Finance While shareholders of Altice USA (NYSE:ATUS) are in the red over the last year, underlying earnings have actually grown

Even the best stock pickers will make plenty of bad investments. And unfortunately for Altice USA, Inc. (NYSE:ATUS) shareholders, the stock is a lot lower today than it was a year ago. In that relatively short period, the share price has plunged 56%. At least the damage isn't so bad if you look at the last three years, since the stock is down 2.7% in that time. Furthermore, it's down 17% in about a quarter. That's not much fun for holders.

The recent uptick of 5.7% could be a positive sign of things to come, so let's take a lot at historical fundamentals.

Check out our latest analysis for Altice USA

To quote Buffett, 'Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace...' One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

The last year saw Altice USA's EPS really take off. We don't think the growth guide to the sustainable growth rate in this case, but we do think this sort of increase is impressive. As you can imagine, the share price action therefore perturbs us. Some different data might shed some more light on the situation.

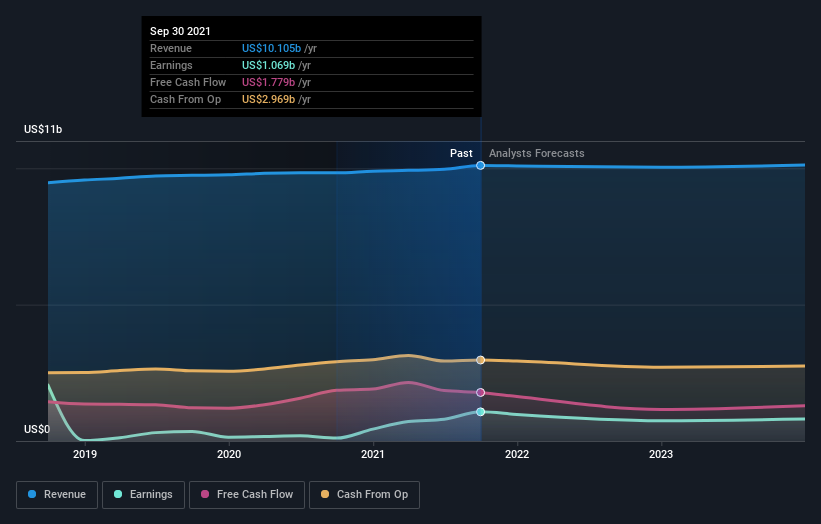

Revenue was fairly steady year on year, which isn't usually such a bad thing. But the share price might be lower because the market expected a meaningful improvement, and got none.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

It's probably worth noting we've seen significant insider buying in the last quarter, which we consider a positive. On the other hand, we think the revenue and earnings trends are much more meaningful measures of the business. This free report showing analyst forecasts should help you form a view on Altice USA

A Different Perspective

The last twelve months weren't great for Altice USA shares, which cost holders 56%, while the market was up about 22%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. The three-year loss of 0.9% per year isn't as bad as the last twelve months, suggesting that the company has not been able to convince the market it has solved its problems. Although Baron Rothschild famously said to "buy when there's blood in the streets, even if the blood is your own", he also focusses on high quality stocks with solid prospects. It's always interesting to track share price performance over the longer term. But to understand Altice USA better, we need to consider many other factors. Case in point: We've spotted 3 warning signs for Altice USA you should be aware of, and 2 of them are a bit concerning.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.