Yahoo Finance

Yahoo Finance Why You Should Retain Arthur J. Gallagher in Your Portfolio

Estimates for Arthur J. Gallagher & Co. AJG have been revised upward over the past 60 days, reflecting analysts’ confidence in the stock. The stock has seen the Zacks Consensus Estimate for 2018 and 2019 earnings being raised 0.3% each to $3.46 and $3.85, respectively.

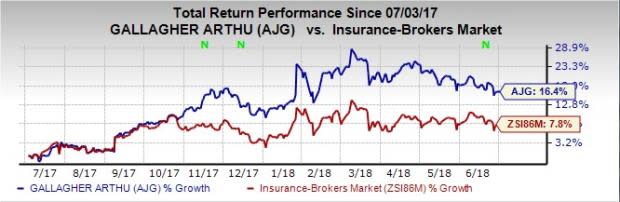

The company provides insurance brokerage, consulting and third party claims settlement plus administration services. Shares of this Zacks Rank #3 (Hold) insurance broker have rallied 16.4% in a year against the industry’s 7.8% increase.

Let’s focus on the factors that make Torchmark a stock to retain for attractive returns.

Improving Top Line: Arthur J. Gallagher has been continuously generating an improved top line. Its revenues witnessed a five-year CAGR of 9%, driven by organic sales as well as acquisition and mergers. Sustained improved performance at its Brokerage segment should continue to drive top line. The company estimates segment performance in 2018 to improve from 2017 level.

Compelling Acquisitions: Arthur J. Gallagher evolved from a small retail presence in Australia, Canada and New Zealand to one of the top five brokers, globally. Its strategic buyouts have helped the company expand footprints besides adding capabilities to its existing portfolio. Arthur J. Gallagher has put the steam behind its acquisition activity in the retail employee benefits brokerage as well as wholesale brokerage areas. The company’s merger and acquisition pipeline remains strong with about $400 million of revenues.

Geographical Expansion: Arthur J. Gallagher derives 25% of its revenues from international operations. Given the number and size of the non-U.S. transactions, the company has been pursuing, it expects international contribution to drive its total revenue base. Moreover, loss of clients or weakening of macro conditions in any particular country should not have any severe impact on the top line.

Effective Capital Management: Arthur J. Gallagher enjoys a solid cash flow, helping it prudently deploy capital. While the company’s dividend payouts witnessed a three year CAGR of 3.5%, its dividend yield of 2.5% betters the industry average of 1.3%. The company also has 7.3 million shares remaining under its repurchase authorization. These make the stock a profitable pick for yield-seeking investors.

Growth Projections: The Zacks Consensus Estimate for current-year earnings per share is pegged at $3.46, representing a year-over-year increase of 13.1% on 8.2% higher revenues of $6.7 billion. For 2019, the consensus mark for the bottom line stands at $3.85, translating into an 11.4% year-over-year rise while the same for the top line is projected at $7.2 billion, up 7.3%.

Arthur J. Gallagher has expected long-term earnings per share growth of 10.3%.

Positive Earnings Surprise History: The company boasts a solid earnings surprise history, exceeding the Zacks Consensus Estimate in the last five quarters. This outperformance underlines the company’s operational efficiency. Its average five-quarter positive earnings surprise stands at 3.48%.

Stocks to Consider

Some better-ranked stocks from the insurance industry are Aon Plc AON, Brown & Brown, Inc. BRO and Alleghany Corporation Y.

Aon provides risk management services, insurance and reinsurance brokerage plus human resource consulting and outsourcing services worldwide. It pulled off an average four-quarter positive surprise of 2.11%. The stock carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Brown & Brown, Inc. markets and sells insurance products in the United States, England, Canada, Bermuda and the Cayman Islands. The company came up with an average four-quarter beat of 9.35%. The stock holds a Zacks Rank of 2.

Alleghany provides property and casualty reinsurance and insurance products in the United States and internationally. It delivered an average four-quarter earnings surprise of 17.61%. The stock sports a Zacks Rank #1.

Today's Stocks from Zacks' Hottest Strategies

It's hard to believe, even for us at Zacks. But while the market gained +21.9% in 2017, our top stock-picking screens have returned +115.0%, +109.3%, +104.9%, +98.6%, and +67.1%.

And this outperformance has not just been a recent phenomenon. Over the years it has been remarkably consistent. From 2000 - 2017, the composite yearly average gain for these strategies has beaten the market more than 19X over. Maybe even more remarkable is the fact that we're willing to share their latest stocks with you without cost or obligation.

See Them Free>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Aon plc (AON) : Free Stock Analysis Report

Brown & Brown, Inc. (BRO) : Free Stock Analysis Report

Arthur J. Gallagher & Co. (AJG) : Free Stock Analysis Report

Alleghany Corporation (Y) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research