Yahoo Finance

Yahoo Finance Wireless Non-US Stock Outlook: High Costs Make Headwinds

The global wireless telecommunications ecosystem has witnessed considerable growth recently due to rapid technological advancements, evolving consumers’ need and increasing smart device usage to access real-time data. Wireless carriers across national territories have expanded their service portfolios to include a wide array of offerings to capitalize on growth opportunities across technology, media and telecommunications in areas such as enterprise cloud, TV, Internet of Things, augmented and virtual reality, and autonomous vehicles among others.

However, a decisive challenge for wireless operators as they expand service portfolios is that adjacent market segments tend to offer lower margins, and disruptive competitors are well-positioned in key segments such as cloud and advertising.

Broad-based industry growth is expected over the next five years as carriers complete 5G superfast network rollouts and benefit from the booming demand for data services. The majority of wireless subscription addition have stemmed from emerging markets, particularly India, China, Japan and Africa.

Markets in developed economies have mostly reached saturation levels, preventing wireless carriers from achieving the subscriber growth rates of their counterparts in emerging economies and leading them to focus on increasing average revenue per user (ARPU). The countries in Latin America such as Brazil, Mexico and Argentina are also slated to offer significant opportunities as the degree of penetration of high-speed broadband, 4G services and the usage of smartphones rise.

Geographically, the wireless telecommunication services market is divided into seven key regions — North America, Latin America, Eastern Europe, Western Europe, Japan, Asia-Pacific excluding Japan, and the Middle East & Africa. North America holds the largest revenue share in the market followed by Europe and Asia Pacific owing to major technology providers based in these regions, and easy adoption of these technologies by the population.

Japan, Middle East and Africa, and Latin America hold significant potential for growth in the market, raising demand for wireless telecommunication services. However, high capital expenditure to extend network infrastructure for mobile connectivity and cut-throat competition is forcing down prices, leading to aggregate lower ARPU for telcos.

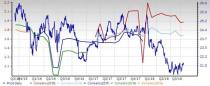

Industry Underperforms S&P 500, Sector

Looking at shareholders’ return over the past year, it appears that wireless carriers have been beleaguered by the churn rate in the face of dwindling voice- and text-revenues, resulting in overall decline in ARPU, market saturation, heavy CAPEX and the disruptive rise of the OTT service providers in this competitive and dynamic industry.

The Zacks Wireless Non-US Industry, which is a 15-stock group within the broader Zacks Computer and Technology Sector, has grossly underperformed both the S&P 500 and its own sector over the past year.

While the stocks in this industry have collectively lost 10.4%, the Zacks S&P 500 Composite and Zacks Computer and Technology Sector have rallied 17.8% and 19.5%, respectively.

One-Year Price Performance

However, it’s worth noting that 4G LTE deployment and network upgrades are the key trend around the world at present, and in select markets there is also massive investment in fixed broadband based on fiber. 5G developments have gained pace and will continue to be a key area of focus in 2018 and beyond.

Wireless Non-US Stocks Trading Cheap

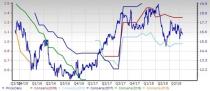

Thanks to the underperformance of the industry over the past year, the valuation picture looks moderately economical. One might get a good sense of the industry’s relative valuation by looking at its Enterprise Value-to-EBITDA ratio (EV/EBITDA), which is the most appropriate multiple for valuing non-US wireless stocks.

Wireless service providers operate in a heavy capital-intensive industry, incurring significantly high capital investments for technologically obsolescent offerings and high R&D expenses. The entities face high depreciation charges due to large fixed asset base. The EV/EBITDA ratio essentially measures the value of a company, inclusive of debt and other liabilities, to the actual cash earnings exclusive of the non-cash expenses.

The industry currently has a trailing 12-month EV/EBITDA of 10.9X, which is below the 12-month median of 18.4X. Over the past year, the industry has traded as high as 19.5X and as low as 10.9X.

The S&P 500 Index is currently trading at 12X trailing 12-month EV/EBITDA with a high, low and median over the past year of 12.7X, 10.7X, and 11.6X, respectively.

Enterprise Value/EBITDA Ratio (TTM)

Comparing the group’s EV/EBITDA ratio with that of its broader sector also shows that the group is trading at a discount. The Computer and Technology Sector’s trailing 12-month EV/EBITDA ratio of 11.2 is above the Zacks Wireless Non-US Industry’s ratio.

Enterprise Value/EBITDA Ratio (TTM)

Underperformance May Continue Due to Bleak Earnings Outlook

In 2018, the global wireless telecommunications market will continue its transformation on account of the digital, sharing and interconnected economy. This radical evolution is primarily driven by the ongoing innovations and technological developments that are taking place, and the industry is working hard to keep up with these rapid changes.

But what really matters to investors is whether this group has the potential to perform better than the broader market in the quarters ahead. A reliable measure that can help investors understand the industry’s prospects for a solid price performance is the earnings outlook for its member companies. Empirical research shows that a company’s earnings outlook significantly influences the performance of its stock.

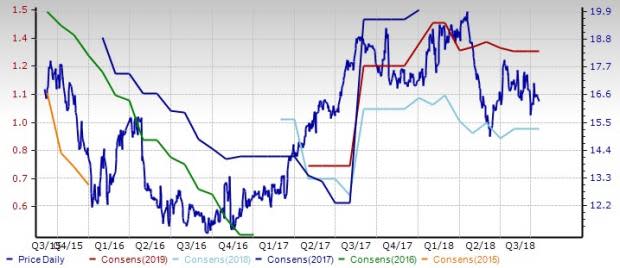

One could get a good sense of a company’s earnings outlook by comparing the consensus earnings expectation for the current financial year with last year’s reported number but an effective measure could be the magnitude and direction of the recent change in earnings estimates.

While the light blue line in the chart below shows the evolution of aggregate 2018 earnings estimates for operators in this space, the red line represents 2019 expectations.

The consensus estimate for 2018 for the Zacks Wireless Non-US Industry of $1.65 per share implies a year-over-year decline of 6.3% as the trend in earnings estimate revisions continues to remain unattractive.

Price and Consensus: Zacks Wireless Non-US Industry

Looking at the aggregate earnings estimate revisions, it appears that analysts are losing confidence in this group’s earnings potential.

The consensus EPS estimate for the current fiscal has been revised 8.3% downward since Feb 28, 2018.

Current Fiscal Year EPS Estimate Revisions

Zacks Industry Rank Indicates Gloomy Prospects

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates continued underperformance in the near term.

The Zacks Wireless Non-US industry currently carries a Zacks Industry Rank #207, which places it at the bottom 19% of more than 250 Zacks industries. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

Non-US Wireless Carriers Portray Decent Long-Term Growth

While the near-term prospects look unwelcoming for investors, the long-term (3-5 years) EPS growth estimate for the Zacks Wireless Non-US industry appears to be relatively promising. The group’s mean estimate of long-term EPS growth rate has maintained nearly a flat trajectory since April 2018 to reach the current level of 13.3%. This compares to 9.8% for the Zacks S&P 500 Composite.

Mean Estimate of Long-Term EPS Growth Rate

In fact, the basis of this attractive long-terms EPS could be the recovery in trailing 12-month gross margin that non-US wireless carriers have been showing since the beginning of 2016.

Another important indication of moderate long-term growth prospects is the improvement in the group’s GAAP net income since the beginning of 2017.

Bottom Line

Moving ahead, the industry is likely to benefit from healthy growth dynamics supported by improving macroeconomic environment, technological innovations and rise in consumers’ disposable income.

This apart, the vast population base of multiple countries, particularly China, India and Japan, coupled with rapid proliferation of smart devices and Internet users will be the key factor responsible for the growth of the telecommunication market worldwide. However, price-sensitive competition for customer retention in core business will likely become more intense in coming days.

The industry might not be able to tide over the broader challenges in the near term. Hence, it may not be a good idea to bet on this space right now. However, keeping the long-term expectations in mind, investors could take advantage of the cheap valuation and bet on a few non-US wireless stocks that have a moderate earnings outlook.

While none of the stocks in our non-US wireless universe currently sport a Zacks Rank #1 (Strong Buy), below is one stock that has been witnessing positive earnings estimate revisions and currently carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Orange S.A. (ORAN): This Paris, France-based wireless carrier has gained 6.1% over the past two years. The Zacks Consensus Estimate for the current-year EPS has been revised 1% upward over the past 90 days.

Price and Consensus: ORAN

Investors may also hold on to the following three stocks currently having a Zacks Rank #3 (Hold).

América Móvil, S.A.B. de C.V. (AMX): The stock of this Mexico-based wireless carrier has gained 45.5% over the past two years. The Zacks Consensus Estimate for the current-year EPS has been revised 4.4% upward over the past 90 days.

Price and Consensus: AMX

BlackBerry Limited (BB): The consensus EPS estimate for this Waterloo, Canada-based wireless carrier has remained flat for the current fiscal year, over the past 90 days. The stock has rallied 14% over the past year.

Price and Consensus: BB

China Mobile Limited (CHL): The stock of this Central, Hong Kong-based wireless carrier has gained 6.5% over the past six months. The Zacks Consensus Estimate for the current-year EPS has remained flat over the past 30 days.

Price and Consensus: CHL

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2020.

Click here for the 6 trades >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Orange (ORAN) : Free Stock Analysis Report

China Mobile (Hong Kong) Ltd. (CHL) : Free Stock Analysis Report

BlackBerry Limited (BB) : Free Stock Analysis Report

America Movil, S.A.B. de C.V. (AMX) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research