Yahoo Finance

Yahoo Finance ZoomerMedia (CVE:ZUM) Seems To Use Debt Quite Sensibly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that ZoomerMedia Limited (CVE:ZUM) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for ZoomerMedia

What Is ZoomerMedia's Debt?

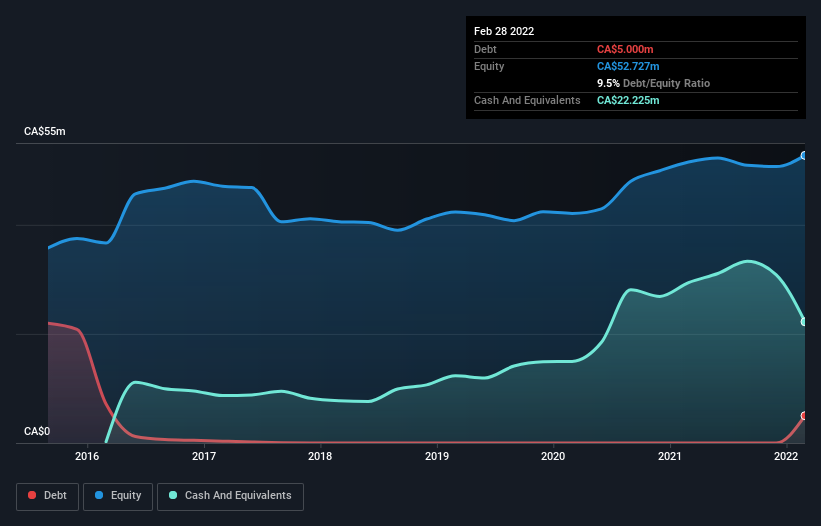

You can click the graphic below for the historical numbers, but it shows that as of February 2022 ZoomerMedia had CA$5.00m of debt, an increase on none, over one year. However, its balance sheet shows it holds CA$22.2m in cash, so it actually has CA$17.2m net cash.

How Strong Is ZoomerMedia's Balance Sheet?

We can see from the most recent balance sheet that ZoomerMedia had liabilities of CA$11.6m falling due within a year, and liabilities of CA$27.2m due beyond that. Offsetting this, it had CA$22.2m in cash and CA$10.0m in receivables that were due within 12 months. So it has liabilities totalling CA$6.54m more than its cash and near-term receivables, combined.

Given ZoomerMedia has a market capitalization of CA$52.9m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, ZoomerMedia also has more cash than debt, so we're pretty confident it can manage its debt safely.

Importantly, ZoomerMedia's EBIT fell a jaw-dropping 38% in the last twelve months. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. There's no doubt that we learn most about debt from the balance sheet. But it is ZoomerMedia's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. ZoomerMedia may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, ZoomerMedia actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While ZoomerMedia does have more liabilities than liquid assets, it also has net cash of CA$17.2m. The cherry on top was that in converted 134% of that EBIT to free cash flow, bringing in CA$6.9m. So we don't have any problem with ZoomerMedia's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example - ZoomerMedia has 5 warning signs we think you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.