Yahoo Finance

Yahoo Finance Is Bill Ackman's Chipotle Sale Cause for Concern?

Pershing Square Capital Management, the investment firm run by investing guru Bill Ackman (Trades, Portfolio), trimmed its stake in Chipotle Mexican Grill Inc. (NYSE:CMG) by nearly 10% during the first quarter of 2024. However, the restaurant chain remains the firm's largest holding at just over 20% of its total portfolio.

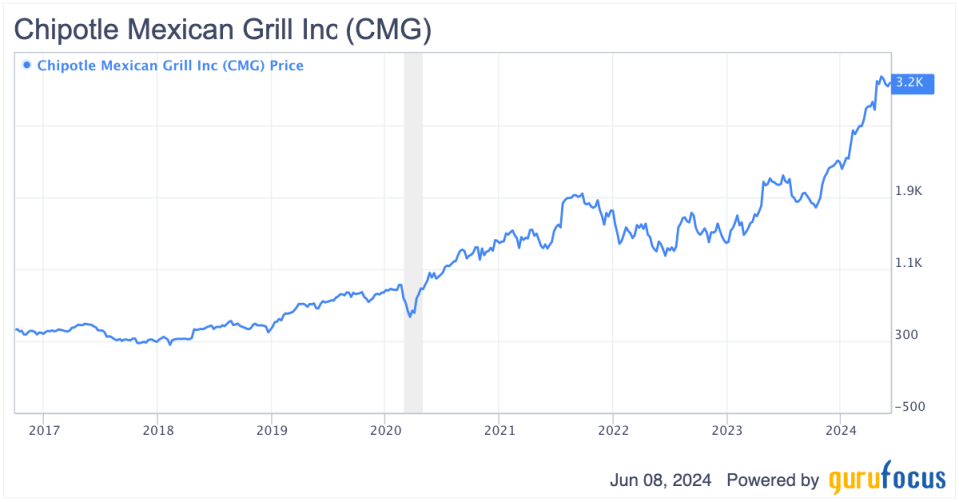

Chipotle has been a longtime favorite of Ackman as the firm made its initial investment in late 2016. Since then, shares have delivered a total return of roughly 620%. Comparably, the S&P 500 has delivered a total return of roughly 180% over the same period. Thus, on a relative basis, Chipotle has proven to be an excellent investment.

The stock's return has been driven by strong earnings growth and multiple expansion. Over the past five years, the company has grown earnings per share at a compound annual rate of nearly 16%.

CMG Data by GuruFocus

Potential reasons why Ackman reduced his position

While it is difficult to know for sure what prompted Ackman to sell Chipotle shares, one potential reason is diversification. In early 2020, he sold Chipotle shares for diversification reasons. He said:

"What started out as a large position recently became a massive one, in excess of 20% of capital... We sold stock earlier this week only for portfolio management reasons."

Chipotle shares are currently up nearly 40% on a year-to-date basis and the stock has once again become a very large part of Pershing Square's portfolio. Thus, selling for diversification purposes is reasonable. Moreover, Ackman recently announced the firm had sold a 10% interest to a group of investors. The move is considered a precursor to a potential initial public offering down the road. Given Pershing Square's strong track record over the past several years, it would seem reasonable that Ackman may want to pursue a more diversified, lower-risk portfolio as he continues to work toward a potential IPO of Pershing Square.

Another reason why Ackman may have decided to sell is that he has lost conviction in the stock and no longer views it as an attractive investment. However, I view this as unlikely given his comments in the 2023 Pershing Square annual letter regarding his long-term view of the business:

We believe Chipotle is in the early innings of a decades-long growth story. In North America, management expects to grow its restaurant count at a rate of 8% to 10% per annum, with the goal of more than doubling its store base to at least 7,000 locations. International expansion remains a largely untapped opportunity, with the company just beginning to increase investment in Europe and recently announcing its first-ever franchise agreement in the Middle East. In addition to opening new restaurants, Chipotle's many growth opportunities in existing restaurants include menu innovations, loyalty program enhancements, and the long-term potential to offer breakfast and leverage automation technology to simplify operations."

Valuation is not inconsistent with historical norms

Historically, Chipotle has almost always been a high valuation stock. Over the past five years, shares have traded at an average trailing price-earnings ratio of roughly 77. Currently, the stock trades at roughly 67 times trailing 12-month earnings per share and roughly 57 times 2024 consensus earnings per share.

Peers such as McDonalds (NYSE:MCD), Restaurant Brands International (NYSE:QSR) and Yum Brands (NYSE:YUM) trade at forward price-earnings ratios of roughly 21, 20 and 24.60. At first glance, Chipotle appears overvalued relative to these companies. However, its valuation is more reasonable when consider its faster growth potential. For this reason, historically Chipotle has tended to trade at a significant valuation premium to its peer group and the current valuation premium is reasonable compared to historical norms.

Chipotle is expected to grow full-year 2024, 2025 and 2026 earnings per share at annual rates of 24%, 20% and 18.4%. Comparably, McDonalds, Restaurant Brands International and Yum Brands are expected to grow annual earnings at high single-digit to low double-digit rates.

In addition to have better near-term growth potential, Chipotle also has a longer growth runway than these peers as its global restaurant count is much lower. Currently, Chipotle owns and operates approximately 3,479 restaurants primarily in the U.S. Comparably, McDonald's has over 40,000 locations worldwide, while Restaurant Brands International and Yum Brands have more than 30,000 and 58,000 locations worldwide. Due to this significant difference, I tend to agree with Ackman's view that the Chipotle growth story remains in the early innings.

What could go wrong for the bulls?

The biggest risk to the bull case is the Chipotle dining experience becomes less attractive to consumers compared to other fast-casual dining options. The fast-casual dining market is highly competitive and new players are always entering the market. Key competitors include Taco Bell, Qdoba Mexican Eats and Moe's Southwest Grill. The Chipotle dining experience could become less attractive versus peers if the company fails to continue to innovate in regards to its offerings or if prices become too high versus comparable offerings.

Chipotle has increased prices six times since 2021. While the company's pricing power is somewhat limited due to a highly competitive operating environment, its customer base tends to skew more toward higher-income consumers compared to peers. For example, roughly 34% of Chipotle consumers earn more than $125,000 per year compared to just 26% for Taco Bell.

Another key risk to the Chipotle bull case is that is unable to replicate its success internationally. Currently, the company operates roughly 66 locations internationally, but has plans to expand aggressively. International expansion can often be challenging for U.S.-based companies due to cultural differences and differences in consumer preferences. That said, the company has suggested its international growth plans will rely heavily on joint ventures and local franchisees, which should help mitigate these risks. In 2023, Chipotle announced an agreement with Alshaya Group to open restaurants in the Middle East.

Ackman Chipotle share sales are not cause for concern

Ackman's Pershing Square sold shares of Chipotle following a massive rally in the stock. While Ackman is a highly successful investor, I do not view his recent sale as cause for concern.

While it is difficult to know for sure why he decided to reduce Pershing Square's position in the stock, I believe diversification is likely the reason.

I would not be surprised to see Ackman continue to trim the position, especially in the event the stock rallies further from here, but do not believe he will fully liquidate given his view that the Chipotle growth story remains in the early innings.

Chipotle shares currently trade at a high valuation and at a premium to peers. However, the company has strong near-term and long-term growth prospects. The stock's valuation is reasonable relative to historical norms and thus, I do not find the stock overvalued at current levels.

This article first appeared on GuruFocus.