Yahoo Finance

Yahoo Finance Buffett and Bondholders Are Now Oxy’s Priorities

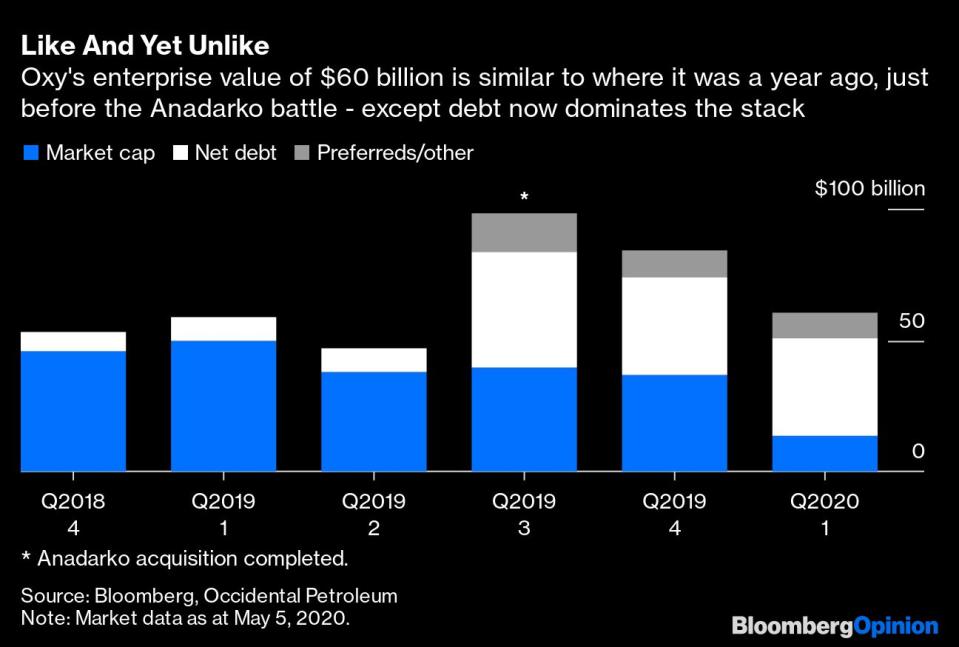

(Bloomberg Opinion) -- A lot has happened since May 5, 2019. That was a busy day for Occidental Petroleum Corp. First, it announced a deal worth almost $9 billion to sell a package of African assets to Total SA, on the proviso that Oxy gained control of Anadarko Petroleum Corp. (which owned said assets). Then Oxy raised its offer for Anadarko, using the $10 billion raised by selling preferred stock to Berkshire Hathaway Inc. in a hurried negotiation with Warren Buffett. The higher bid, together with the fact that Buffett’s money allowed Oxy to sidestep a vote of its own shareholders, clinched it.

On May 5, 2020, Oxy reported a quarterly loss of $2.2 billion and withdrew annual guidance. Also, news emerged it had hired a bank to help cut its debt load, as reported by The Wall Street Journal. Meanwhile, Total, hosting its own earnings call that day, indicated completion of the Algerian and Ghanaian parts of that African deal was not exactly imminent. On Wednesday, Oxy’s 10-Q filing confirmed the Algerian deal is effectively dead and the Ghanaian one in limbo. Like I said, a lot’s happened.

M&A is all about the income statement; how cost savings mean 1+1=3 for the bottom line. But off-stage, the balance sheet is doing the heavy lifting. Oxy’s experience of the past 12 months is destined to be a case study in what happens when the balance sheet gets stressed and ends up having a meltdown on center stage.

Oxy took a risk with Anadarko, and Covid-19 is its unforeseen nemesis. Hence, Oxy is pulling every lever to conserve cash. Dividends to common shareholders have been slashed by 86%. Buffett’s $200 million-per-quarter coupon is being paid in new shares rather than cash. Now the capital expenditure budget has been cut, again, to less than half what was laid out three months ago. Further cost savings are promised.

Altogether, it may be enough to keep Oxy’s balance sheet running in place but not to lose weight anytime soon. Adding the incremental savings to existing consensus estimates(2) implies Ebitda (as a proxy for cash flow) of roughly $4 billion through the rest of the year. Interest, dividends and capex take about $2.6 billion of that (assuming Buffett keeps getting new stock every quarter). The resulting free cash flow helps, but would still imply Oxy ending the year with leverage above 5 times Ebitda, or about 6.5 times with the preferreds. On Wednesday’s call, Oxy mentioned $2 billion of potential disposals in the near future. If they happen this year, they would take those multiples down slightly. Even a utility would feel uncomfortable with those numbers — and an oil company in the middle of a pandemic is no utility(3).

One option for those hired bankers to consider is capitalizing on the bond sell-off by persuading Oxy’s creditors to swap their unsecured paper below face value for secured bonds. Charles Johnston of CreditSights, an analytics firm, estimates a $10 billion exchange at 65 cents on the dollar could shrink the pile by $5 billion, taking leverage to about 4.4 times at year-end (based on my numbers above)(1). That would still be very high but an improvement, especially if some semblance of stability entered the oil market later this year.

There’s a catch, though. Creditors being asked to take a haircut to par value might look at Oxy’s current market cap of almost $13 billion and wonder why more of the pain shouldn’t fall on equity holders. As it is, CreditSights estimates asset coverage for Oxy’s creditors of just over $51 billion under a “high-case” scenario — implying residual equity value of less than $5 billion.

This is why, despite Oxy’s progress on cutting costs, the sheer size of the balance sheet makes its stock — and lately its bonds — options on oil-price recovery. Even before Covid-19’s arrival, that was not a hot ticket among energy investors, who have realized the oil option often doesn’t pay off for them. Now, with Oxy’s maturities wall looming, potentially tough negotiations with creditors beckon amid a fragile oil market. The world has changed a lot for oil producers this past year, but for Oxy more than most. The next 12 months don’t promise much respite.

(1) Clearly, these are very much subject to change given volatileoil prices and Oxy's suspension of guidance.

(2) In terms of liquidity, Oxy also faces a wildcard in the form of 2036 bonds that are putable to the company in October. This may require almost$1 billion of refinancing depending on what bondholders decide to do..

(3) Adding in preferreds, it would drop from 6.5 times to 5.8 times. Assuming $2 billion of disposal proceeds would take the implied multiples down to 4.1 without preferreds and 5.5 times all in, using my numbers.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

For more articles like this, please visit us at bloomberg.com/opinion

Subscribe now to stay ahead with the most trusted business news source.

©2020 Bloomberg L.P.