Yahoo Finance

Yahoo Finance How a DCF Analysis Validates Crocs' Value Thesis

Shares of Crocs Inc. (NASDAQ:CROX) have made an interesting comeback in recent months, especially after the release of better-than-expected first-quarter earnings. The shares were trading at $180 at the end of 2021, but after the acquisition of HeyDude, the market became fearful, with the shares having accumulated just over a 70% drop by mid-2022.

It turns out that since then, the company has done an excellent job of continuing to grow its flagship brand, generate strong cash flow and maintain an interesting capital allocation. Despite this, HeyDude's plans continue to present challenges.

Even with relatively high debt and nebulous short-term growth, Crocs shares are trading at an attractive level, both when looking at multiples and a conservative discounted cash flow analysis. This attractive level is in line with its moat, which has been able to build a strong brand and deliver good financial indicators.

Moats and prospects

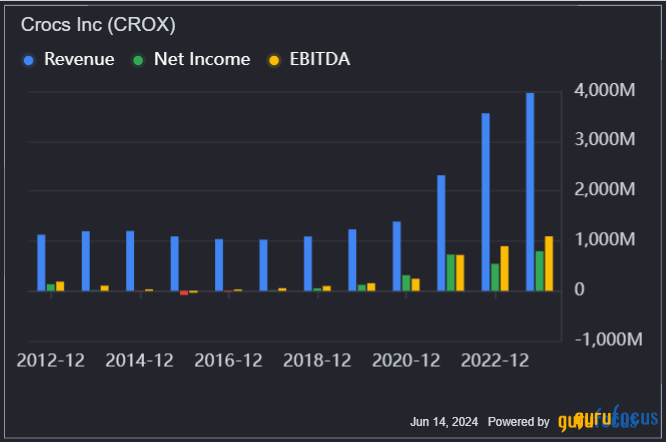

Despite the challenges on the short-term horizon, Crocs has a recent history of very interesting results. Its net revenue was around $1.2 billion in 2019 and in the last 12 months, it has surpassed the $4 billion mark, a growth that mixes the acquisition of HeyDude (which of this amount, represents something close to $900 million) with very strong growth of the main brand, a compound annual rate of more than 20% between 2017 and 2023.

As you can see from the graph above, the company has not always been able to generate value. From 2012 to 2019, its revenue was practically stagnant and, on several occasions, reaching a margin far below what is seen today, including a negative Ebitda margin in mid-2015. This means that even though the company has maintained an Ebitda margin of around 30% over the last three years, the average over the last decade has fallen to 14%, a factor that weighs heavily on financial modeling and confidence in the company's future.

Looking at the company now, profitability is a major factor. Not surprisingly, Crocs has an 8 out of 10 profitability rank with a very good gross margin, which highlights its brand power even in a competitive market, as well as very strong operating and net margins compared to the industry.

Source: GuruFocus

This margin (mainly gross) is due to the added value that Crocs managed to add to its products since, even with a less complex production process, it manages to sell at interesting prices by creating brand awareness and using strategies such as partnerships with famous brands, creating products such as Crocs Toy Story, Crocs NBA and others. Not only that, but there is a strong demand for clog products among consumers, with the casual trend driving them, along with cultural movements that are also proving to be strong and are evidenced by the strong growth that the brand is having in China (triple-digit growth last quarter).

Thus, the triggers for maintaining Crocs' growth are not so clear. There is work being done on the execution of the brand, as well as it being a utilitarian shoe, widely used by some sectors such as health care, but on the other hand, in parts, this growth may depend on fashion trends and other factors. This is one of the reasons why the acquisition of HeyDude is not all bad, since it ends up mitigating this risk by diversifying into another strong brand.

As for HeyDude, the guidance for the next few quarters is still weak, with revenue expected to fall between 19% and 17% in the second quarter and close to 10% to 8% in 2024, with strategies to maintain the price in digital and improve inventories. In addition, there are still some synergies that can be captured, such as entering some international markets by taking advantage of Crocs' distribution channels.

Crocs has value in a DCF analysis, but the margin of safety is not that high

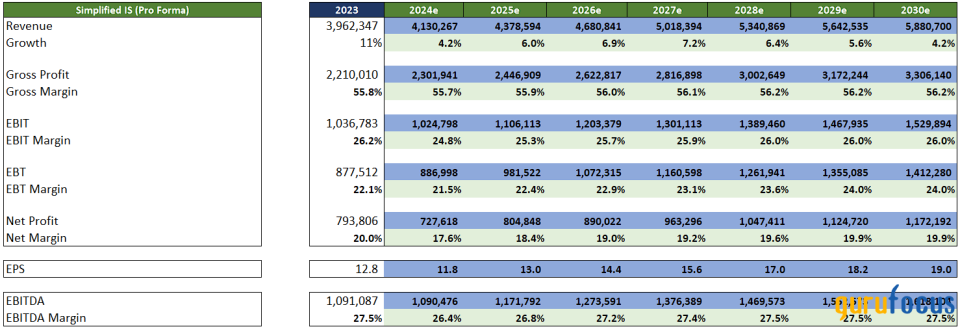

Based on this information, it would not be plausible to perpetuate aggressive growth for Crocs. Even if it were possible for the company to maintain double-digit growth in revenue and return Ebitda margins back to 30%, making such assumptions would be unreasonable and would reduce the margin of safety. That's why in my model I applied realistic data and that the company should not have too many challenges to execute.

In line with the guidance, in my model I find revenue of $4.13 billion for 2024, the result of a decline in HeyDude of around 11%, offset by an increase of 9% in revenue from the main brand (per year). In addition, the Ebit margin is slightly below guidance, causing earnings per share to also fall short of what the company indicated last quarter.

In terms of evolution, I project a gradual upturn for the HeyDude brand, along with lower growth for Crocs over the next several years, ranging from 4% to 7% from 2025 to 2030. Meanwhile, margins are reaching very manageable levels. For example, the perpetuation of 26% Ebit margin after 2028 and a 24% margin after 2029.

Not only that, but the effective tax rate is also at slightly higher than historical levels, returning to 17% in 2026. This means the model takes into account a net income margin of 19.90% in perpetuity, a level that the company has already reached in the past and shouldn't have too many problems reaching again if the initiatives are successful.

Source: Author

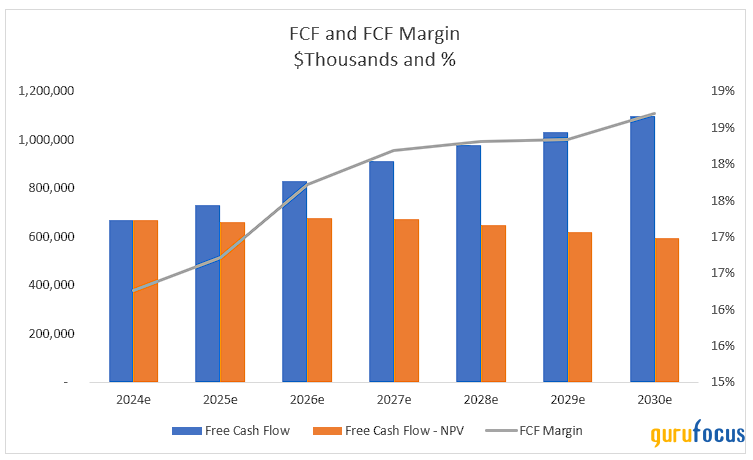

In addition to these income statement assumptions, the model takes into account other assumptions, such as capital expenditures of -3% of revenue until 2029, falling to -2.5% from 2030 onwards, a stagnant depreciation of 1.50% of revenue as well as a perpetuation of the variation in working capital. Thus, there is a good evolution for free cash flow, with the margin reaching 19% in 2030 and an amount above $1 billion.

Source: Author

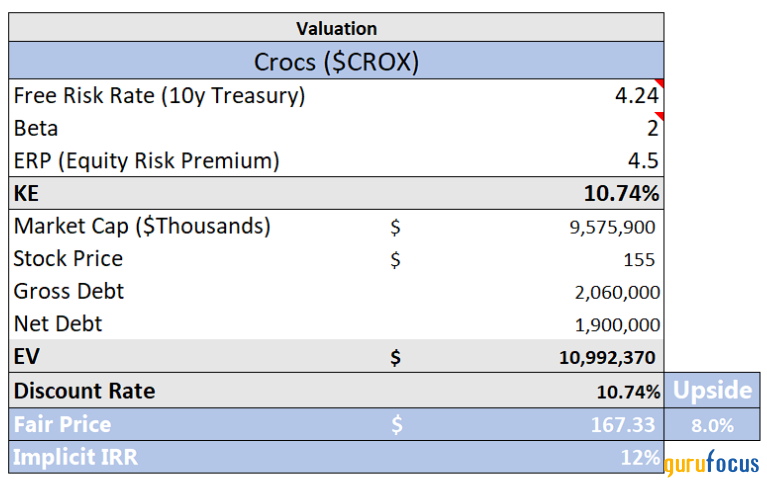

Note that bringing this cash flow to present value, the amount decreases significantly since the discount rate used is 10.74%, reflecting the 10-year Treasury of 4.24% and an equity risk premium of 4.50% (in addition to beta). The result of this account is a fair price of $167 for Crocs, resulting in an upside of 8% in relation to the current price. The internal rate of return implicit in this modeling is roughly 12%.

Source: Author

Compared to other value plays, this upside may seem low, but the assumptions are conservative (and the discount rate as well), slightly below the guidance for 2024, and with modest growth. Therefore, this ends up adding a greater possibility of positive surprises (or upside risk) that are not being represented in a conservative model, as may be the case with continued growth in the international segment, the renewal of HeyDude and efficiencies that can further increase margins.

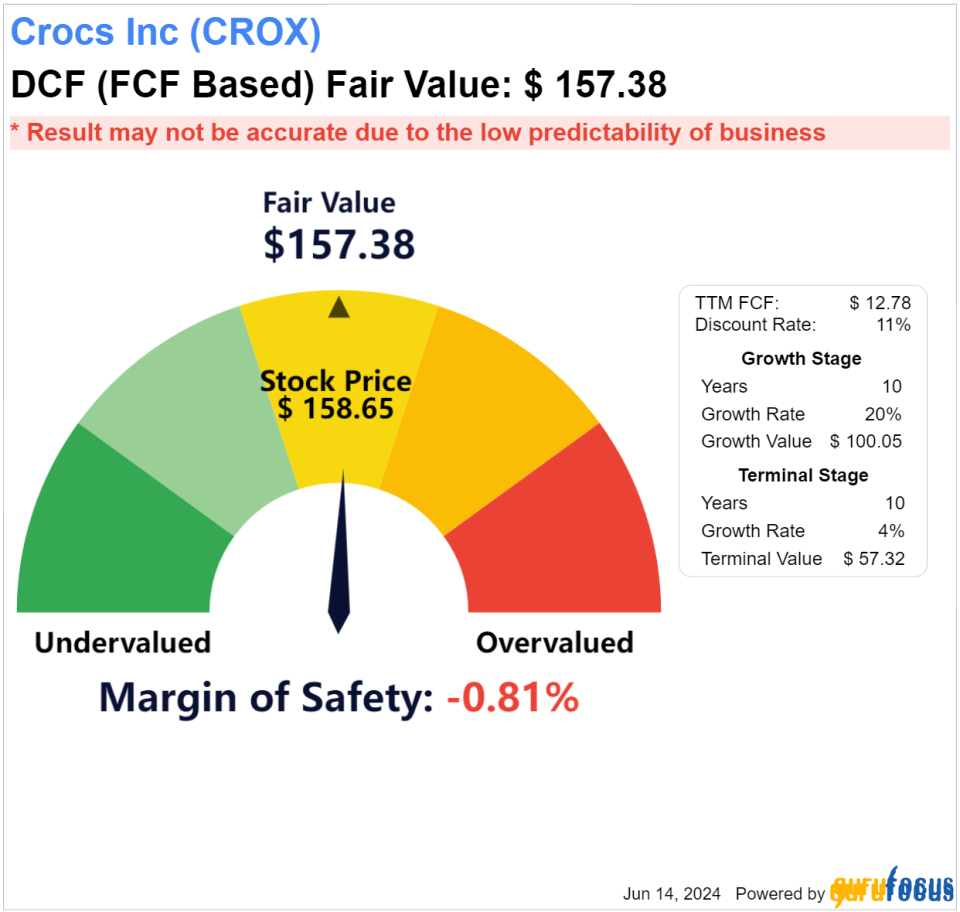

In a reverse discounted cash flow model, it is possible to see the market's assumptions are similar to those described above, with estimates close to 6% FCF growth for the next decade and 4% for the terminal stage and a discount rate of 11%, giving us a price equal to the current one ($157). In other words, even with a history of recent growth and some initiatives that could lead to its growth being maintained and its profitability returning to better levels at some point in the future, the stock is traded with a certain amount of suspicion.

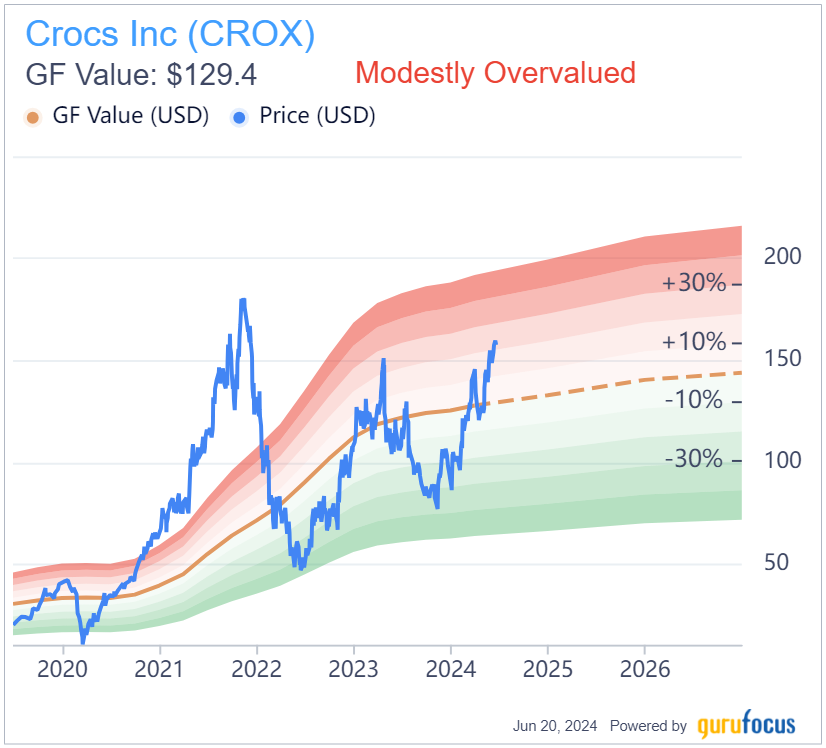

The forward price-earnings ratio is 12, below the average of the last five years (14.50), a reasonably attractive level, but one that does not attract as much attention after the stock's recent advances. As for GF Value, the recent performance has taken the stock from undervalued to modestly overvalued.

In short, I believe Crocs stands out in the apparel and footwear space, with a business model that has interesting moats and growth possibilities. Even a DCF with conservative assumptions can support the thesis, which is why I think it would be wise to keep the stock on your radar until it reaches a better margin of safety.

This article first appeared on GuruFocus.