Yahoo Finance

Yahoo Finance Deckers Outdoor Is Overvalued, but Offers Exceptional Growth, High ROIC

Deckers Outdoor Corp. (NYSE:DECK) has a great history of compounding its shareholders' money over time. Over the past 10 years, its share price has advanced by 1,133%, equivalent to a 28.80% compounded annual return. In the past 12 months, the share price has surged by nearly 105% as of the time of writing. In spite of impressive business expansion, recent share price increases are making the stock overvalued.

Impressive 2024 growth

The company is a global leader in innovative footwear, apparel and accessories for both everyday casual and high-performance use. With six proprietary brandsUGG, HOKA, Teva, Sanuk, Koolaburra and AHNUDeckers competes in the fashion, lifestyle, performance and outdoor markets. The company does not itself manufacture its products, but outsourced to third-party manufacturers. This enables it to keep an asset-light balance sheet and enable it to concentrate primarily on designing, advertising as well as distribution. The company's strategy concentrates on direct-to-consumer sales, which includes e-commerce and 164 worldwide retailers in 56 different countries, boosting brand loyalty and merchandise sales.

The outcome of Deckers Outdoor's fiscal year 2024 were nothing short of incredible, demonstrating a well-executed approach as well as strong brand image. The company reported an 18% increase in revenue, almost reaching $4.30 billion. The remarkable growth was fueled by an impressive increase in gross margin to 55.60%, 530 basis points higher compared to last year. The operating margin climbed to 21.60%, while earnings per share improved by 51% to $29.16.

The company's standout brands, HOKA and UGG, have driven significant growth. HOKA achieved global revenue of $1.80 billion, a 28% increase year over year. This growth was fueled by increased brand awareness, with U.S. awareness reaching approximately 40% and international regions just over 20%. As President and CEO Dave Powers said in a statement, "Aligned with our strategy to solidify HOKA as a global player, international regions are driving particularly strong gains in awareness, increasing more than 80% versus the prior year."

Meanwhile, UGG delivered strong results with global revenue of $2.20 billion, a 16% increase year over year through mainly the DTC and international business.

DTC business is the strategic focus

Deckers Brands experienced robust DTC growth in 2024, reflecting its strategic focus on expanding this high-margin channel. DTC revenue surged by 27%, contributing nearly $400 million in incremental business and representing 43% of the total company revenue, up from 40% in the prior fiscal year. The increase was driven by strong performances across Deckers' leading brands, with HOKA and UGG's DTC revenues increasing by 40% and 22%. This growth highlights the effectiveness of Deckers' omni-channel marketplace management strategy, which emphasizes maintaining lean inventory levels, preserving premium brand positioning and capturing upside demand through direct engagement with consumers.

As Powers said, "We remain encouraged by the growth across markets, with the U.S. continuing to deliver strong increases in alignment with global averages and international regions increasing more than 50% in both acquisition and retention."

This strategic emphasis on DTC not only enhances margins, but also fosters stronger consumer connections.

Growing operating performance with high ROIC

I always like companies with growing operating performance alongside sustainable, high returns on invested capital. This is true with Deckers Outdoor.

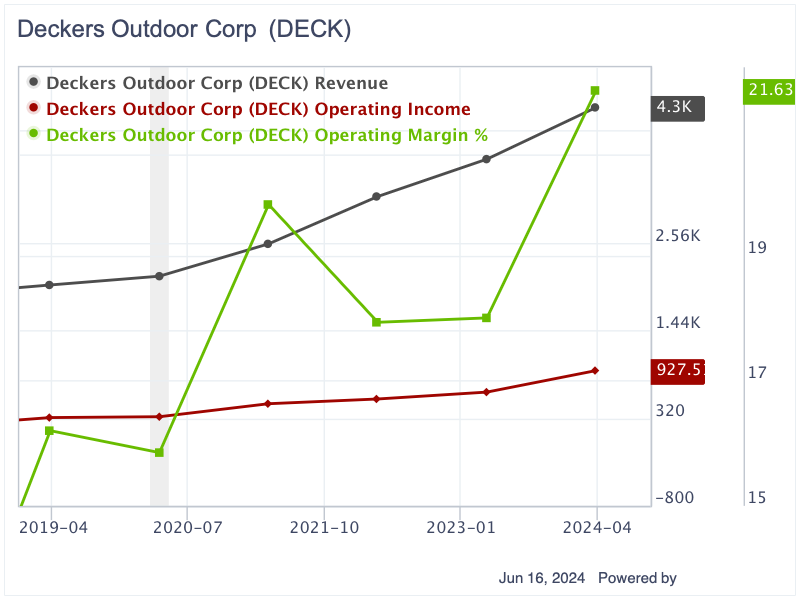

The company has increased its revenue from $2 billion in 2019 to $4.29 billion in 2024. In those five years, operating income grown from $327 million to $927.50 million. The operating margin also improved from 16.20% to 21.63%.

Deckers Outdoor was able to continue boosting both revenue and operating income throughout the Covid-19 pandemic. Increased sales during the period were due primarily to the DTC business and adaptability as well as worldwide expansion of the HOKA brand.

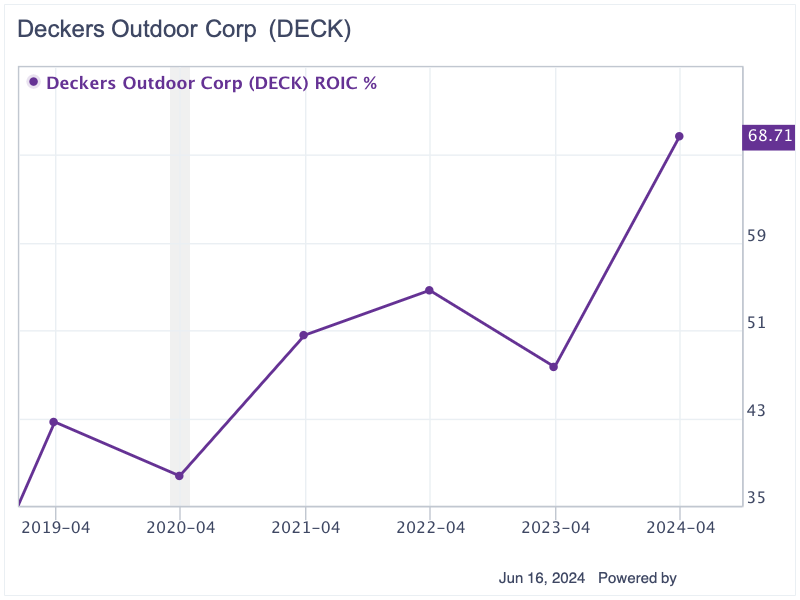

Along with the growing revenue and operating profits, Deckers Outdoor has managed to generate extremely high ROIC. Moreover, its ROIC has improved over time, from 42.65% in 2019 to 68.71% in 2024.

Debt-free balance sheet

What makes investors sleep well at night is Deckers Outdoor's debt-free balance sheet. As of March, it had $2.10 billion in total shareholders' equity, including a huge cash balance of $1.50 billion. The company does not employ any interest-bearing debt. It only incurred operating lease liabilities due to its retail operations. The total lease liabilities came in at $266.90 million, accounting for 17.80% of the company's cash position.

Significantly overvalued

For fiscal 2025, Deckers Outdoor's management estimated it could deliver 10% revenue growth to $4.70 billion. The operating margin could come in a bit lower at 19.50%, translating into $916.50 million. Using this management outlook, let's calculate the stock's intrinsic value.

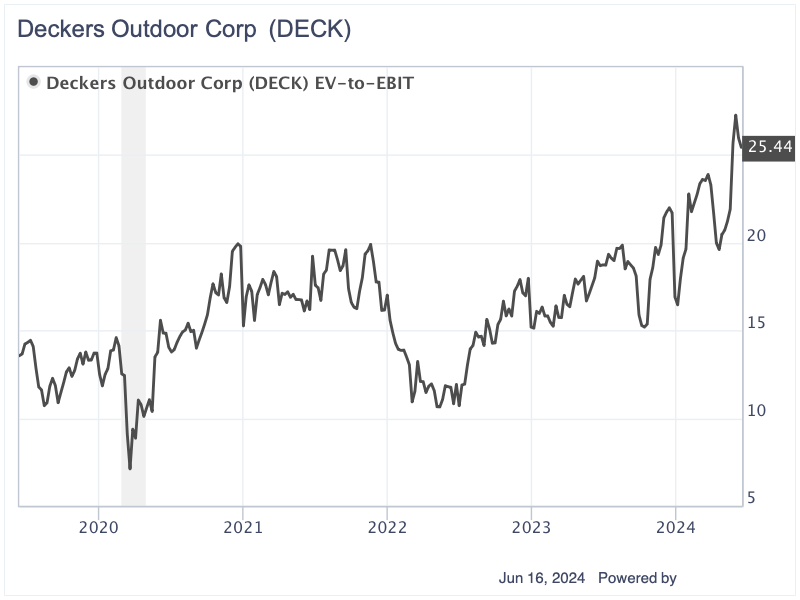

The company is currently valued at the top range of its five-year valuation at around 25.40 times Ebit. In the last five years, its Ebit multiples have fluctuated in the range of 7.11 to 27.27, with a five-year average of 16.10.

If Deckers Outdoor can maintain its current Ebit multiple of 25.40, its enterprise value should be $23.28 billion. If we apply a five-year average Ebit multiple, its enterprise value should be only $14.76 billion. Both of these valuations are much lower than its current enterprise value of $24.80 billion. This currently values Deckers Outdoor as high as 27 times its 2025 Ebit.

As the result, we can conclude the market is currently over optimistic about the company, placing a high valuation on the stock, making it quite expensive now.

Conclusion

While Deckers Outdoor has shown exceptional growth, the stock market's recent surge implies that optimism has caused overvaluation. With the company currently valued at the upper end of its historical Ebit multiple range, there appears to be little margin of safety for value investors.

Deckers' strong operational performance, high ROIC and debt-free balance sheet are commendable, but prudent investors might wait for a more attractive entry point. In the meantime, it would be wise to keep an eye on the company for future opportunities when the valuation aligns more closely with the underlying fundamentals.

This article first appeared on GuruFocus.