Yahoo Finance

Yahoo Finance Exploring Three SEHK Growth Companies With High Insider Ownership

Amidst a backdrop of global economic recalibrations, the Hong Kong market has shown resilience with the Hang Seng Index climbing by 3.11%. This robust performance highlights an environment where growth companies with high insider ownership can be particularly compelling, as these firms often demonstrate aligned interests between shareholders and management, fostering strong corporate governance and potentially enhanced long-term value creation.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

Name | Insider Ownership | Earnings Growth |

iDreamSky Technology Holdings (SEHK:1119) | 20.1% | 104.1% |

New Horizon Health (SEHK:6606) | 16.6% | 61% |

Fenbi (SEHK:2469) | 32.1% | 43% |

Meitu (SEHK:1357) | 38% | 34.3% |

Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.5% | 79.3% |

Adicon Holdings (SEHK:9860) | 22.3% | 29.6% |

Beijing Airdoc Technology (SEHK:2251) | 26.7% | 83.9% |

Zhejiang Leapmotor Technology (SEHK:9863) | 14.2% | 76.2% |

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 15.7% | 100.1% |

Ocumension Therapeutics (SEHK:1477) | 17.7% | 93.7% |

Let's dive into some prime choices out of from the screener.

Meitu

Simply Wall St Growth Rating: ★★★★★☆

Overview: Meitu, Inc. is an investment holding company that specializes in developing image, video, and design products to promote industry digitalization with beauty-related solutions, operating both in the People’s Republic of China and globally, with a market capitalization of approximately HK$14.60 billion.

Operations: The company generates revenue primarily from its Internet Business segment, totaling CN¥2.70 billion.

Insider Ownership: 38%

Earnings Growth Forecast: 34.3% p.a.

Meitu has demonstrated robust growth with a significant increase in sales to CNY 2.70 billion and net income to CNY 378.29 million in the past year, reflecting strong operational performance. Despite low forecasted return on equity and shareholder dilution, revenue and earnings are expected to outpace the Hong Kong market significantly, with substantial insider purchases underscoring confidence from within. The company also plans changes to its Articles of Association, potentially impacting governance structures positively.

Click to explore a detailed breakdown of our findings in Meitu's earnings growth report.

Our expertly prepared valuation report Meitu implies its share price may be too high.

Tian Tu Capital

Simply Wall St Growth Rating: ★★★★★☆

Overview: Tian Tu Capital Co., Ltd. is a private equity and venture capital firm focusing on early-stage, mature, and Pre-IPO investments in small and medium-sized companies, with a market capitalization of approximately HK$2.45 billion.

Operations: The revenue from asset management for the firm is CN¥-0.77 billion.

Insider Ownership: 34%

Earnings Growth Forecast: 70.5% p.a.

Tian Tu Capital is poised for substantial growth with expected revenue increases of 63.2% per year, outpacing the Hong Kong market average significantly. Despite making less than US$1m in revenue and facing high share price volatility, the company's earnings are forecast to grow by 70.47% annually. Recent executive changes and the decision not to issue a dividend highlight some governance and financial strategy shifts, yet its trading value stands at 72% below estimated fair value, suggesting potential underpricing.

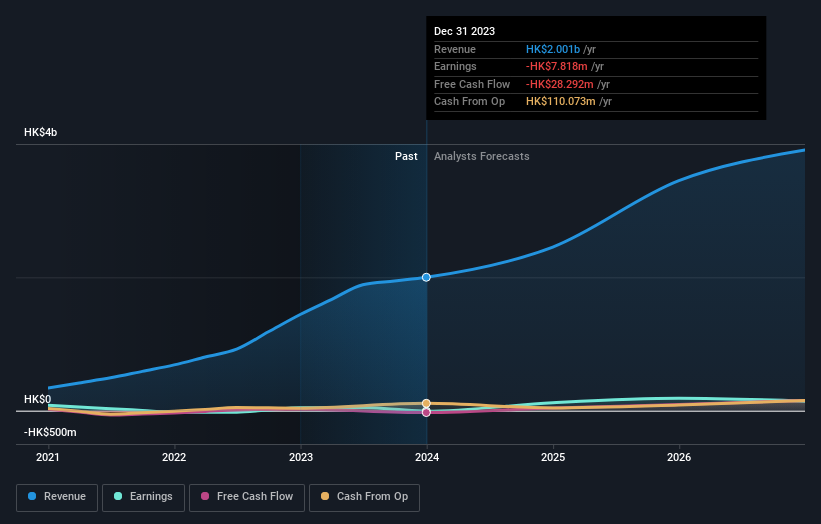

Vobile Group

Simply Wall St Growth Rating: ★★★★★☆

Overview: Vobile Group Limited, an investment holding company, offers software as a service for digital content asset protection and transactions across the United States, Japan, Mainland China, and other global markets, with a market capitalization of approximately HK$3.39 billion.

Operations: The company generates revenue primarily through its SaaS offerings, totaling approximately HK$2.00 billion.

Insider Ownership: 23.2%

Earnings Growth Forecast: 56.5% p.a.

Vobile Group, a growth-oriented company with significant insider ownership in Hong Kong, recently secured HK$159.99 million through convertible bonds, signaling strong investor confidence despite a net loss reported for 2023. The firm's revenue surged by approximately 26% in Q1 2024 compared to the previous year, with notable gains in mainland China and monthly recurring revenue. While facing shareholder dilution over the past year, Vobile is expected to turn profitable within three years, outstripping average market growth forecasts significantly.

Taking Advantage

Navigate through the entire inventory of 52 Fast Growing SEHK Companies With High Insider Ownership here.

Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Contemplating Other Strategies?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1357 SEHK:1973 and SEHK:3738.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com