Yahoo Finance

Yahoo Finance Exploring Undervalued TSX Stocks With Discounts Ranging From 11.4% To 42.9%

Amidst a backdrop of moderating inflation and shifting interest rate expectations in both the U.S. and Canada, investors are closely watching market movements for potential opportunities. In this environment, identifying undervalued stocks on the TSX can be particularly compelling, as these assets may present significant value in light of current economic conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

Name | Current Price | Fair Value (Est) | Discount (Est) |

Calian Group (TSX:CGY) | CA$55.42 | CA$110.42 | 49.8% |

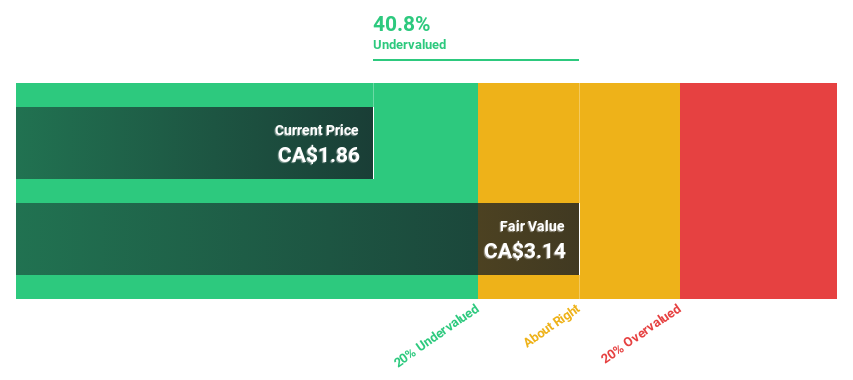

Calibre Mining (TSX:CXB) | CA$1.86 | CA$3.14 | 40.8% |

goeasy (TSX:GSY) | CA$187.26 | CA$313.66 | 40.3% |

Trisura Group (TSX:TSU) | CA$42.00 | CA$80.18 | 47.6% |

Viemed Healthcare (TSX:VMD) | CA$10.45 | CA$20.08 | 48% |

Endeavour Mining (TSX:EDV) | CA$28.61 | CA$54.00 | 47% |

Green Thumb Industries (CNSX:GTII) | CA$15.96 | CA$27.20 | 41.3% |

Jamieson Wellness (TSX:JWEL) | CA$27.98 | CA$46.93 | 40.4% |

Kits Eyecare (TSX:KITS) | CA$7.85 | CA$14.24 | 44.9% |

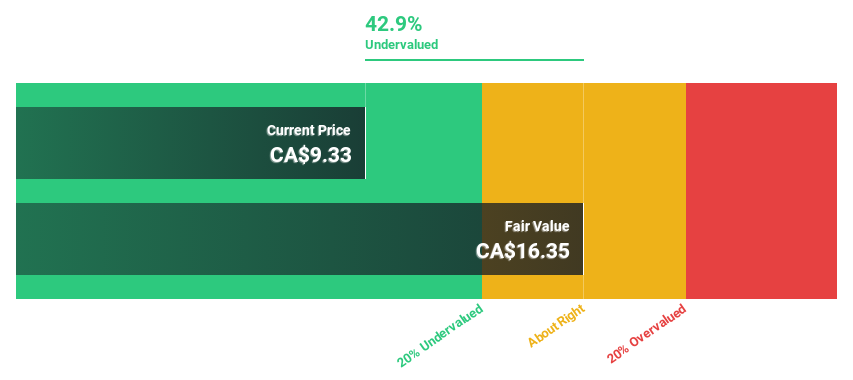

Capstone Copper (TSX:CS) | CA$9.33 | CA$16.35 | 42.9% |

We're going to check out a few of the best picks from our screener tool

Capstone Copper

Overview: Capstone Copper Corp. is a copper mining company with operations in the United States, Chile, and Mexico, and has a market capitalization of approximately CA$6.66 billion.

Operations: The company's revenue is primarily generated from its mining operations at Pinto Valley ($438.59 million), Mantoverde ($307.90 million), Mantos Blancos ($379.16 million), and Cozamin ($216.78 million).

Estimated Discount To Fair Value: 42.9%

Capstone Copper, trading at CA$9.33, significantly below the estimated fair value of CA$16.35, appears undervalued based on cash flow analysis. Recent financials show a reduction in net loss to US$4.84 million from US$20 million year-over-year with a slight earnings per share improvement. Despite recent equity offerings raising AUD 592.8 million and projected revenue growth at 18.1% annually—above the Canadian market average—the company's profitability is expected within three years, though past shareholder dilution raises concerns about future value per share retention.

Calibre Mining

Overview: Calibre Mining Corp. operates in the exploration, development, and mining of gold properties across Nicaragua, the United States, and Canada, with a market capitalization of approximately CA$1.40 billion.

Operations: The company generates revenue primarily from refined gold, totaling CA$566.68 million.

Estimated Discount To Fair Value: 40.8%

Calibre Mining, priced at CA$1.86, is undervalued per DCF valuation, suggesting a fair value of CA$3.14. Recent drill results from Valentine Gold Mine indicate significant untapped potential, enhancing its investment appeal despite a net loss this quarter. With expected annual earnings growth outpacing the Canadian market average significantly and revenue growth forecasts also strong, the stock shows promise although recent substantial insider selling and shareholder dilution could temper optimism.

Our growth report here indicates Calibre Mining may be poised for an improving outlook.

Get an in-depth perspective on Calibre Mining's balance sheet by reading our health report here.

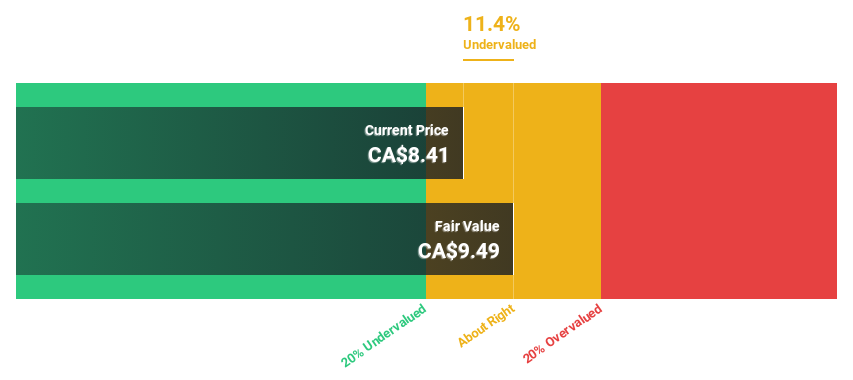

Energy Fuels

Overview: Energy Fuels Inc. operates in the United States, focusing on the extraction, recovery, recycling, exploration, permitting, evaluation, and sale of uranium mineral properties with a market capitalization of approximately CA$1.35 billion.

Operations: The company's revenue primarily stems from miscellaneous metals and mining activities, totaling CA$43.74 million.

Estimated Discount To Fair Value: 11.4%

Energy Fuels, trading at CA$8.41, is considered undervalued with a DCF-based fair value of CA$9.49. Analyst consensus suggests strong potential with a 77.2% upside and forecasts indicate robust revenue growth at 40.8% annually, outpacing the Canadian market's 7.3%. The recent strategic alliance to develop the Donald Project in Australia underscores its commitment to expanding its uranium and rare earth elements production, aligning with global clean energy needs despite recent shareholder dilution concerns.

Next Steps

Unlock our comprehensive list of 24 Undervalued TSX Stocks Based On Cash Flows by clicking here.

Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Contemplating Other Strategies?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include TSX:CS TSX:CXB and TSX:EFR.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com