Yahoo Finance

Yahoo Finance Update of the Financial Strength of Columbia Financial, Inc.

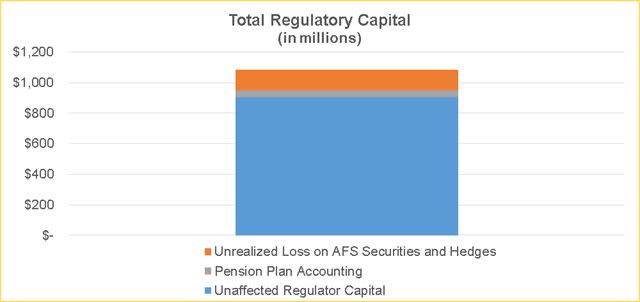

Total Regulatory Capital

Columbia Financial Inc. - Regulatory Capital

FAIR LAWN, N.J., March 12, 2023 (GLOBE NEWSWIRE) -- Silicon Valley Bank’s and Silvergate Bank’s problems have attracted nationwide attention. As such, Columbia Financial, Inc. (the “Company”) the holding company of Columbia Bank and Freehold Bank, want to assure clients and shareholders that the Company’s risk profile continues to be prudently managed in order to ensure a safe and secure environment. The below statement demonstrates that the Company’s risk profile vastly differs from both Silicon Valley Bank and Silvergate Bank.

We believe that Silicon Valley Bank’s and Silvergate Bank’s distress was caused by high exposure to undiversified lines of business. In particular, we understand that Silvergate maintained significant exposure to cryptocurrencies, while Silicon Valley maintained significant exposure to the venture capital and start-up companies. Cryptocurrency is extremely volatile and venture capital and early stage companies rely on new capital to fund early-stage cash burn. While unrealized losses on bonds (due to the rise in interest rates) appears to have contributed to Silicon Valley Bank’s failure, we believe that a lack of liquidity and capital to realize those losses played a key role in the closure of that bank.

Columbia Bank is a community bank with a diverse depositor base with over 210,000 accounts serviced through 64 branches with an average depositor account balance of approximately $37,000. Columbia Financial does not have any significant depositor concentrations. The Company is neither exposed to cryptocurrency loans, deposits or services in any way, nor is the Company involved with the venture capital or early stage company space. The Company has a community bank strategy by way of gathering in-market deposits and lending to local consumers and businesses in a conservative manner.

Columbia Financial does have unrealized losses on its available for sale bond portfolio, just like almost every other bank in America. At December 31, 2022, the additional other comprehensive income (“AOCI”) impact of the available for sale securities portfolio was $135.5 million. The other material component of AOCI is related to the Company’s defined benefit plan of $44.3 million, which is currently 83% overfunded.

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/53aa0b6e-9321-4596-990d-e575cd1a0c1d

The Company’s capital base relative to its asset size provides a more than adequate cushion relative to our unrealized loss on the securities portfolio. Furthermore, the Company has no need to sell securities, as it has a significant amount of liquidity. As of the close of business on March 10, 2023, Columbia Bank has immediate access to over $1.7 billion in funding, with plenty of additional available collateral to pledge to generate even more liquidity if needed. Our available sources of liquidity on March 10, 2023 are as follows:

Cash and cash equivalents on balance sheet are $84.2 million.

Borrowing capacity based on collateral already pledged at the FHLB of New York is $1.3 billion.

Untapped correspondent lines of credit amount to $339.0 million.

Unpledged securities, with a market value of $525.6 million, are available to pledge at the FHLB, brokers or the Federal Reserve.

Unpledged loan collateral available to pledge is over $4.0 billion.

Borrowing capacity based on collateral already pledged at the Federal Reserve of New York is $54.3 million.

As demonstrated, Columbia’s liquidity position is very strong.

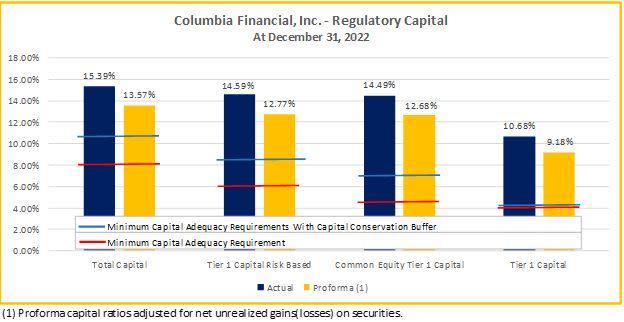

The Company’s tier 1 leverage ratio was 10.68% at December 31, 2022. If every available for sale bond was sold, the Company’s tier 1 leverage ratio would be 9.18%, more than double the amount required by bank regulation. The following table provides the Company’s regulatory capital ratios at December 31, 2022, along with the pro forma capital ratios if the Bank sold all available for sale securities as of that date.

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/82fa5aaa-4273-4a5c-8a53-4bd316afb8e1

In summary, the Company has a diversified deposit base and a conservative community bank business model which is completely different than the profile of the two failed banks. The Company has a strong capital position, abundant liquidity, conservative credit culture and market-leading low level of problem loans, all of which we believe enables us to withstand current and future market conditions.

Forward Looking Statements

Certain statements herein constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act and are intended to be covered by the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such statements may be identified by words such as “believes,” “will,” “would,” “expects,” “projects,” “may,” “could,” “developments,” “strategic,” “launching,” “opportunities,” “anticipates,” “estimates,” “intends,” “plans,” “targets” and similar expressions. These statements are based upon the current beliefs and expectations of the Company’s management and are subject to significant risks and uncertainties. Actual results may differ materially from those set forth in the forward-looking statements as a result of numerous factors. Factors that could cause such differences to exist include, but are not limited to, adverse conditions in the capital and debt markets and the impact of such conditions on the Company’s business activities; changes in interest rates, higher inflation and their impact on national and local economic conditions; changes in monetary and fiscal policies of the U.S. Treasury, the Board of Governors of the Federal Reserve System and other governmental entities; competitive pressures from other financial institutions; the effects of general economic conditions on a national basis or in the local markets in which the Company operates, including changes that adversely affect a borrowers’ ability to service and repay the Company’s loans; the effect of the COVID-19 pandemic, including on our credit quality and business operations, as well as its impact on general economic and financial market conditions; changes in the value of securities in the Company’s portfolio; changes in loan default and charge-off rates; fluctuations in real estate values; the adequacy of loan loss reserves; decreases in deposit levels necessitating increased borrowing to fund loans and securities; legislative changes and changes in government regulation; changes in accounting standards and practices; the risk that goodwill and intangibles recorded in the Company’s consolidated financial statements will become impaired; demand for loans in the Company’s market area; the Company’s ability to attract and maintain deposits; risks related to the implementation of acquisitions, dispositions, and restructurings; the risk that the Company may not be successful in the implementation of its business strategy, or its integration of acquired financial institutions and businesses, and changes in assumptions used in making such forward-looking statements which are subject to numerous risks and uncertainties, including but not limited to, those set forth in Item 1A of the Company's Annual Report on Form 10-K and those set forth in the Company's Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, all as filed with the Securities and Exchange Commission (the “SEC”), which are available at the SEC’s website, www.sec.gov. Should one or more of these risks materialize or should underlying beliefs or assumptions prove incorrect, the Company's actual results could differ materially from those discussed. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this release. The Company disclaims any obligation to publicly update or revise any forward-looking statements to reflect changes in underlying assumptions or factors, new information, future events or other changes, except as required by law.

Columbia Financial, Inc.

Investor Relations Department

(833) 550-0717