Yahoo Finance

Yahoo Finance Global Data Centre Pricing Analysis Report 2023: Data Centre Pricing is Evolving Rapidly With Inflation Adjustment & New Cloud Fabric Services Being the Key Developments

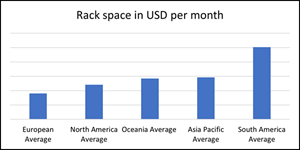

Rack Space in USD per Month

Dublin, Jan. 27, 2023 (GLOBE NEWSWIRE) -- The "The Future of Data Centre Pricing" report has been added to ResearchAndMarkets.com's offering.

The analyst herein provides an insight into data centre pricing adopted across the globe and the key trends to the Future of Data Centre Pricing.

The report quantifies the 10 key trends taking place in Data Centre Pricing worldwide. One of the trends identified is that Data Centre Providers are seeking to charge more for their ancillary services - Ancillary services are providing a useful source of additional revenue to colocation services and Data Centre Providers are making substantial new investments in DCIM services and cloud fabric services. Reported Data Centre financial results however seem to indicate that there is only a gradual increase in non-colocation services, as shown with an example.

The report also looks at Remote hands services which are being offered at a range of different pricing.

The analyst concludes that Inflationary conditions are likely to persist and pricing for rack space rentals is increasing in most markets by an average of around 2 percent per annum. There has been an increase in rentals in selected Tier 2 markets in particular driven by the introduction of wholesale capacity from cloud and hyperscale users.

The launch of new capacity increases price levels over time. Cloud Service Providers (CSPs) are building new Availability Zones (AZ's) in Tier 2 markets including Athens, Israel, Madrid, Milan, Oslo, Stockholm, Turin, Vienna & Warsaw as part of a programme of deploying cloud services in new markets (partly to generate new users and to allay data sovereignty concerns).

The main pricing increase has been in power costs - Although energy costs are typically "passed through" power usage applied by a Data Centre Provider typically are applied with an extra margin to cover facility costs (with the exception of the USA market where Data Centres are prohibited from adding any additional power charge unless they are a registered utility).

The power costs applied vary by Data Centre Provider. The per kW rental rate applied is also increased by a factor to cover the facility's operational cost, typically multiplied by a PUE (Performance Usage Effectiveness) factor of up to 1.5 times allowing an additional rental cost.

Data Centre Providers are seeking to diversify their business by introducing a range of new connectivity services. These include cloud fabric services (which provide access to a number of cloud providers using a virtualised online portal), metro connectivity services and IXP (Internet Exchange) services to connect to a range of ISPs.

Data Centres are investing in online portals and DCIM (Data Centre Investment Management) for service automation - in order to provide near real-time information - on current server utilisation and power usage. They are also set to introduce predictive analytics using machine learning and AI to forecast future usage.

Despite the investment in new technology and connectivity services the majority of Data Centre Provider revenues are derived from colocation services. And the rentals of Data Centres remain focused on dedicated cabinets or racks using long-term contracts and so are different from the virtualised on-demand services used by the CSP.

Data Centre rack space rentals are increasing over time. But there remains a wide range of average rack space pricing worldwide with considerable differences between regions. Average Data Centre rentals in the most mature markets such as Europe and North America are considerably lower than the newer Data Centre markets in the Asia Pacific and South America regions where rentals remain much higher.

Key Data Centre pricing is typically composed of a core rental for rack space plus a rental for the "right" to use an amount of power plus a usage charge per kWH (kilo-Watt Hour) which varies according to usage. Data Centre capacity continues to increase, particularly in Tier 2 markets where cloud operators are introducing services (in countries such as South Africa and Mexico) and is driving ecosystems in those regions. Data Centre capacity is set to continue to increase despite the economic conditions.

The analyst finds that Data Centre Pricing is continuing to evolve worldwide as Data Centre Providers respond to a series of new challenges.

The challenges include:

The migration to cloud services: Cloud Service Providers (CSPs) are a significant user of colocation capacity, accounting for 30% of revenues. Retail Data Centres are offering both colocation services and access to the cloud as part of a hybrid cloud solution. But those local Data Centres without cloud access face an uncertain future.

Wholesale Data Centre capacity is growing rapidly worldwide: Wholesale Data Centre capacity is growing worldwide, driven by CSPs and hyperscale users, as cloud providers expand their services into new markets.

Price rentals for Data Centres are increasing over time: Data Centre rentals are increasing as new high specification facilities are launched. The construction cost of new facilities is increasing. Additionally, Data Centre Providers are introducing a CPI (Consumer Price Index) factor into their end-user pricing to cover inflation & protect their margins.

Power pricing is also increasing rapidly: Data Centre power costs worldwide are increasing as a result of the conflict in Ukraine. Data Centre Providers are passing on the increase in power costs to their users, with utility costs increasing by as much as 80% in Europe over the last 6 month period.

Key Topics Covered:

Part One - An introduction to Data Centre Pricing

Introduction

The factors that influence Data Centre Pricing

The elements of Data Centre Pricing

The different models for Data Centre Pricing

The changes in Data Centre Pricing

Summary

Part Two - The Future of Data Centre Pricing

Introduction

The Future of Data Centre Pricing

Data Centre Pricing around the world

New types of Data Centre Pricing

Summary

Part Three - Key Trends & Conclusions in the Future of Data Centre Pricing

Introduction

The 10 Key Trends in Data Centre Pricing

Data Centre Pricing in the next 5 years - from the end of 2022 to the end of 2027

Conclusions to the Future of Data Centre Pricing

Summary

A selection of companies mentioned in this report includes

Aruba Cloud

Equinix Data Centre

Google

Hines & Compass Datacenter

Hyperscale Data Centre

For more information about this report visit https://www.researchandmarkets.com/r/6qb3h4-future-of?w=12

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900