Yahoo Finance

Yahoo Finance Global Synchronous Condenser Market Report to 2027 - Converting Existing Synchronous Generators into Synchronous Condensers Presents Opportunities

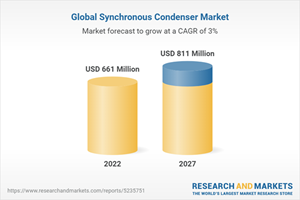

Global Synchronous Condenser Market

Dublin, Dec. 06, 2022 (GLOBE NEWSWIRE) -- The "Synchronous Condenser Market by Cooling Type (Hydrogen-Cooles, Air-Cooled, Water-Cooled), Type (New & Refurbished), Starting Method (Static Frequency Converter, Pony Motor), End-User, Reactive Power Rating and Region - Global Forecast to 2030" report has been added to ResearchAndMarkets.com's offering.

The global synchronous condenser market is projected to grow from USD 661 million in 2022 to USD 811 million by 2030, registering a CAGR of 2.6% during the review period.

New Synchronous Condenser: is expected to be the largest segment synchronous condenser market, by type

The type segment is categorized as New Synchronous Condenser and refurbished synchronous condenser. A new synchronous condenser is constructed with 2 or 4 poles (2-pole pair), which can be cooled with hydrogen, air, and water. With the globally expanding HVDC network, countries such as Canada, Brazil, and Italy have deployed new synchronous condensers for stabilizing and improving transmission systems' stability and strength. Besides, they are also being deployed to control voltage fluctuations and provide reactive power support.

The hydrogen cooled synchronous condenser segment is expected to emerge as the fastest segment, by Cooling technology

The Synchronous Condenser market has been segmented into hydrogen cooled synchronous condenser, Air cooled synchronous condenser and Water cooled synchronous condenser. The hydrogen-cooled synchronous condenser uses gaseous hydrogen as a coolant because of its superior cooling properties.

It exhibits low density, high specific heat, and high thermal conductivity features. The hydrogen-cooled synchronous condenser has 1.5 times higher heat transfer capability and 1/14th the density than its air-cooled counterpart, resulting in fewer friction losses and faster cooling. Hydrogen-cooled synchronous condensers can be operated at a higher load with the same temperature rise, and the windage loss is lower than air-cooled synchronous condensers.

North America is expected to account for the largest market size during the forecast period.

North America is expected to be the largest market during the forecast period. North America has aging power infrastructures, which may increase the risk of blackouts. Therefore, governments of different countries in this region are actively focusing on upgrading and replacing aging infrastructures to improve grid reliability and resilience and develop smart electricity networks.

The North American power sector is currently facing challenges such as meeting energy-efficiency targets, compliance with federal carbon policies, and integrating various distributed generation sources in the grid.

Report Attribute | Details |

No. of Pages | 226 |

Forecast Period | 2022 - 2027 |

Estimated Market Value (USD) in 2022 | $661 Million |

Forecasted Market Value (USD) by 2027 | $811 Million |

Compound Annual Growth Rate | 3.0% |

Regions Covered | Global |

Key Topics Covered:

1 Introduction

2 Research Methodology

3 Executive Summary

4 Premium Insights

5 Market Overview

5.1 Introduction

5.2 COVID-19 Health Assessment

5.3 Market Dynamics

5.3.1 Drivers

5.3.1.1 Increasing Demand for Renewable Power Generation

5.3.1.2 Growing Need for Power Factor Correction (Pfc)

5.3.2 Restraints

5.3.2.1 High Maintenance and Equipment Costs of Synchronous Condensers

5.3.3 Opportunities

5.3.3.1 Converting the Existing Synchronous Generators into Synchronous Condensers

5.3.3.2 Expanding High-Voltage Direct Current (Hvdc) Network

5.3.4 Challenges

5.3.4.1 Availability of Low-Cost Alternatives Such as Synchronous Generators, Capacitors, and Statcom

5.3.4.2 Rising Product Costs Due to Shortage of Components/Parts Used in Manufacturing Synchronous Condensers Due to COVID-19

5.4 YC-Shift

5.4.1 Revenue Shift & New Revenue Pockets for Synchronous Condenser Manufacturers

5.5 Market Map

5.6 Average Pricing of Synchronous Condenser

5.7 Value Chain Analysis

5.7.1 Raw Material Providers/ Suppliers

5.7.2 Component Manufacturers

5.7.3 Assemblers/Manufacturers

5.7.4 Distributors (Buyers)/ End-users and Post-Sales Services

5.8 Case Study Analysis

5.8.1 Terna's Synchronous Condenser Success

5.8.1.1 Problem Statement

5.8.1.2 Possible Solution by GE's Synchronous Condenser

5.9 Technology Analysis

5.10 Regulatory Landscape

5.10.1 Regulatory Framework in North America

5.10.2 Regulatory Framework in Europe

5.11 Porter's Five Forces Analysis

6 Impact of COVID-19 on Synchronous Condenser Market, Scenario Analysis, by Region

6.1 Scenario Analysis

6.1.1 Optimistic Scenario

6.1.2 Realistic Scenario

6.1.3 Pessimistic Scenario

7 Synchronous Condenser Market, by Cooling Type

7.1 Introduction

7.2 Hydrogen Cooled

7.2.1 High Thermal Conductivity of Hydrogen-Cooled Synchronous Condensers is Expected to Foster Their Demand

7.3 Air Cooled

7.3.1 Improved Cooling Feature of Air-Cooled Synchronous Condensers Using Air Circulation is Likely to Fuel Market Growth

7.4 Water Cooled

7.4.1 Cost Efficiency of Water-Cooled Synchronous Condensers Over Their Hydrogen-Cooled Counterpart is Likely to Foster Their Demand in Market

8 Synchronous Condenser Market, by Starting Method

8.1 Introduction

8.2 Static Frequency Converters

8.2.1 Low Installation Costs and Low Noise Features Are Expected To Boost Demand for Static Frequency Converters

8.3 Pony Motors

8.3.1 Low Cost of Pony Motors is Likely to Foster Their Demand in Synchronous Condenser Market

8.4 Others

9 Synchronous Condenser Market, by Reactive Power Rating (Mvar)

9.1 Introduction

9.2 Up to 100 Mvar Synchronous Condensers

9.2.1 Growing Usage of Air- & Water-Cooled Synchronous Condensers is Expected to Foster Demand for Synchronous Condensers of Up to 100 Mvar

9.3 100-200 Mvar Synchronous Condensers

9.3.1 Use of 100-200 Mvar Synchronous Condensers for Transmission System Stability is Likely to Foster Their Demand

9.4 Above 200 Mvar Synchronous Condensers

9.4.1 Growing Use of Hydrogen-Cooled Synchronous Condensers is Expected to Boost Their Demand

10 Synchronous Condenser Market, by End-user

10.1 Introduction

10.2 Electrical Utilities

10.2.1 Demand for Grid Stability and Controlling Voltage Fluctuations is Expected to Drive Market

10.3 Industries

10.3.1 Requirement for Industrial Loads' Power Factor Correction is Likely to Drive Market

11 Synchronous Condenser Market, by Type

11.1 Introduction

11.2 New Synchronous Condensers

11.2.1 Expansion of Hvdc Network is Likely to Generate Demand for New Synchronous Condensers

11.3 Refurbished Synchronous Condensers

11.3.1 Refurbished Synchronous Condensers Are More Economical, Which is Likely to Propel Market Growth

12 Synchronous Condenser Market, by Region

13 Competitive Landscape

13.1 Overview

13.2 Market Share Analysis, 2019

13.3 Market Evaluation Framework

13.4 Synchronous Condenser Revenue Analysis of Top 5 Market Players

13.5 Key Market Developments

13.5.1 Product Launches

13.5.2 Contracts & Agreements

13.5.3 Collaborations

13.5.4 Mergers & Acquisitions

14 Company Evaluation Quadrant and Company Profiles

14.1 Company Evaluation Quadrant Definitions and Methodology

14.1.1 Stars

14.1.2 Innovators

14.1.3 Pervasive

14.1.4 Emerging Companies

14.1.5 Product Footprint Analysis of Top Players

14.2 Company Profiles

14.2.1 ABB

14.2.2 Siemens

14.2.3 GE

14.2.4 WEG

14.2.5 Eaton

14.2.6 Andritz

14.2.7 Ansaldo Energia

14.2.8 Fuji Electric

14.2.9 Voith Group

14.2.10 Bharat Heavy Electricals Limited (Bhel)

14.2.11 Ideal Electric Power (Hyundai Ideal Electric Co.)

14.2.12 Sustainable Power Systems

14.2.13 Power Systems & Controls

14.2.14 Brush Group

14.2.15 Electromechanical Engineering Associates

15 Adjacent & Related Market

16 Appendix

For more information about this report visit https://www.researchandmarkets.com/r/ladkzn

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900