Yahoo Finance

Yahoo Finance Can Growing Costs Hurt Discover Financial's (DFS) Q1 Earnings?

Discover Financial Services DFS is set to report its first-quarter 2024 results on Apr 17, after the closing bell.

What Do the Estimates Say?

The Zacks Consensus Estimate for first-quarter earnings per share of $2.96 suggests a 17.3% decrease from the prior-year figure of $3.58. The consensus mark remained stable over the past week. The consensus estimate for first-quarter revenues of $4.1 billion indicates an 8.2% increase from the year-ago reported figure.

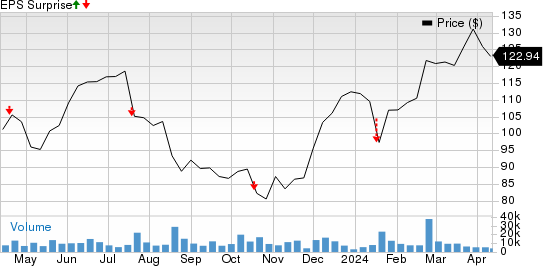

Discover Financial missed the consensus estimate for earnings in each of the trailing four quarters, with the average surprise being negative 16.6%. This is depicted in the graph below:

Discover Financial Services Price and EPS Surprise

Discover Financial Services price-eps-surprise | Discover Financial Services Quote

Before we get into what to expect for the to-be-reported quarter in detail, it’s worth taking a look at DFS’ previous-quarter performance first.

Q4 Earnings Rewind

The digital banking and payment services company reported adjusted earnings of $1.54 per share for the previous quarter, missing the Zacks Consensus Estimate by 38.4%. The quarterly results received a blow from escalating operating costs, feeble contributions from the Digital Banking segment and higher provision for credit losses. Nevertheless, the negatives were partially offset by receivables growth, deposit inflows and growing PULSE and Diners Club volumes.

Now, let’s see how things have shaped up before the first-quarter earnings announcement.

Q1 Factors to Note

Discover Financial's top-line performance is anticipated to have been positively influenced by an uptick in net interest income, which serves as the main contributor to its revenues. This metric is expected to have been propelled by strong asset expansion and favorable interest rate conditions during the first quarter.

The Zacks Consensus Estimate for the net interest income of DFS indicates 8% growth from the prior-year quarter’s reported figure of $3.1 billion, while our estimate suggests a 7.1% year-over-year increase.

The anticipated increase in receivables growth for Discover Financial in the upcoming quarter is expected to be propelled by robust sales, moderated payment rates, and improved new account growth. Additionally, the company's cautious strategies in underwriting, pricing, and marketing its non-card products are likely to have contributed to its performance during the period.

Increased debit transaction volume and higher spending in travel and entertainment-related activities are expected to have driven PULSE and Diners Club volume, leading to a positive performance for the Payment Services unit.

The top line of Discover Financial is also expected to have benefited from improving non-interest income in the first quarter. Improved loan fee income and higher net discount and interchange revenues, aided by a favorable sales mix, are likely to have contributed to the non-interest income growth of DFS. The Zacks Consensus Estimate for the metric indicates a 9.3% year-over-year increase, whereas our model estimate suggests a 9.6% jump.

However, strong sales usually give rise to high reward costs, which are expected to have partially offset the company's non-interest income. Our estimate for first-quarter reward costs indicates almost 6% year-over-year growth.

The Zacks Consensus Estimate for net interest margin is pegged at 10.82% for the first quarter, implying a decrease from 11.34% a year ago. The profits of Discover Financial are likely to have suffered a setback due to escalating costs. Also, the bottom line is expected to have been affected by high provisions for bad loans in the first quarter.

Marketing costs and professional fees are likely to have witnessed increases as DFS has been investing in technology and card and consumer banking products. Our estimate for employee compensation and benefits suggests almost 19% year-over-year growth. We expect total operating expense for the first quarter to have jumped more than 17% year over year, leading to a noticeable decline in the bottom line, making an earnings beat uncertain.

Earnings Whispers

Our proven model does not conclusively predict an earnings beat for Discover Financial this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. That is not the case here, as you will see below.

Earnings ESP: The company has an Earnings ESP of -1.67%. This is because the Most Accurate Estimate currently stands at $2.91 per share, lower than the Zacks Consensus Estimate of $2.96.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: Discover Financial currently carries a Zacks Rank #3.

Stocks to Consider

While an earnings beat looks uncertain for Discover Financial, here are some companies from the broader Finance space that you may want to consider, as our model shows that these have the right combination of elements to post an earnings beat this time around:

Mr. Cooper Group Inc. COOP has an Earnings ESP of +7.40% and is a Zacks #2 Ranked player. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Mr. Cooper Group’s bottom line for the to-be-reported quarter is pegged at $2.07 per share, indicating 76.9% year-over-year growth. The estimate grew by 2 cents in the past month. The consensus estimate for CACC’s revenues is pegged at $493.9 million, suggesting a 49.7% increase from a year ago.

SLM Corporation SLM has an Earnings ESP of +2.12% and a Zacks Rank of 2.

The Zacks Consensus Estimate for SLM Corporation’s bottom line for the to-be-reported quarter is pegged at 98 cents per share, suggesting a 108.5% year-over-year increase. The estimate increased by a penny over the past week. The consensus estimate for SLM’s revenues is pegged at $376.2 million.

Regional Management Corp. RM has an Earnings ESP of +1.15% and a Zacks Rank of 3.

The Zacks Consensus Estimate for Regional Management’s bottom line for the to-be-reported quarter is pegged at 87 cents per share. The consensus estimate for its revenues is pegged at $139.1 million, predicting a 2.7% increase from a year ago. RM beat earnings estimates in each of the past four quarters, with an average of 41.2%.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Discover Financial Services (DFS) : Free Stock Analysis Report

SLM Corporation (SLM) : Free Stock Analysis Report

Regional Management Corp. (RM) : Free Stock Analysis Report

MR. COOPER GROUP INC (COOP) : Free Stock Analysis Report