Yahoo Finance

Yahoo Finance Here's Why Hold Strategy is Apt for Everest Group (EG) Stock

Everest Group, Ltd.’s EG product diversification, higher income from the fixed income portfolio, favorable estimates, strong renewal retention, prudent capital deployment and a solid capital position make it worth retaining in one’s portfolio.

Growth Projections

The Zacks Consensus Estimate for Everest Group’s 2024 revenues is pegged at $17.74 billion, implying a year-over-year improvement of 21.4%.

The consensus estimate for 2025 earnings per share and revenues indicates an increase of 11.3% and 11.5%, respectively, from the corresponding 2024 estimates.

Earnings have grown 40.4% in the past five years, better than the industry average of 9.2%

Northbound Estimate Revision

The Zacks Consensus Estimate for EG’s 2024 and 2025 earnings has moved north 0.01% and 0.1% north, respectively, in the past 30 days. This should instill investors' confidence in the stock.

Earnings Surprise History

EG surpassed earnings estimates in each of the last four quarters, the average being 37.54%.

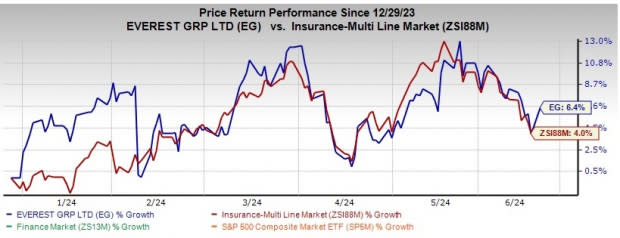

Zacks Rank & Price Performance

Everest Group currently carries a Zacks Rank #3 (Hold). Year to date, the stock has gained 6.4% compared with the industry’s growth of 4%.

Image Source: Zacks Investment Research

Return on Equity

Everest Group’s annualized after-tax operating income return on equity was 20% in the first quarter, which expanded 280 basis points year over year. Its return on equity for the trailing 12 months is 24.9%, which expanded 1,190 bps year over year. This reflects its efficiency in utilizing its shareholders’ funds.

Style Score

The insurer has a VGM Score of A. The VGM Score helps identify stocks with the most attractive value, best growth and the most promising momentum.

Business Tailwinds

Global presence, product diversification, rate increase and high retention rate continue to drive EG’s overall growth. The Insurance segment is poised to benefit from an increase in property and short tail business and a rise in specialty casualty business. On the other hand, leveraging opportunities stemming from the continued disruption and evolution of the reinsurance market should poise the Reinsurance segment for growth.

Net investment income stands to benefit from higher income from the fixed income portfolio, increase in limited partnership income, rise in dividend income from the equity portfolio and higher income from other invested assets. An improved interest rate environment adds to the upside.

Everest Group has a strong capital position, banking on sufficient cash generation capabilities and benefits from capital adequacy, financial flexibility, long-term operating performance and traditional risk management capabilities.

The company boasts a consistent increase in dividends, with the metric witnessing an eight-year (2016-2023) CAGR of 34.9%. The insurer targets a total shareholder return on equity of more than 17% from 2024 to 2026, reflecting robust and well-diversified earnings power. EG boasts consistent and industry-leading shareholder returns.

Everest Group has an impressive Growth Score of B. This style score helps analyze the growth prospects of a company.

However, the insurer has been experiencing an increase in expenses due to higher incurred losses and loss adjustment expenses, commission, brokerage, taxes and fees and other underwriting expenses. The company should continue to generate revenues at a higher magnitude than expenses.

Stocks to Consider

Some better-ranked stocks from the multi-line insurance industry are Radian Group Inc. RDN, Old Republic International Corporation ORI and EverQuote, Inc. EVER, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radian Group has a solid track record of beating earnings estimates in each of the trailing four quarters, the average being 22.79%. Year to date, shares of RDN have jumped 7%.

The Zacks Consensus Estimate for RDN’s 2024 and 2025 revenues implies year-over-year growth of 8.2% and 4.9%, respectively.

Old Republic International has a solid track record of beating earnings estimates in three of the last four quarters while missing in one, the average being 6.61%. Year to date, shares of ORI have inched up 1.9%.

The Zacks Consensus Estimate for ORI’s 2024 and 2025 earnings implies year-over-year growth of 3.8% and 4.4%, respectively.

EverQuote has a solid track record of beating earnings estimates in each of the trailing four quarters, the average being 65.16%. Year to date, shares of EVER have rallied 52.6%.

The Zacks Consensus Estimate for EVER’s 2024 and 2025 earnings implies year-over-year growth of 98% and 550%, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Radian Group Inc. (RDN) : Free Stock Analysis Report

EverQuote, Inc. (EVER) : Free Stock Analysis Report

Old Republic International Corporation (ORI) : Free Stock Analysis Report

Everest Group, Ltd. (EG) : Free Stock Analysis Report