Yahoo Finance

Yahoo Finance Here's Why Investors Should Hold Brown-Forman (BF.B) Stock

Brown-Forman Corp. (BF.B) looks well-poised on the back of increased demand for its brands, and growth across all geographic clusters and the Travel Retail channel, which have been driving organic sales growth. BF.B is also benefiting from recent acquisitions, portfolio premiumization, product innovation and strategic relationships. It expects strength in its brand portfolio, strong consumer demand and the return of inventories to more normalized levels to aid organic sales growth in fiscal 2023.

Driven by these factors, Brown-Forman reported a sales beat for the fifth straight quarter in third-quarter fiscal 2023. The top line increased 4% year over year on a reported basis and 5% on an organic basis. Sales benefited from strong consumer demand for its brands and sustained brand investments. It anticipates organic sales growth of 8-10% for fiscal 2023.

An uptrend in the Zacks Consensus Estimate for the Zacks Rank #3 (Hold) company echoes a positive sentiment. The Zacks Consensus Estimate for Brown-Forman’s fiscal 2023 sales suggests growth of 6.6% from the year-ago period’s reported number.

However, soft margin trends, resulting from input cost inflation, higher supply-chain costs, and increased compensation and advertising expenses, have been hurting the company’s bottom line. The consensus mark for the company’s EPS reflects a decline of 2.9% year over year.

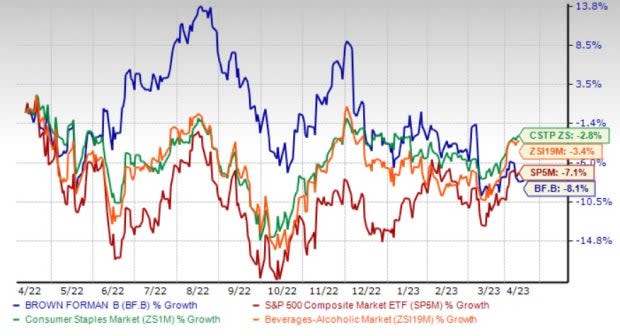

Moreover, the stock has lost 8.1% in the past year compared with the industry’s fall of 3.5%. The stock also compared unfavorably with the Consumer Staples sector’s decline of 2.8% and the S&P 500’s fall of 7.1%.

Image Source: Zacks Investment Research

Factors Driving Growth

Brown-Forman is focused on investing in the diversification of its brand portfolio to drive growth. For more than a decade, the Jack Daniel's Tennessee Whiskey has been the key contributor of growth in the United States. The company’s investments in brands center around broadening the Jack Daniel’s family of brands, while exiting the weaker brands and expanding the fast-growing premium spirits categories.

The company is investing in organically accelerating growth of two fast-growing spirits categories, bourbon and tequila. The balanced portfolio investments are supporting the company’s record of consistent growth.

In the first nine months of fiscal 2023, net sales for Jack Daniel’s family of brands were up 5% on a reported basis and 11% on an organic basis. The brand’s sales were driven by solid demand, higher pricing and the estimated increase in distributor inventories. The upside in sales was also driven by the strength in Jack Daniel’s Tennessee Whiskey in international markets and the Travel Retail channel.

Further, sales benefited from the continued consumer interest in flavor and convenience, which boosted the performance of Jack Daniel’s Ready-to-Drink (RTD), Jack Daniel’s Tennessee Honey and Jack Daniel’s Tennessee Fire. Innovation contributed to sales growth through the launch of Jack Daniel’s Bonded series.

In the first nine months of fiscal 2023, net sales increased 8% year over year and 12% on an organic basis. The rise was mainly driven by broad-based growth across all geographic regions, and the Travel Retail channel on strong consumer demand and the rebuilding of distributor inventories.

The company’s overall sales in the United States advanced 4% on a reported and organic basis in the first nine months of fiscal 2023. The rise was driven by volume gains for Woodford Reserve, owing to the rise in distributor inventories, and higher pricing across the Jack Daniel’s portfolio.

The developed international market reported sales growth of 5%, with organic sales rising 13%. The improvement can be attributed to volume gains for the Jack Daniel’s Tennessee Whiskey and Jack Daniel’s RTDs. Additionally, higher pricing for Jack Daniel’s Tennessee Whiskey has aided the results.

The emerging markets registered 18% net sales growth, whereas organic sales improved 26%. This was backed by growth of Jack Daniel’s Tennessee Whiskey in the United Arab Emirates and Brazil, as well as continued double-digit growth of New Mix in Mexico.

Net sales in the Travel Retail channel advanced 48% on a reported basis and 52% on an organic basis due to higher volumes for the majority of its portfolio, as travel trends continued to rebound.

Headwinds to Overcome

Brown-Forman is witnessing higher input costs and supply-chain disruptions. It also continues to witness higher advertising expenses due to continued investments in its brands.

Brown-Forman succumbed to soft bottom-line performance in third-quarter fiscal 2023, driven by elevated costs, inflation and currency headwinds, which weighed on its margins. The company’s gross margin declined due to the impacts of input cost inflation, elevated costs, resulting from supply-chain disruptions, and adverse currency rates.

Despite cost management initiatives, advertising expenses increased 16% year over year in third-quarter fiscal 2023. On an organic basis, advertising expenses advanced 23%. The increase was driven by elevated marketing spends in the United States to back growth of Jack Daniel’s Tennessee Whiskey, Herradura, Woodford Reserve and the launch of the Jack Daniel’s Bonded series. SG&A expenses rose 14% year over year and on an organic basis, mainly on higher compensation-related expenses, rising discretionary spending and the acquisition, and integration costs for the Gin Mare and Diplomatico brands.

Stocks to Consider

We have highlighted three better-ranked stocks from the Consumer Staples sector, namely Coca-Cola FEMSA KOF, The Duckhorn Portfolio NAPA and Vita Coco Company COCO.

Coca-Cola FEMSA produces, markets and distributes soft drinks throughout the metropolitan area of Mexico City in Southeastern Mexico and the metropolitan region in Buenos Aires, Argentina. KOF has a trailing four-quarter earnings surprise of 36.5%, on average. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today's Zacks #1 Rank stocks here.

Shares of Coca-Cola FEMSA have rallied 49.1% in the past year. The Zacks Consensus Estimate for Coca-Cola FEMSA’s current financial-year sales and earnings suggests growth of 13.4% and 7.8%, respectively, from the year-ago period's reported figures. KOF has an expected EPS growth rate of 12% for three to five years.

Duckhorn is the premier producer of wines, principally in North America. It currently carries a Zacks Rank #2 (Buy). The company has an expected EPS growth rate of 6.6% for three to five years. Shares of Duckhorn have declined 18.4% in the past year.

The Zacks Consensus Estimate for Duckhorn’s fiscal 2023 sales and earnings suggests growth of 8.4% and 1.6%, respectively, from the year-ago period’s reported figures. NAPA has a trailing four-quarter earnings surprise of 13.5%, on average.

Vita Coco provides coconut water products under the Vita Coco brand name in the United States, Canada, Europe, the Middle East, and the Asia Pacific. COCO currently has a Zacks Rank #2. The company has a trailing four-quarter negative earnings surprise of 21.7%, on average. Shares of COCO have rallied 143.2% in the past year.

The Zacks Consensus Estimate for Vita Coco’s current financial-year sales and earnings suggests growth of 10% and 178.3%, respectively, from the year-ago period’s reported figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Brown-Forman Corporation (BF.B) : Free Stock Analysis Report

Vita Coco Company, Inc. (COCO) : Free Stock Analysis Report

Coca Cola Femsa S.A.B. de C.V. (KOF) : Free Stock Analysis Report

The Duckhorn Portfolio, Inc. (NAPA) : Free Stock Analysis Report