Yahoo Finance

Yahoo Finance Here's Why Investors Should Retain Restaurant Brands (QSR)

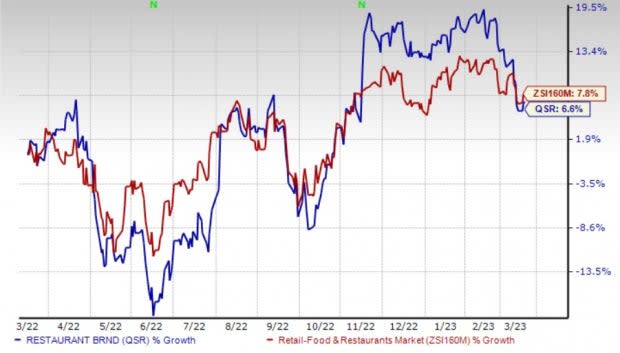

Restaurant Brands International Inc. QSR continues to benefit from robust comparable sales, menu innovations, expansion efforts and digitalization. The company also has an impressive long-term earnings growth rate of 8.3%. In the past six months, the company’s shares have gained 6.6% compared with the industry’s increase of 7.8%. However, high costs are hurting the company.

Let’s delve deeper.

Factors Driving Growth

The company impressed investors with solid comps. In 2022, the company’s consolidated comparable sales increased 60 basis points (bps) to 8.5% from 2021 end. Comps in Popeyes and Burger King reflected growth of 180 bps and 40 bps, respectively, on a year-over-year basis.

The upside was primarily driven by menu innovation, solid promotions for its core platform, and a rise in delivery and digital sales. Also, sequential improvements at Burger King, Popeyes and Firehouse Subs home markets are added positives.

Restaurant Brands believes that there is a huge opportunity to grow all its brands around the world by expanding its presence in existing markets as well as entering new markets. During the third quarter of 2022, the company opened four locations in India, and registered growth in the Middle East, Philippines, Mexico and Monterrey. It also opened restaurants in Houston and Texas.

In fourth-quarter 2022, the company opened about 700 new restaurants in international markets. QSR intends to evaluate opportunities to ramp up international development by establishing master franchisees with exclusive development rights and joint ventures with new and existing franchisees.

The company is also gaining from expansion of delivery via digital platform. QSR’s performance has been primarily driven by attributes such as growth in delivery, an increase in mobile order and pay as well as continued traction in the loyalty program. The company remains optimistic about growth of digital sales in international markets, backed by various service modes.

This Zacks Rank #3 (Hold) company continues to focus on improving its level of service through comprehensive training, improved restaurant operations, reimaging efforts and attractive menu options to enhance overall guest satisfaction and thereby drive comps. Restaurant Brands believes that new product development is a key driver of long-term success for its brands and will continue to be in focus.

Image Source: Zacks Investment Research

Concerns

A rise in labor and commodity costs continues to hurt the company. The industry players expect to witness higher costs due to labor and supply-chain shortages for quite some time. The company has been witnessing labor challenges in a handful of markets.

In 2022, total costs of sales came in at $2,312 million, up from $1890 million reported in the prior-year quarter.

In the past 30 days, earnings estimates for 2023 have witnessed downward revision of 1% to $2.99 per share. In 2023, the company’s earnings are likely to witness a decline of 4.8% year over year.

Zacks Rank & Key Picks

Some better-ranked stocks in the Zacks Retail – Restaurants industry are Chuy's Holdings, Inc. CHUY, Arcos Dorados Holdings Inc. ARCO and Brinker International, Inc. (EAT).

Chuy’s Holdings currently sports a Zacks Rank #1 (Strong Buy). CHUY has a trailing four-quarter earnings surprise of 19.1%, on average. Shares of CHUY have increased 26.4% in the past year. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Chuy’s Holdings’ 2023 sales and EPS suggests growth of 10.8% and 16.1%, respectively, from the year-ago period’s levels.

Arcos Dorados carries a Zacks Rank #2 (Buy). ARCO has a long-term earnings growth of 11.6%. Shares of the company have increased 9.8% in the past year.

The Zacks Consensus Estimate for Arcos Dorados’ 2023 sales and EPS suggests growth of 8.1% and 4.2%, respectively, from the year-ago period’s levels.

Brinker carries a Zacks Rank #2. EAT has a long-term earnings growth rate of 7.1%. The stock has gained 8.4% in the past year.

The Zacks Consensus Estimate for Brinker’s 2024 sales and EPS suggests growth of 3.9% and 36.5%, respectively, from the year-ago period’s levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Brinker International, Inc. (EAT) : Free Stock Analysis Report

Chuy's Holdings, Inc. (CHUY) : Free Stock Analysis Report

Arcos Dorados Holdings Inc. (ARCO) : Free Stock Analysis Report

Restaurant Brands International Inc. (QSR) : Free Stock Analysis Report