Yahoo Finance

Yahoo Finance Here's Why Merchants Bancorp (MBIN) Stock is Worth Betting on

Merchants Bancorp MBIN is well-positioned for growth on its diversified client base and revenue streams, strong liquidity and capital base. Moreover, a decent loan pipeline and initiatives to reduce interest rate risks are positives.

Over the past week, the Zacks Consensus Estimate for 2024 and 2025 earnings has remained unchanged at $6.38 and $6.14, respectively. MBIN currently sports a Zacks Rank #1 (Strong Buy).

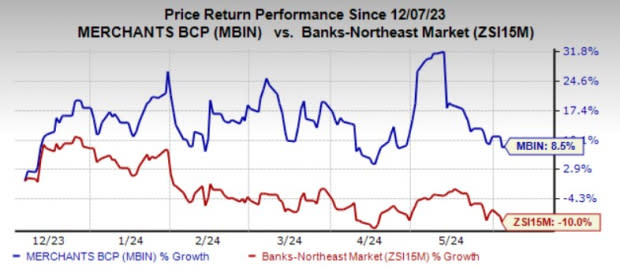

Over the past six months, shares of Merchants Bancorp have gained 8.5% against the industry’s decline of 10%.

Image Source: Zacks Investment Research

Let’s dive deeper into the reasons that make MBIN stock a lucrative bet now.

Earnings Growth: Merchants Bancorp witnessed earnings growth of 34.32% over the past three to five years, significantly outperforming the industry average of 6.76%. This was driven by an expanding top line and prudent initiatives to reduce interest-rate risk.

Also, the company has an impressive earnings surprise history. Its earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, with the average beat being 18.48%.

The Zacks Consensus Estimate for earnings indicates 13.1% growth on a year-over-year basis in 2024.

Revenue Strength: Driven by continued growth in non-interest income and net interest income, Merchant Bancorp’s revenues witnessed a compound annual growth rate (CAGR) of 35% over the last four years (2019-2023). The trend continued in the first quarter of 2024 as well. Organic growth measures and a healthy loan pipeline are likely to aid top-line expansion. Net loans and total deposits witnessed a CAGR of 35.4% and 26.6%, respectively, over the last four years ended 2023. The uptrend continued for both metrics in the first quarter of 2024.

Further, diversified revenues and client base, alongside an emphasis on well-collateralized and affordable multi-family housing, are likely to keep revenue growth healthy in the near term.

The Zacks Consensus Estimate for revenues indicates 16.5% and 2.7% growth in 2024 and 2025, respectively.

Strong Balance Sheet: As of Mar 31, 2024, MBIN’s total cash and cash equivalents (comprising cash and due from banks and interest-earning demand deposits) were $508.8 million and other liabilities were $190.5 million. Hence, a solid liquidity position allows the company to address its near-term obligations.

Further, tier 1 risk-based capital ratio and common equity tier-1 capital ratio were pegged at 11.1% and 7.8% as of the same date, well above regulatory requirements of 8.5% and 7%, respectively. This will enable the company to withstand any economic deterioration and absorb losses.

Stock Seems Undervalued: MBIN’s price-to-cash-flow and price-to-earnings (F1) ratios of 5.99 and 6.13 are well below the industry average of 7.83 and 9.96. Thus, the stock seems to be available at a better valuation than its peers.

Superior Return on Equity (ROE): Merchant Bancorp’s trailing 12-month ROE reflects its superiority in terms of utilizing shareholders’ funds. The company’s ROE of 26.65% compares favorably with 8.61% of the industry.

Other Stocks to Consider

Some other top-ranked stocks from the banking space worth a look are FB Financial Corporation FBK and Princeton Bancorp, Inc. BPRN, each sporting a Zacks Rank #1 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for FBK’s current-year earnings has been revised marginally upward over the past week. Shares of the company have lost 1% in the past six months.

The Zacks Consensus Estimate for BPRN’s 2024 earnings has been revised marginally higher over the past 60 days. Over the past six months, shares of the company have lost 12.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

FB Financial Corporation (FBK) : Free Stock Analysis Report

Merchants Bancorp (MBIN) : Free Stock Analysis Report

Princeton Bancorp, Inc. (BPRN) : Free Stock Analysis Report