Yahoo Finance

Yahoo Finance Here's Why PaySauce Limited's (NZSE:PYS) CEO Compensation Is The Least Of Shareholders Concerns

Key Insights

PaySauce to hold its Annual General Meeting on 14th of September

CEO Asantha Wijeyeratne's total compensation includes salary of NZ$213.7k

Total compensation is 60% below industry average

Over the past three years, PaySauce's EPS grew by 48% and over the past three years, the total loss to shareholders 42%

Shareholders may be wondering what CEO Asantha Wijeyeratne plans to do to improve the less than great performance at PaySauce Limited (NZSE:PYS) recently. At the next AGM coming up on 14th of September, they can influence managerial decision making through voting on resolutions, including executive remuneration. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. In our opinion, CEO compensation does not look excessive and we discuss why.

View our latest analysis for PaySauce

Comparing PaySauce Limited's CEO Compensation With The Industry

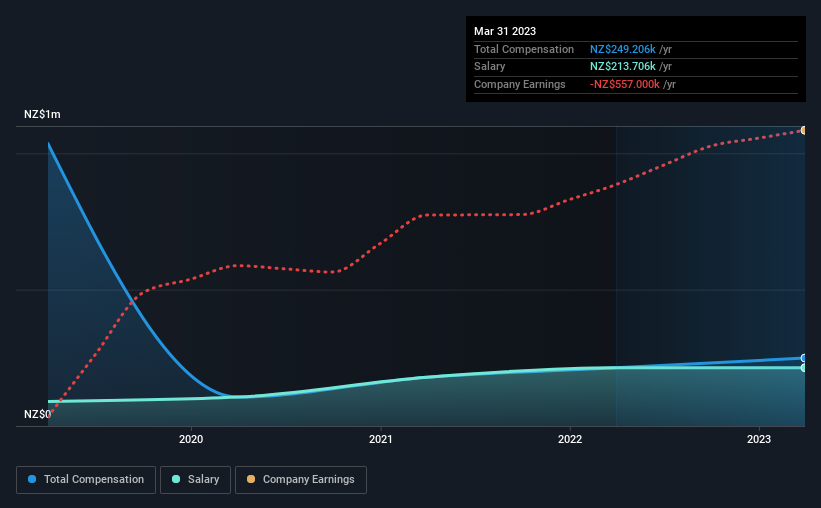

Our data indicates that PaySauce Limited has a market capitalization of NZ$31m, and total annual CEO compensation was reported as NZ$249k for the year to March 2023. We note that's an increase of 17% above last year. In particular, the salary of NZ$213.7k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the New Zealand Professional Services industry with market capitalizations under NZ$340m, the reported median total CEO compensation was NZ$623k. In other words, PaySauce pays its CEO lower than the industry median. Furthermore, Asantha Wijeyeratne directly owns NZ$6.1m worth of shares in the company, implying that they are deeply invested in the company's success.

Component | 2023 | 2022 | Proportion (2023) |

Salary | NZ$214k | NZ$213k | 86% |

Other | NZ$36k | - | 14% |

Total Compensation | NZ$249k | NZ$213k | 100% |

On an industry level, around 71% of total compensation represents salary and 29% is other remuneration. According to our research, PaySauce has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

PaySauce Limited's Growth

PaySauce Limited's earnings per share (EPS) grew 48% per year over the last three years. It achieved revenue growth of 65% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. Most shareholders would be pleased to see strong revenue growth combined with EPS growth. This combo suggests a fast growing business. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has PaySauce Limited Been A Good Investment?

The return of -42% over three years would not have pleased PaySauce Limited shareholders. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

The loss to shareholders over the past three years is certainly concerning. The share price trend has diverged with the robust growth in EPS however, suggesting there may be other factors that could be driving the price performance. A key question may be why the fundamentals have not yet been reflected into the share price. The upcoming AGM will provide shareholders the opportunity to raise their concerns and evaluate if the board’s judgement and decision-making is aligned with their expectations.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. In our study, we found 3 warning signs for PaySauce you should be aware of, and 1 of them makes us a bit uncomfortable.

Switching gears from PaySauce, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.