Yahoo Finance

Yahoo Finance Lam Research Corp (LRCX) Reports Q3 2024 Earnings: Surpasses Analyst Revenue Forecasts

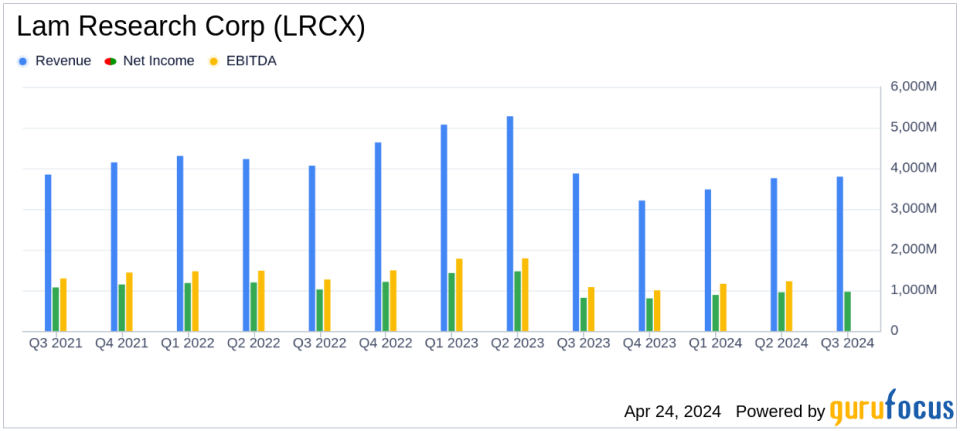

Revenue: Reported at $3.79 billion, surpassing estimates of $3.72 billion.

Net Income: Achieved $966 million, exceeding estimates of $963.16 million.

Earnings Per Share (EPS): U.S. GAAP diluted EPS reached $7.34, slightly above the estimated $7.30.

Gross Margin: U.S. GAAP gross margin improved to 47.5% from 46.8% in the previous quarter, indicating a 70 basis points increase.

Operating Income: U.S. GAAP operating income as a percentage of revenue slightly decreased to 27.9% from 28.1% quarter-over-quarter.

Cash Flow: Generated $1,385 million from operating activities, demonstrating robust operational efficiency.

Share Repurchases and Dividends: Returned $981 million to shareholders through repurchases and paid $263 million in dividends.

Lam Research Corp (NASDAQ:LRCX) released its 8-K filing on April 24, 2024, detailing its financial results for the quarter ended March 31, 2024. The company reported revenue of $3.79 billion, surpassing the analyst estimate of $3.72 billion. The U.S. GAAP diluted EPS stood at $7.34, also exceeding the expected $7.30 per share. These results highlight Lam Research's robust performance in a competitive semiconductor industry landscape.

Lam Research, a leading global supplier of semiconductor wafer fabrication equipment, specializes in deposition and etch processes crucial for semiconductor manufacturing. The company's technology is pivotal in producing smaller, more efficient devices, serving top global chipmakers like TSMC, Samsung, Intel, and Micron.

Financial Highlights and Strategic Positioning

For the March 2024 quarter, Lam Research reported a U.S. GAAP gross margin of 47.5% and an operating income of 27.9% of revenue. Non-GAAP figures were also strong, with a gross margin of 48.7% and an operating income of 30.3% of revenue. These metrics demonstrate Lam's ability to maintain profitability and operational efficiency amidst market fluctuations.

President and CEO Tim Archer commented on the results, stating, "With solid revenue and earnings per share performance in the March quarter, Lam is off to a strong start in calendar 2024. As our customers address the challenges in scaling semiconductors to meet the power and speed requirements for driving AI transformation, Lam is strengthening its leadership and is well-positioned for the significant opportunities ahead."

Operational and Geographic Breakdown

Lam's revenue sources are well-diversified geographically, with significant contributions from China (42%), Korea (24%), and balanced inputs from Japan, Taiwan, the United States, Southeast Asia, and Europe. This global footprint helps mitigate regional market volatilities and harness growth across various markets.

From a product perspective, systems revenue, which includes sales of new leading-edge equipment, was reported at approximately $2.40 billion. Customer support-related revenue, comprising service, spares, upgrades, and non-leading-edge equipment, contributed around $1.40 billion, underscoring the company's strong after-market support and recurring revenue streams.

Future Outlook and Investor Considerations

Looking forward, Lam Research provided guidance for the June 2024 quarter, projecting revenue of approximately $3.8 billion and a U.S. GAAP gross margin of 46.7%. The non-GAAP EPS is expected to be around $7.50, reflecting ongoing operational excellence and market leadership.

The company's balance sheet remains robust with cash and cash equivalents increasing to $5.7 billion, up from $5.6 billion in the previous quarter, driven by strong cash flows from operations which totaled $1.385 billion for the quarter.

Lam Research's consistent performance, strategic market positioning, and forward-looking management practices make it a noteworthy entity in the semiconductor equipment sector, offering potential value to investors and industry stakeholders alike.

For detailed financial tables and further information, visit Lam Researchs investor relations website.

Explore the complete 8-K earnings release (here) from Lam Research Corp for further details.

This article first appeared on GuruFocus.