Yahoo Finance

Yahoo Finance Nu Skin (NUS) Troubled by Customer Acquisition Challenges

Nu Skin Enterprises, Inc. NUS appears in troubled waters. The company has been battling persistent macroeconomic headwinds across most regions, which has affected customer and affiliate acquisition.

Additionally, greater-than-expected foreign currency headwinds weighed on Nu Skin's first-quarter 2024 performance. Management expects the global macro landscape to remain difficult in the near term, leading to a drab 2024 view. The Zacks Consensus Estimate for 2024 earnings per share has declined from $1.13 to $1.10 over the past 60 days.

Macroeconomic Hurdles Persist

Nu Skin has been encountering persistent macroeconomic obstacles, which continued in the first quarter of 2024. The company’s performance was hurt by continuous macroeconomic headwinds across most regions, including inflationary pressure on consumer spending for premium products. This, along with price hikes, has affected the company’s customer and affiliate acquisition.

Quarterly revenues of $417.3 million tumbled 13.3% year over year in the first quarter. On a constant-currency basis, revenues fell 9.5%. Sales leaders were down 12% year over year to 38,609. Nu Skin’s customer base dropped 19% to 875,261. The company’s paid affiliates were down 30% to 154,171. On an adjusted basis, paid affiliates tumbled 14%.

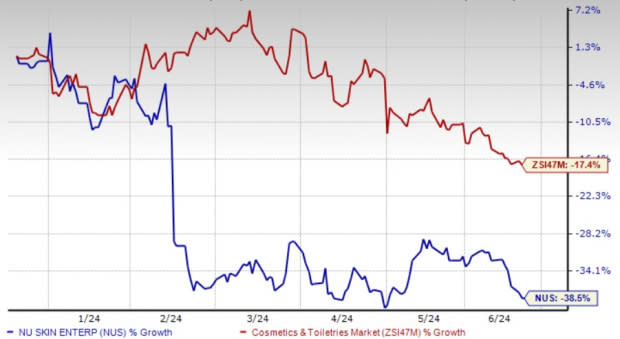

Image Source: Zacks Investment Research

Volatile Currency Movements

Nu Skin’s strong international presence exposes it to the risk of volatile currency movements as any adverse currency fluctuation is likely to weigh on the company’s operating performance. Nu Skin’s first-quarter 2024 revenues witnessed greater-than-expected adverse currency effects. First-quarter revenues included a negative impact of 3.8% from foreign currency fluctuations. The company envisions unfavorable foreign currency impacts of 2-3% on 2024 revenues and of 4-3% on second-quarter revenues.

What’s Ahead?

Nu Skin's business continues to bear the brunt of macroeconomic challenges. Management expects macroeconomic hurdles to persist in the near to mid-term. Given the lingering economic challenges and hurdles related to business transformation and foreign currency volatility, Nu Skin reaffirmed its drab view for 2024 on its first-quarter earnings call.

Nu Skin anticipates revenues in the band of $1.73-$1.87 billion for 2024, which suggests a 12-5% decline from the year-ago period’s reported figure. Management envisions an adjusted EPS of 95 cents to $1.35. The projection implies a decline from adjusted earnings of $1.85 recorded in 2023. Nu Skin’s bottom-line view reflects expectations of an increased global tax rate.

For the second quarter of 2024, Nu Skin expects revenues between $420 million and $455 million, which suggests a decline of 16% to 9% from the year-ago quarter’s reported level. Nu Skin expects adjusted earnings of 10-20 cents a share for the second quarter compared with the year-ago period’s figure of 54 cents.

While a focus on the Nu Vision 2025 strategy, effective product launches and the strength of the Rhyz business bode well, the aforementioned hurdles cannot be ignored for now. Shares of the Zacks Rank #4 (Sell) company have tumbled 38.5% in the past six months compared with the industry’s decline of 17.4%.

3 Solid Consumer Staple Bets

Vital Farms Inc. VITL offers a range of produced pasture-raised foods. It currently sports a Zacks Rank #1 (Strong Buy). VITL has a trailing four-quarter average earnings surprise of 102.1%. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Vital Farms’ current financial-year sales and earnings indicates growth of 22.5% and 59.3%, respectively, from the year-ago reported numbers.

Utz Brands Inc. UTZ, which manufactures a diverse range of salty snacks, currently carries a Zacks Rank #2 (Buy). UTZ has a trailing four-quarter earnings surprise of 2%, on average.

The consensus estimate for Utz Brands’ current financial-year earnings indicates growth of 26.3% from the year-ago reported numbers.

Ingredion Incorporated INGR, which manufactures and sells sweeteners, starches, nutrition ingredients, and biomaterial solutions, currently carries a Zacks Rank of 2. The Zacks Consensus Estimate for INGR’s current fiscal-year earnings indicates growth of 3.6% from the year-ago reported figure.

Ingredion Incorporated has a trailing three-quarter earnings surprise of 10.1%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ingredion Incorporated (INGR) : Free Stock Analysis Report

Nu Skin Enterprises, Inc. (NUS) : Free Stock Analysis Report

Vital Farms, Inc. (VITL) : Free Stock Analysis Report

Utz Brands, Inc. (UTZ) : Free Stock Analysis Report