Yahoo Finance

Yahoo Finance Pfizer: An Oversold Pharma Stock in Recovery

Some say the art of investing is the ability of catching falling knives. Pfizer Inc. (NYSE:PFE) shares have sold off in 2023 and represent an attractive opportunity after having likely bottomed out.

Attractive opportunity despite poor stock performance

The pharmaceutical company's dividend yield of approximately 5.80% naturally draws the attention of the market and seasoned investors alike. Approximately $9 billion is spent by the company in dividend payments per year, despite a free cash flow of only $4.80 billion in 2024 - meaning the free cash flow is now unable to meet the dividend payments after a sharp decline from the 2021 ($29.90 billion) and 2022 ($26 billion) levels boosted by Covid-19 vaccine sales.

The abnormally high dividend yield is explained by two factors. First, Pfizer increased its dividend payments during the pandemic without reducing them afterward. Second, the stock sharply sold off in 2023 (40% drop). The stock action of last year mechanically caused the dividend yield to go up, without the company having to increase its dividend payments.

The stock sold off in 2023 as the Covid-19 pandemic came under control and vaccine sales plummeted. Revenue, earnings, free cash flow and practically every financial metric plunged in 2023 and caused shareholders to sell their shares. The company had focused much of its resources for two years in developing and commercializing the vaccine, which led it to accumulating large amounts of cash. The cash has massively been invested in share buybacks (to the point that the latter are now unlikely in the next couple of years), paid out in generous dividends to the shareholders and this Covid era cash continues to support an attractive pipeline that is likely to boost the company's revenue and diversify its cash generation sources.

The stock is, therefore, an attractive turnaround investment, as its pipeline is being regenerated.

Attractive pipeline and potential growth catalysts

Looking ahead, Pfizer has a drug treating Duchenne muscular dystrophy in Phase 3 clinical trials. The drug could turn into a real growth catalyst for the company, given the DMD drugs market is expected to grow at an impressive 33% rate per year in the next 10 years.

No direct competitor of Pfizer has the Food and Drug Administration's approval for any DMD drugs. The only company that currently has a head start is Sarepta Therapeutics Inc. (NASDAQ:SRPT). However, Sarepta is a much smaller pharma company with a market cap of $12 billion (Pfizer's is currently around $160 billion). Therefore, its financial resources are extremely limited. A direct acquisition of Sarepta by Pfizer is also not out of the question. As a matter of fact, Pfizer currently has the equivalent of Sarepta's market cap in cash and short-term investments. Tactical acquisitions like this one could guarantee the company dominance in various niches thanks to the available cash from the pandemic revenue.

Indeed, Pfizer's large financial resources guarantee the company options in relation to the future. It can invest in new drugs and it can buy smaller companies with promising pipelines. The company is also well established and has significantly more experience with the FDA's approval processes. In the pharmaceutical industry, time is a crucial component. A swifter FDA process means the company saved months (if not years) in the commercialization and revenue making of a drug. In addition to the cash generated during the time that was saved by the company, the first-mover advantage is an important one in a sector where doctors and patients tend to stick with the drug they know works.

Last but not least, on May 16, Pfizer announced the acquisition of an oncology drug company Seagen Inc. (SGEN) for $43 billion. The company had to increase its debt by $31 billion (practically doubling its total indebtedness to $61 billion). Of course, investors are worried that large debts in the current interest rate environment is dangerous. However, this is likely a good bet from management to boost the company's growth prior to interest rate cuts (which would push the valuation of Seagen up).

Seagen has 31 oncology drugs under development and will bring $2 billion of revenue to Pfizer. These 31 drugs ensure a long and wide pipeline, which the company has been lacking since the Covid years.

Financials and valuation

Shares of Pifzer have been under severe pressure because its financials have declined sharply since 2022. However, when we zoom out, it becomes clear that the company is merely returning to pre-pandemic levels after two exceptional (in all meanings of the word) years due to a unique global health situation.

While revenue is now above the pre-Covid levels, Ebitda and net income have dropped too quickly. The latter two metrics have dropped because revenue fell quickly and the costs induced by a high inflationary environment have risen. This combination caused a mechanical reaction of profit squeeze, which is unlikely to be sustained as inflation stabilizes and Pfizer's revenue sources diversify away from Covid vaccines.

Indeed, from a forecast standpoint, the near future looks bright. While revenue will witness only mild growth in the next four years, Ebitda is estimated to rise by 36% this year to reach $21.20 billion, up from 2023's $15.60 billion, and puts the company back to pre-pandemic levels. It is a similar story for free cash flow, which is probably the main reason for the sell-off in 2023. At that time, shareholders feared the drop of FCF to $4.80 billion, i.e., below the yearly dividend payment of $9 billion, would force the company to cut its generous dividend. However, FCF is forecasted to reach $10.70 billion in 2024 (enough to cover the dividend payments), to accelerate to $14.60 billion in 2025 and continue its rise to $18.60 billion in 2027. These estimates are reassuring as all the company needs to do is wait for the financial recovery: the cash it holds is absolutely sufficient to not have to cut dividend payments and even to pursue its merger and acquisition strategy.

From a valuation standpoint, the stock is highly attractive in light of the profitability rise in the next few years.

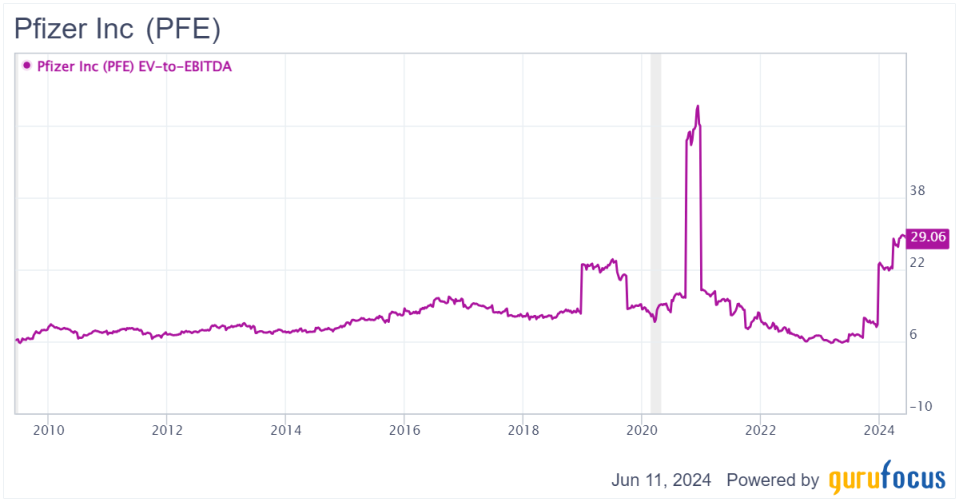

While the valuation has returned to 2013 to 2018 levels (note the rising trendline of the stock's valuation over time), it is likely that it will resume its rising valuation trend as its profitability continues to grow. Indeed, the stock is currently valued at around 10 times forward Ebitda and, in light of the rapid recovery, its pipeline and its M&A strategy, it is likely that Pfizer's shares could rise by double-digit levels annually over the next several years.

Risk factors to my case

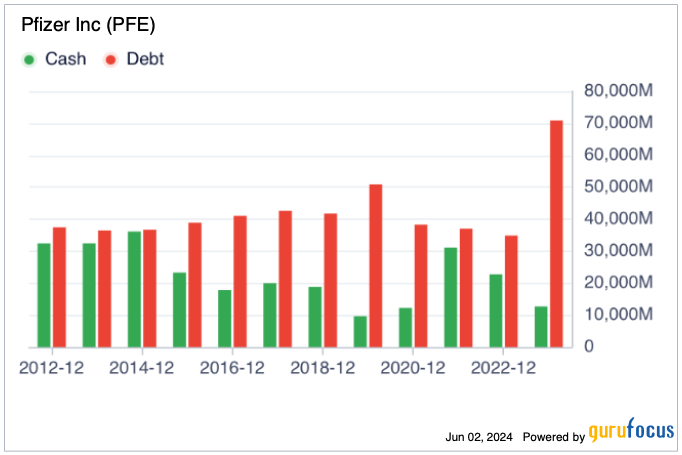

There are, however, a few risk factors to consider. The first is its debt levels: the declining cash and rising debt could cause financial strain on the company.

The unfortunate part of the debt problem is that this downward cycle for the company occurs in a tight monetary policy and high interest rate environment. Potential new debt financings and refinancings can cause further pressure, especially if the U.S. central bank decides to stay high for much longer than expected, as inflation seems to remain sticky.

However there are mitigants to the company's indebtedness risk. The excellent notation of Pfizer, rated A, A2 and A by Standard & Poor's, Moody's and Fitch respectively, allows the company to refinance its debt in the most competitive terms with banks. But more than the notation, one needs to analyze the use of the debt. When a company contracts debt to finance its operations, it is usually a red flag for a value investor. In the case of Pfizer, the company doubled its debt to acquire Seagen, which brings along its revenue and, most importantly, its promising pipeline that could generate additional cash to repay the debt. From a macroeconomic level, it is unlikely the Fed will keep the high interest rate environment in 2025 as the tight monetary policy is clearly showing signs of weakening in inflation.

Another risk factor to consider is the dividend it pays. Many shareholders left the boat in 2023, causing the stock to decline and its dividend yield to rise. One of the buy side's upward pressures is precisely its attractive dividend yield. If Pfizer's management fails to ensure the financial turnaround of the company, it might have to slash its generous dividend payments and that could cause a further sell-off. However, as we saw, the large cash buffer accumulated from the Covid vaccine sales is likely sufficient for management to not have to choose that path.

Bottom line

The stock has an attractive risk-reward ratio at this point in time. Despite fears of slashed dividend payments, they are unlikely to occur as they didn't happen in 2023 when the company was struggling financially. Further, the free cash flow in 2024 is expected to cover the dividend payments and even generate additional cash. 2025's acceleration in free cash flow would put the company in comfortable cash levels, and the expected interest rate cuts of the end of this year and next would likely release the company from some of its current financial headaches.

Given the attractive dividend yield, the growth catalysts and its expected financial growth in the next few years, the stock may be a good opportunity for any investor wishing to have some exposure to the pharmaceutical sector.

This article first appeared on GuruFocus.