Yahoo Finance

Yahoo Finance Should You Retain Crown Castle Stock in Your Portfolio Now?

Crown Castle CCI owns a portfolio of wireless communication infrastructure assets in the United States. It is well-poised to benefit from the increase in mobile data usage, spectrum availability and high capital spending by wireless carriers to deploy 4G and 5G networks amid incremental customer demand. However, customer concentration and consolidation in the wireless industry are key concerns for the company. High interest rates add to its woes.

What’s Supporting CCI?

The exponential growth in mobile data usage, higher availability of spectrum and deployment of 5G networks at scale are driving significant network investments by carriers who aim to improve and densify their cell sites. Moreover, wireless data consumption is expected to increase considerably over the next several years.

This is likely to be driven by the advent of next-generation technologies, including edge computing functionality, autonomous vehicle networks and the Internet of Things and the rampant usage of network-intensive applications for video conferencing, cloud services and hybrid-working scenarios.

Given Crown Castle’s unmatched portfolio of more than 40,000 towers in each of the top 100 basic trading areas of the United States and approximately 90,000 route miles of fiber (as of the second quarter of 2024), it remains well-positioned to capitalize on this upbeat trend.

The company’s investments in the fiber and small cell business on the back of acquisitions, constructions and new deployments complement its tower business and offer meaningful upside potential to its 5G growth strategy. Management remains on track to deliver 2024 organic revenue growth of 4.5% in towers, 2% in fiber solutions and double digits in small cells, adjusted for the impact of Sprint Cancellations.

Crown Castle is focused on maintaining a decent balance sheet position with sufficient liquidity. The company exited the second quarter of 2024 with cash and cash equivalents of $155 million. As of June 30, 2024, the net debt to last quarter’s annualized adjusted EBITDA was 5.39X. It has only 8% of its debt maturing through 2025, with a weighted average term-to-maturity of seven years. With investment-grade credit ratings of BBB, BBB+ and Baa3 from Standard & Poor’s, Fitch, and Moody’s, respectively, CCI is well-poised to capitalize on long-term growth opportunities.

Solid dividend payouts are arguably the biggest enticement for REIT shareholders, and Crown Castle is committed to that. The company’s dividends are supported by high-quality, long-term contracted lease payments, and it benefits from being a provider of mission-critical shared communication infrastructure assets. CCI has increased its dividend four times in the last five years, and its five-year annualized dividend growth rate is 7.66%. Check Crown Castle’s dividend history here.

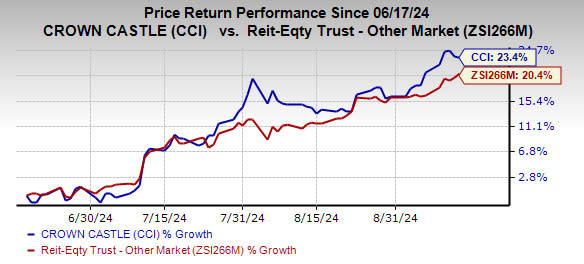

Over the past three months, shares of this Zacks Rank #3 (Hold) company have gained 23.4% compared with the industry’s upside of 20.4%.

Image Source: Zacks Investment Research

What’s Hurting CCI?

Customer concentration is very high for Crown Castle. As of June 30, 2024, around three-fourths of the company’s site rental revenues were derived from T-Mobile (35%), Verizon (19%) and AT&T (20%). A loss of any of these customers or consolidation among them will significantly affect the company’s top line. Moreover, any pullback or rationalization in network spending by carriers might affect Crown Castle’s performance.

Crown Castle has a substantially leveraged balance sheet and a significant amount of debt relative to its cash flows. The company’s debt and other long-term obligations aggregated $22.85 billion as of June 30, 2024. Moreover, in an elevated interest rate environment, additional borrowings to fund near-term capital expenditures will not only inflate the company’s debt but also raise the cost of borrowings.

Management expects incurring net interest expense and amortization of deferred financing costs between $926 million and $971 million in 2024. Our estimate indicates a year-over-year rise of 9.3% in the company’s current-year interest expenses. Further, with high interest rates still in place, the dividend payout might seem less attractive than the yields on fixed-income and money market accounts.

Stocks to Consider

Some better-ranked stocks from the broader REIT sector are Cousins Properties CUZ and Lamar Advertising LAMR, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Cousins Properties’ 2024 FFO per share has moved marginally northward over the past two months to $2.66.

The Zacks Consensus Estimate for Lamar Advertising’s current-year FFO per share has been raised marginally over the past two months to $8.09.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Crown Castle Inc. (CCI) : Free Stock Analysis Report

Lamar Advertising Company (LAMR) : Free Stock Analysis Report

Cousins Properties Incorporated (CUZ) : Free Stock Analysis Report