Yahoo Finance

Yahoo Finance Should You Retain Franklin (BEN) for 5.2% Dividend Yield?

Investors seeking attractive dividend yields amid the current uncertain macroeconomic environment can consider Franklin Resources, Inc. BEN, a fundamentally solid investment manager.

The majority of BEN’s operating revenues and net income is derived from offering investment management and related services to retail mutual funds, and institutional and high-net-worth investors in jurisdictions worldwide.

It announced a 3.3% hike in the common stock dividend to 31 cents in December 2023.

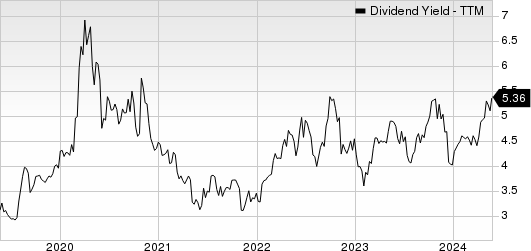

In the past five years, BEN raised its dividend five times, with an annualized dividend growth rate of 3.5%. Considering the last day’s closing price of $23.13, the company’s dividend yield currently stands at 5.22%. This is impressive compared with the industry’s average of 1.90% and attractive for investors as it represents a steady income stream.

Franklin Resources, Inc. Dividend Yield (TTM)

Franklin Resources, Inc. dividend-yield-ttm | Franklin Resources, Inc. Quote

Dividend aside, the company has a share repurchase program in place. In December 2023, Franklin announced a repurchase authorization of 27.2 million shares of its common stock. This is in addition to the existing authorization, of which 12.8 million shares were available for repurchase at November 2023 end. It repurchased 0.4 million shares of its common stock for $11.7 million in first-quarter 2024. Such consistent capital distribution activities are likely to stoke investors’ confidence in the stock.

Should one keep an eye on the BEN stock to earn a high dividend yield? Let us check the company's financials to understand the risks and rewards before making any decision.

Franklin has a decent balance sheet. As of Mar 31, 2024, the company had a debt of $3.04 billion, which has declined over the past few quarters. The company’s liquidity (comprising cash and cash equivalents and investments) as of the same date totaled $5.7 billion. Thus, a decent liquidity position and earnings strength reflect a lesser likelihood of defaulting on interest and debt repayments, even if the economic situation worsens, and its ability to sustain dividend payments.

Also, in the past few years, Franklin has grown through acquisitions, thereby enhancing its foothold. In January 2024, the company completed the acquisition of Putnam Investments, a global asset management firm, from Great-West Lifeco. The transaction is expected to accelerate Franklin’s growth in the retirement space by increasing its defined contribution AUM to more than $100 billion. Such efforts will help the company in improving and expanding its alternative investments and multi-asset solutions platforms.

Franklin has been witnessing solid growth in its assets under management (AUM) balance over the years. Though AUM declined in fiscal 2022, it recorded a compounded annual growth rate (CAGR) of 18.7% over the last five fiscal years (ended fiscal 2023). The rising trend continued in first-quarter fiscal 2024. Also, the company’s efforts to diversify its business into asset classes that are seeing growing client demand, such as alternative asset classes, are expected to continue to propel AUM growth.

In the past six months, shares of this Zacks Rank #3 (Hold) company have declined 2.5% against the industry’s rally of 22.2%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Image Source: Zacks Investment Research

Therefore, investors should consider holding this stock to their portfolio as this will help generate robust returns over time.

Other Companies With Solid Dividends

Major regional banking stocks like Truist Financial TFC and Comerica CMA are worth a look, as these, too, have decent dividend yields.

Considering the last day’s closing price, Truist Financial’s dividend yield currently stands at 5.35%. It presently carries a Zacks Rank of 3.

Based on the last day’s closing price, Comerica’s dividend yield currently stands at 5.33%. It carries a Zacks Rank of 3 at present.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Franklin Resources, Inc. (BEN) : Free Stock Analysis Report

Comerica Incorporated (CMA) : Free Stock Analysis Report

Truist Financial Corporation (TFC) : Free Stock Analysis Report