Yahoo Finance

Yahoo Finance SEHK Growth Companies With High Insider Ownership And At Least 12% Revenue Growth

Amidst a backdrop of fluctuating global markets, the Hong Kong stock market continues to present unique opportunities for discerning investors. High insider ownership combined with robust revenue growth can be indicative of management's confidence in a company's future prospects, making such stocks potentially attractive in the current economic climate.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

Name | Insider Ownership | Earnings Growth |

iDreamSky Technology Holdings (SEHK:1119) | 20.1% | 104.1% |

Fenbi (SEHK:2469) | 32.4% | 43% |

Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.5% | 79.3% |

Adicon Holdings (SEHK:9860) | 22.3% | 29.6% |

Tian Tu Capital (SEHK:1973) | 34% | 70.5% |

DPC Dash (SEHK:1405) | 38.2% | 89.7% |

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 100.1% |

Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 76.5% |

Beijing Airdoc Technology (SEHK:2251) | 28.2% | 83.9% |

Lianlian DigiTech (SEHK:2598) | 19.4% | 84.2% |

Below we spotlight a couple of our favorites from our exclusive screener.

BYD

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited operates in the automobile and battery sectors across China, including Hong Kong, Macau, Taiwan, and internationally, with a market capitalization of approximately HK$749.39 billion.

Operations: The company generates revenue primarily from its automobile and battery sectors.

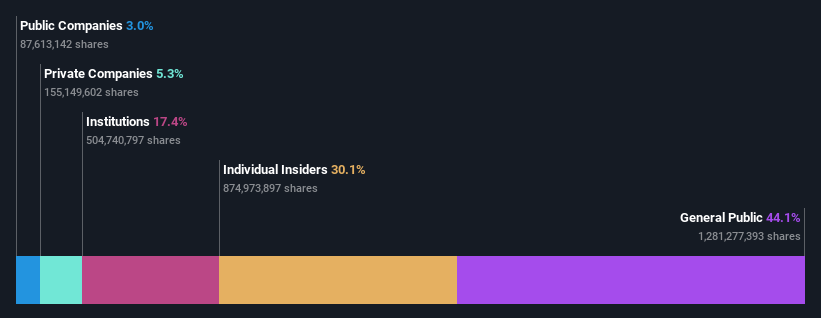

Insider Ownership: 30.1%

Revenue Growth Forecast: 14.0% p.a.

BYD Company Limited, a significant entity in the Hong Kong market, is poised for robust growth with earnings forecasted to grow by 14.84% annually, outpacing the local market's 11.7%. The company's revenue growth is also expected to exceed the market average at 14% per year. Despite these promising figures, growth rates are not considered very high as they fall below the significant threshold of 20%. Additionally, BYD trades at a substantial discount of 22.2% below its estimated fair value and has demonstrated strong revenue and earnings growth over the past year with an impressive increase of 52.7%. This financial health is complemented by strategic expansions such as entering new product markets including launching its first pickup truck internationally.

J&T Global Express

Simply Wall St Growth Rating: ★★★★☆☆

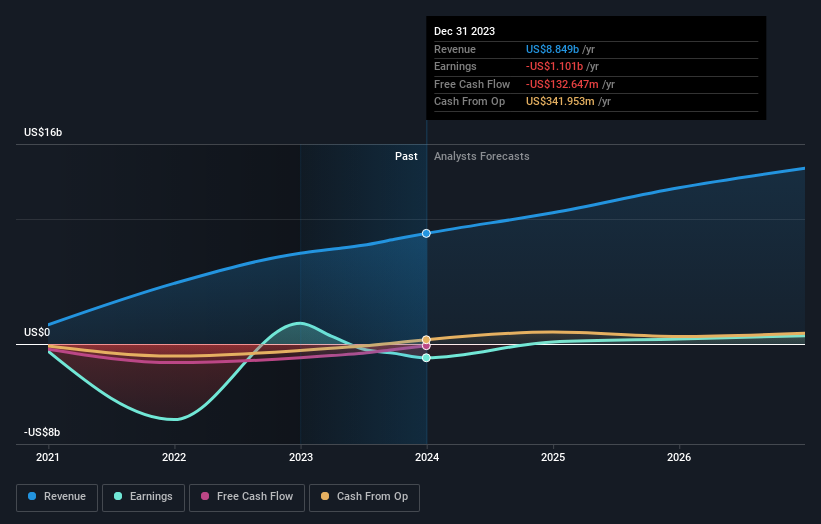

Overview: J&T Global Express Limited, an investment holding company, provides express delivery services and has a market capitalization of approximately HK$73.14 billion.

Operations: The firm generates its revenue primarily from air freight transportation, totaling approximately HK$8.85 billion.

Insider Ownership: 20.2%

Revenue Growth Forecast: 15.9% p.a.

J&T Global Express Limited, a growth-oriented firm in Hong Kong, exhibits promising revenue trends with an annual forecasted increase of 15.9%, surpassing the local market average of 7.8%. Despite a lower-than-benchmark forecasted return on equity at 17.9%, the company's earnings are expected to surge by approximately 102.86% annually. Recent executive changes and substantial parcel volume growth highlight its dynamic operational environment, although it faces challenges in achieving high profitability within three years as per market expectations.

Upon reviewing our latest valuation report, J&T Global Express' share price might be too optimistic.

Meituan

Simply Wall St Growth Rating: ★★★★★☆

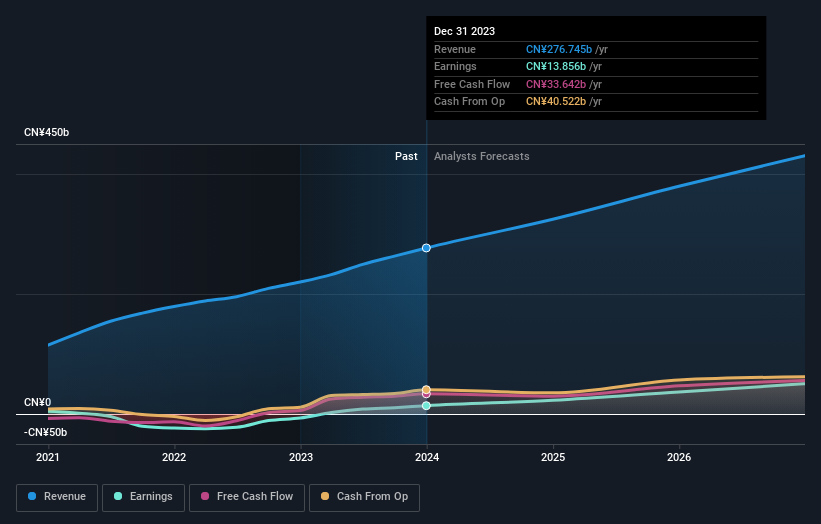

Overview: Meituan is a technology retail company based in the People's Republic of China, with a market capitalization of approximately HK$741.75 billion.

Operations: The company generates its revenue from various technology retail activities within China.

Insider Ownership: 11.4%

Revenue Growth Forecast: 12.7% p.a.

Meituan, a growth company in Hong Kong, is poised for substantial earnings growth at 31.5% annually, outpacing the local market's 11.7%. Despite recent significant insider selling, its revenue growth forecast of 12.7% annually also exceeds the Hong Kong market average of 7.8%. The company's high-quality earnings have been impacted by one-off items but show resilience with a robust return on equity projected at 20.7% in three years. Recent financial reports indicate strong sales and net income increases, affirming its growth trajectory.

Make It Happen

Unlock more gems! Our Fast Growing SEHK Companies With High Insider Ownership screener has unearthed 48 more companies for you to explore.Click here to unveil our expertly curated list of 51 Fast Growing SEHK Companies With High Insider Ownership.

Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Interested In Other Possibilities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1211 SEHK:1519 and SEHK:3690.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com