Yahoo Finance

Yahoo Finance Sysco's (SYY) Operational Efficiency Aids Amid Soft Traffic

Sysco Corporation SYY continues to thrive in the growing food-away-from-home industry. Emphasizing efficiency improvements through supply-chain productivity and prudent cost containment, the company demonstrated strong discipline and adaptability by navigating a soft customer environment in the third quarter of fiscal 2024.

Key Upsides

Sysco has been focused on enhancing efficiency through supply-chain productivity and structural cost-containment efforts. Despite witnessing slow restaurant traffic and soft volumes, Sysco’s operational efficiency led to robust bottom-line growth in the third quarter of fiscal 2024.

Additionally, both the gross profit and the gross margin improved in the third quarter, reflecting the company’s ability to effectively manage product cost fluctuations through tight margin management, driven by strategic sourcing efforts, disciplined and rational pricing, a higher mix of specialty products and improved penetration rates of Sysco brand products in local markets.

Markedly, Sysco witnessed positive operating leverage for the sixth straight time, driven by a faster expansion in the gross profit compared to operating expenses. Management undertook proactive measures to address both variable and structural operating costs, leading to a raised cost-out goal for fiscal 2024. The company targets cost savings of $120 million now compared with the $100 million expected earlier.

Sysco is a diversified company that covers every part of the growing food-away-from-home industry. The food-away-from-home channel has been capturing market share from the grocery channel for a while now, and this macro trend is expected to stay for many years. The food-away-from-home industry is solid and reliable, and Sysco benefits from a diversified customer base that helps mitigate fluctuations in specific segments. This includes strong operations in healthcare, hospitality, education, travel, recreation, and business and industry.

Image Source: Zacks Investment Research

Restaurant Traffic Soft

On its third-quarter fiscal 2024 earnings call, management highlighted that restaurant foot traffic has declined year over year, as observed through credit card transaction data. January restaurant traffic started slow, down in the high single digits year over year due to various factors. February and March saw an improvement, with traffic down to the low single digits, but continued to pose a challenge for distributor case volume growth. Although there was sequential improvement throughout the third quarter, a stronger recovery had been anticipated.

High restaurant menu prices have impacted foot traffic, a concern that needs to be addressed industry-wide to improve affordability for consumers. Apart from this, restaurants continue to face significantly elevated labor costs, while food costs have moderated year over year. Nonetheless, Sysco is committed to supporting its local restaurant customers through several initiatives.

Wrapping Up

Sysco’s extensive range of product offerings, together with the proficiency of Sysco’s sales team, the strength of its supply chain and financial stability, positions it well to achieve impressive outcomes in the short run and even more robust results in the long run. For fiscal 2024, management envisions sales to increase to nearly $79 billion compared with $76.3 billion recorded in fiscal 2023. Adjusted earnings per share or EPS are expected to rise 5-10% to the $4.20-$4.40 band.

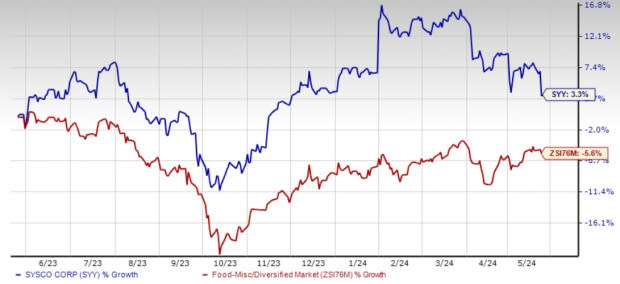

Shares of the Zacks Rank #3 (Hold) company have risen 3.3% in a year against the industry’s decline of 5.6%.

Better-Ranked Food Bets

Vital Farms Inc. VITL offers a range of produced pasture-raised foods. It currently sports a Zacks Rank #1 (Strong Buy). VITL has a trailing four-quarter average earnings surprise of 102.1%. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Vital Farms’ current financial-year sales and earnings suggests growth of 22.5% and 59.3%, respectively, from the year-ago reported numbers.

Utz Brands Inc. UTZ manufactures a diverse portfolio of salty snacks and currently carries a Zacks Rank #2 (Buy). UTZ has a trailing four-quarter earnings surprise of 2%, on average.

The Zacks Consensus Estimate for Utz Brands’ current financial-year earnings suggests growth of 24.6% from the year-ago reported numbers.

McCormick & Company, Inc. MKC is a leading manufacturer, marketer and distributor of spices, seasonings, specialty foods and flavors. It currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for McCormick & Company’s current fiscal-year sales and earnings indicates advancements of 0.3% and 5.6%, respectively, from the year-ago reported figures. MKC has a trailing four-quarter earnings surprise of 5.4%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

McCormick & Company, Incorporated (MKC) : Free Stock Analysis Report

Sysco Corporation (SYY) : Free Stock Analysis Report

Vital Farms, Inc. (VITL) : Free Stock Analysis Report

Utz Brands, Inc. (UTZ) : Free Stock Analysis Report