Yahoo Finance

Yahoo Finance Taking a Closer Look at Brown-Forman

For long-term investment opportunities, the Dividend Aristocrats group is especially appealing. These companies have consistently raised their dividends for at least 25 consecutive years. This has shown their financial stability and their commitment to return money to investors.

In this analysis, I am going to examine Brown-Forman Corp. (NYSE:BF.A)(NYSE:BF.B). The company has distributed cash dividends every quarter for 80 years and raised it for 40 years in a row.

Global juggernaut in premium alcoholic market

With operations in more than 170 countries, Brown-Forman is recognized as a prominent player in the global marketplace for premium alcoholic drinks. The biggest market for the business throughout the 2024 financial year was the United States, with sales in this market making up 45% of total revenue. The rest originated from overseas markets (55%), with the main contributing countries being Germany, Australia, Mexico and the United Kingdom. The company's distribution strategy is adapted to the legal and regulatory context of each market, including owned distribution, partnerships and government-controlled models. Brown-Forman sells its products through distributors or state governments in the United States. It creates its own distribution channels in other countries, including France, Germany, Thailand, Germany, France, Australia and Japan. In Canada, it supplies to provincial governments.

Throughout fiscal 2024, the top two customers made up around 13% and 11% of total sales, demonstrating a wide range of customers that can help reduce the risk of dependence on any single client. The company experienced its highest sales during the last three months of the year, primarily due to increased holiday purchases, which made up 28% of total sales.

The brand portfolio, including Jack Daniel's Tennessee Whiskey, is the company's most valuable asset. In 2023, Jack Daniels introduced new products such as Jack Daniel's Bonded Tennessee Rye Whiskey and American Single Malt to its lineup. Other significant brands include Woodford Reserve, which sold over 1.70 million nine-liter cases in fiscal 2024, and Old Forester. The portfolio also includes some of the finest tequilas, such as Herradura as well as El Jimador, along with Scotch and Irish whiskies like The Glendronach, Benriach, Glenglassaugh as well as Slane. Thanks to recent acquisitions, Brown-Forman is also broadening its selection in the high-end gin and rum markets with the addition of brands such as Gin Mare and Diplomatico.

Growth in operating income driven by divestitures

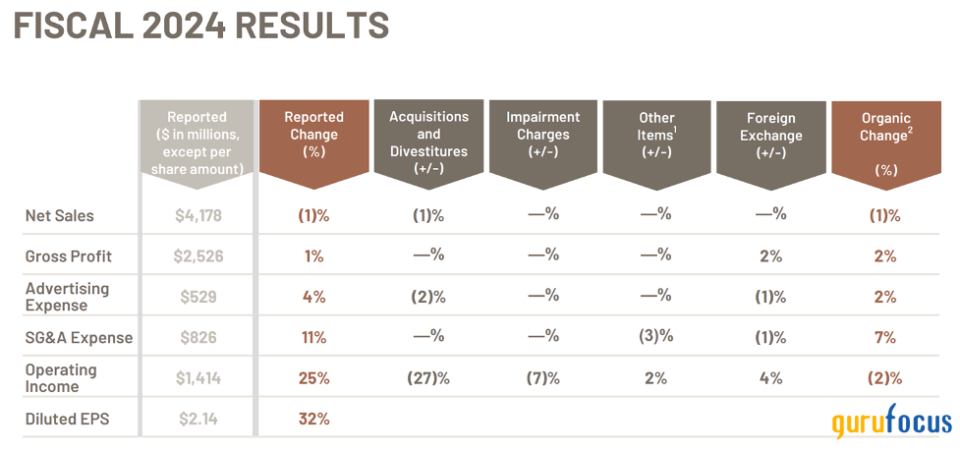

Brown-Forman has faced significant challenges from macroeconomic headwinds, including rising inflation and increased interest rates, and consumer purchasing behaviors, leading to the unprecedented changes in distributor inventories. These inventory fluctuations, driven by tough comparisons against prior-year inventory rebuilding and changes in distributor and retail ordering patterns.

At first glance, Brown-Forman appeared to have achieved an impressive 25% growth in reported operating income, reaching $1.40 billion. However, this surge was driven primarily by positive effects, including gains from the sale of the Finlandia vodka business and the Sonoma-Cutrer wine business. Looking closer, the organic revenue experienced a decline of 1% and its operating margin dropped by 2% in 2024.

Source: Brown-Forman presentation

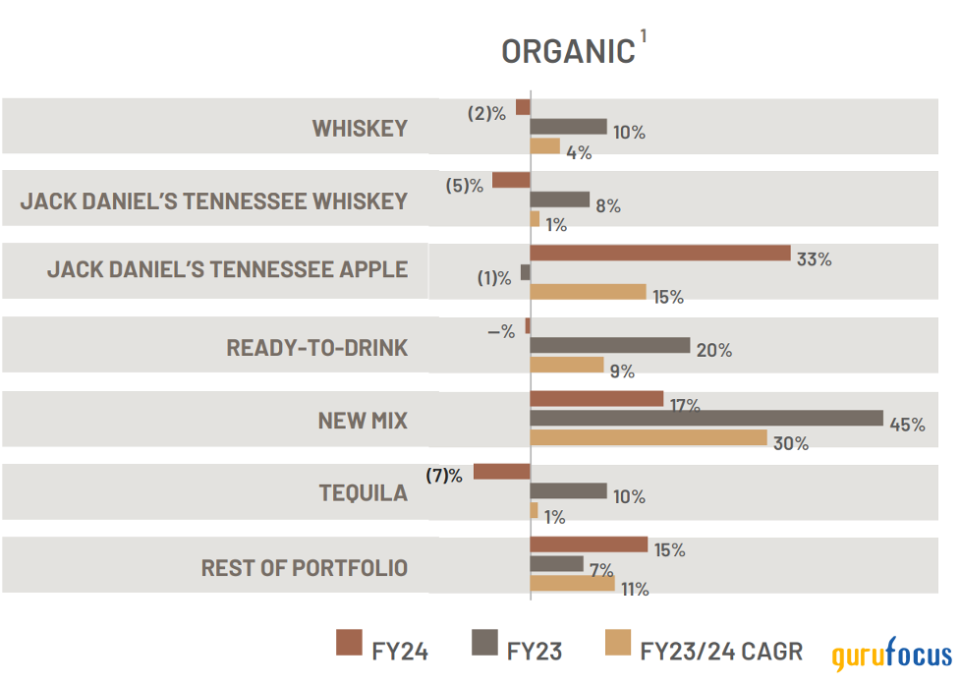

What makes investors optimistic is Brown-Forman's other key brands experienced good growth in many markets. Jack Daniel's Tennessee Apple, achieving double-digit growth, expanded successfully into markets like South Korea, Brazil and Chile. The Jack Daniel's super-premium expressions also showed robust growth, with brands like Jack Daniel's Sinatra, Single Barrel Rye and Bonded Rye contributing significantly.

Additionally, the ready-to-drink segment, particularly New Mix and Jack & Coke RTD, saw strong rise, with New Mix reaching over 10 million nine-liter cases and Jack & Coke RTD achieving 4.50 million nine-liter depletions across 25 markets. These depletion-based results measure the sale of its products from distributors to retailers. This strategic focus on premiumization, coupled with the integration of high-growth brands like Gin Mare and Diplomatico, has positioned Brown-Forman for continued success despite a dynamic operating environment.

Source: Brown-Forman presentation

Growing performance over time

Brown-Forman has maintained a steady increase in revenue as well as operating income over the years. Revenue grew from approximately $3 billion in 2014 to approximately $4.18 billion by 2024. Although there were some fluctuations, the operating income rose from $971 million to $1.15 billion over the past decade.

BF.A Data by GuruFocus

I ought to mention that about 49% of Brown-Forman's consolidated inventories are valued using the cost technique of last-in, first-out (LIFO), which can be used for nearly all its U.S. inventories. The rest of the inventories are valued using the cost method "first-in, first-out" (FIFO). FIFO is among the most widely used methods that companies use nowadays. This method presumes the very first items bought (or produced) are sold first, so the ending inventory consists of the most current costs. On the other hand, the LIFO technique assumes the items most recently acquired are sold first. Thus, the final inventory consists of the older costs.

The LIFO approach leads to reduced inventory values, greater cost of goods sold, reduced tax income and business income tax payments. If the company utilized FIFO for all its inventories, its inventory values will be greater (by $429 million in 2023 and by $512 million in 2024). It also would result in reduced COGS and increased pretax income of the same size. Therefore, under FIFO accounting, its operating income will be $1.56 billion in 2023 and $1.66 billion in 2024.

40 years of increasing dividends

For income investors who would like stability over the long run, Brown-Forman is a good candidate. Its long dividend payment history consists of quarterly dividends for 80 years as well as increases for 40 years. The dividend per share has increased consistently in the past couple of decades from 17 cents to 85 cents, providing a compound annual growth rate of 8.38%.

Even though a track record of increasing dividend payments sounds exciting, it is important to figure out whether the dividend payments are sustainable. We can take a look at the dividend payout ratio, which is the percent of earnings distributed by the business to shareholders as dividends. Throughout the last 20 years, Brown-Forman has enjoyed a good payout ratio of between 0.32 and 0.50.

BF.A Data by GuruFocus

Conservative capital structure

Brown-Forman has a strong balance sheet with high shareholders' equity and decent debt level. As of April, it had nearly $3.27 billion in total shareholders' equity and $374 million in cash and cash equivalents. The total long-term debt came in at around $2.68 billion, with maturities spreading out until 2045.

In the next five years, the company only has three debt matures in 2025, 2026 and 2028, with the debt principal ranging from $299 million to $375 million. With the current operating income and the cash level, Brown-Forman could pay off its long-term debt quite easily.

Fairly valued

We can use the Gordon Growth Model to value Brown-Forman. This model is quite suitable for companies with consistent dividend growth. Thus, this fits well with the company considering its remarkable history of four decades of uninterrupted dividend increases.

Assuming Brown-Forman will grow its dividend at the reduced rate of 8% per year, with a discount rate of 10%, the intrinsic value is calculated as follows:

P = Expected Dividend for 2025 / (Required Rate of Return - Dividend Growth Rate)

= 0.85 *(1+8%) / (10%-8%)

= $45.90

The Gordon Growth Model suggests the intrinsic value of Brown-Forman is around $45.90 per share, which is only 5% higher than the current share price of $43.60. As such, we can conclude is currently fairly valued

Takeaway

For investors looking for a long-term investments, Brown-Forman's solid business model and long history of dividend payments make it an attractive option. Although its share price has fallen by 34%, it remains well positioned for growth in the years ahead because of its solid financial position, the product varieties and smart acquisitions. Its sound financial position is backed by its conservative capital structure, constant growth in both revenue and operating income ,along with a commitment to maintaining an increasing dividend with a disciplined payout ratio.

The Gordon Growth Model values the stock at $45.90 per share. Thus, Brown-Forman is currently fairly valued. As a result, I think it is a decent pick for investors seeking consistent dividends.

This article first appeared on GuruFocus.