Yahoo Finance

Yahoo Finance Top Value Stocks That Could Be Bargains In June 2024

As global markets continue to navigate through political uncertainties and mixed economic signals, investors are keenly observing shifting trends across various indices. With the S&P 500 and Nasdaq reaching new highs amid a narrow market advance, discerning investors might find potential opportunities in undervalued stocks that could emerge as bargains.

Top 10 Undervalued Stocks Based On Cash Flows

Name | Current Price | Fair Value (Est) | Discount (Est) |

Plus Alpha ConsultingLtd (TSE:4071) | ¥1885.00 | ¥3564.60 | 47.1% |

Selective Insurance Group (NasdaqGS:SIGI) | US$91.87 | US$183.64 | 50% |

DO & CO (WBAG:DOC) | €156.80 | €313.00 | 49.9% |

Boule Diagnostics (OM:BOUL) | SEK10.50 | SEK20.93 | 49.8% |

Shanghai Milkground Food Tech (SHSE:600882) | CN¥13.54 | CN¥26.97 | 49.8% |

Interojo (KOSDAQ:A119610) | ₩24900.00 | ₩49562.21 | 49.8% |

17LIVE Group (SGX:LVR) | SGD0.765 | SGD1.52 | 49.8% |

Hollysys Automation Technologies (NasdaqGS:HOLI) | US$21.21 | US$42.18 | 49.7% |

Humble Group (OM:HUMBLE) | SEK9.775 | SEK19.45 | 49.8% |

Napatech (OB:NAPA) | NOK37.30 | NOK74.12 | 49.7% |

Below we spotlight a couple of our favorites from our exclusive screener

UCB

Overview: UCB SA is a global biopharmaceutical company specializing in neurology and immunology diseases, with a market capitalization of approximately €26.03 billion.

Operations: The company generates €5.18 billion in revenue from its biopharmaceuticals segment.

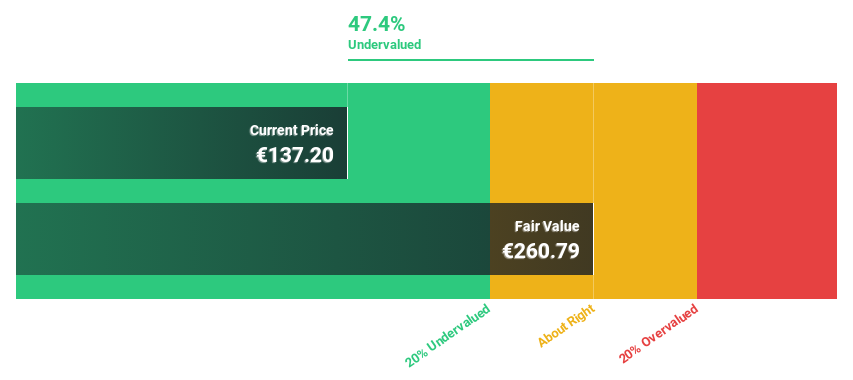

Estimated Discount To Fair Value: 47.4%

UCB's financial analysis highlights its trading status at €137.85, significantly below the estimated fair value of €260.79, indicating a potential undervaluation by 47.1%. Despite this, UCB's forecasted annual revenue growth rate of 9.2% falls short of the high-growth threshold but surpasses the Belgian market's 6.3%. Earnings are expected to rise by an impressive 27.7% annually, outpacing the market projection of 17.6%. However, its projected Return on Equity (ROE) in three years is considered low at 13.8%, suggesting some concerns about efficiency or profitability relative to equity levels.

Insights from our recent growth report point to a promising forecast for UCB's business outlook.

Delve into the full analysis health report here for a deeper understanding of UCB.

Equifax

Overview: Equifax Inc., a data, analytics, and technology company, has a market capitalization of approximately $29.87 billion.

Operations: The company's revenue is generated from three primary segments: International ($1.27 billion), Workforce Solutions ($2.32 billion), and U.S. Information Solutions ($1.76 billion).

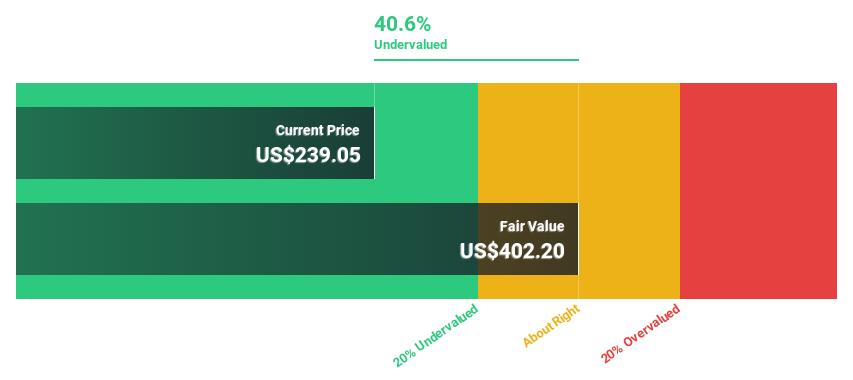

Estimated Discount To Fair Value: 40.6%

Equifax, with a current trading price of US$239.05, is significantly undervalued by 40.6%, positioned below the fair value estimate of US$402.2. This discrepancy highlights potential market oversight despite robust forecasts for revenue and earnings growth, outpacing the US market averages at 9.6% and 22.2% per year respectively. However, its high level of debt could temper investor optimism, necessitating a balanced view on its financial health and growth trajectory amidst recent executive changes and strategic partnerships aimed at enhancing data-driven services.

According our earnings growth report, there's an indication that Equifax might be ready to expand.

Take a closer look at Equifax's balance sheet health here in our report.

Zhongji Innolight

Overview: Zhongji Innolight Co., Ltd. focuses on researching, developing, producing, and selling optical communication transceiver modules and optical devices within China, with a market capitalization of approximately CN¥156.49 billion.

Operations: The company generates revenue primarily from the sale of optical communication transceiver modules and optical devices.

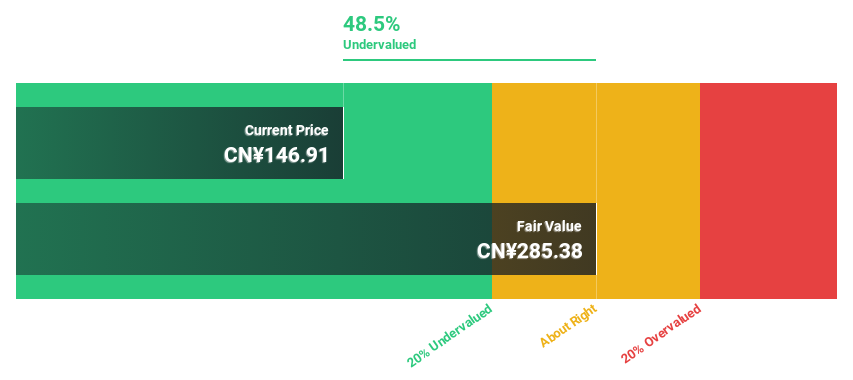

Estimated Discount To Fair Value: 48.5%

Zhongji Innolight, priced at CN¥146.91, is significantly undervalued with a fair value estimate of CN¥285.38. This valuation gap is supported by strong fundamentals, including a forecasted earnings growth of 30.3% annually and revenue growth of 30.7% per year, both surpassing market averages significantly. Despite its highly volatile share price recently, the company's robust non-cash earnings and recent dividend increases suggest an appealing cash flow profile that could attract investors looking for growth at a reasonable price.

Key Takeaways

Click this link to deep-dive into the 950 companies within our Undervalued Stocks Based On Cash Flows screener.

Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Contemplating Other Strategies?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ENXTBR:UCB NYSE:EFXSZSE:300308

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com