Yahoo Finance

Yahoo Finance Why You Should Buy Global Payments (GPN) Stock Right Now

Global Payments Inc. GPN is a leading payment technology and software solutions provider that has the potential to benefit from the rising demand for point-of-sale solutions. Increasing transaction volumes and core issuer growth in the Issuer Solutions business are expected to continue boosting its performance.

Due to its solid prospects, this currently Zacks Rank #2 (Buy) stock presents an attractive investment opportunity for investors at the moment. Let’s delve deeper & check the positives for the stock.

Estimates

Seven estimates for the 2024 bottom line moved north in the past 60 days versus two southward revisions, reflecting the majority of analysts’ confidence in the company. The Zacks Consensus Estimate for GPN’s 2024 bottom line of $11.64 per share indicates an 11.7% year-over-year increase. The consensus estimate for 2025 indicates further 13.5% growth on a year-over-year basis.

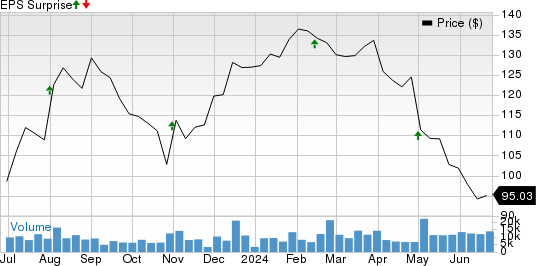

The company beat earnings estimates in each of the past four quarters, with an average surprise of 1.1%. This is depicted in the figure below.

Global Payments Inc. Price and EPS Surprise

Global Payments Inc. price-eps-surprise | Global Payments Inc. Quote

The consensus estimate for 2024 revenues is pegged at $9.2 billion, signaling 6.4% year-over-year growth. Both its Merchant Solutions and Issuer Solutions businesses are expected to support its top-line growth.

Growth Drivers

The Merchant Solutions unit will likely benefit from growth in volume, U.S. merchant partners and point-of-sale. We expect revenues from Merchant Solutions alone to grow more than 9% year over year this year. Meanwhile, the Issuer Solutions segment is expected to gain from higher transactions and core issuer growth. Our model estimate indicates Issuer Solutions revenues to see a nearly 6% jump.

If we look at its geographical breakdown, it generated only 4.3% year-over-year growth in the Americas last year and 5.4% in the Asia Pacific region. The Europe business, on the other hand, witnessed a 28.6% increase and is expected to continue the momentum. Even in the first quarter of 2024, the business recorded 31.2% growth. The Americas business will continue to bring stability and innovation to its growth path.

The large numbers of unbanked individuals and small businesses across the Asia Pacific region present a significant opportunity for GPN to expand its network. Effectively tapping into this market could serve as a sustainable growth catalyst for the company.

Lastly

Despite Global Payments' shares declining 25.1% year to date, in contrast with the industry's 3.4% growth, the company now offers a compelling entry point for investors. Valuation-wise, Global Payments appears significantly undervalued, relative to the industry average, with its shares trading at a forward price/earnings ratio of 7.67X, notably lower than the industry average of 21.60X.

Other Stocks to Consider

Investors interested in the broader Business Services space can look at some other top-ranked stocks like Envestnet, Inc. ENV, Paysafe Limited PSFE and Fiserv, Inc. FI, each carrying a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Envestnet’s 2024 earnings is currently pegged at $2.62 per share, indicating 23.6% year-over-year growth. It beat earnings estimates in three of the past four quarters and met once, with an average surprise of 9.4%. The consensus mark for ENV’s revenues of almost $1.4 billion suggests a 9.6% increase from the year-ago level.

The Zacks Consensus Estimate for Paysafe’s current-year earnings is now pegged at $2.47 per share, indicating 6% year-over-year growth. It beat earnings estimates thrice in the past four quarters and missed once, with an average surprise of 18.3%. The consensus mark for PSFE’s revenues of $1.7 billion suggests a 6.5% increase from the year-ago level.

The Zacks Consensus Estimate for Fiserv’s 2024 earnings of $8.69 per share suggests 15.6% year-over-year growth. It beat earnings estimates thrice in the past four quarters and met once, with an average surprise of 2.3%. The consensus estimate for FI’s current year revenues is pegged at $19.3 billion, indicating a 7.2% increase from a year ago.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Global Payments Inc. (GPN) : Free Stock Analysis Report

Envestnet, Inc (ENV) : Free Stock Analysis Report

Fiserv, Inc. (FI) : Free Stock Analysis Report

Paysafe Limited (PSFE) : Free Stock Analysis Report