Yahoo Finance

Yahoo Finance ConocoPhillips: Oil Stocks Are Vulnerable to a US Recession

ConocoPhillips (NYSE:COP) is a global oil and gas company, with 76% of its 2023 revenue generated in the United States. The company's stock has surged higher over the past three years on the back of buybacks and elevated oil prices. However, I believe oil prices could fall off in the event of a U.S. recession, potentially hitting oil stocks hard. With a near all-time high price-book ratio of 3, ConocoPhillips' stock does not seem to be pricing in the downside.

Why a U.S. recession could hit ConocoPhillips

The American economy has been booming since 2020 due to government stimulus, but with a large federal deficit and record debt-to-gross domestic product, this trend may be unsustainable. GDP growth recently fell dramatically to 1.60% in the first quarter of 2024 from 3.4% in the fourth quarter of 2023. The yield curve has been inverted for some time now, and it has a perfect track record of predicting recessions because it incentivizes consumers and investors to go to cash. Moreover, leading indicators like RV sales have recently fallen off in North America; this was discussed in my analysis of Thor Industries (NYSE:THO).

Legendary investors Warren Buffett (Trades, Portfolio) and Peter Lynch famously do not attempt to predict macroeconomic events and instead invest fearlessly when a business' valuation is favorable. I subscribe to this way of thinking. I like to buy when the outlook is gloomy and the valuation tilts the risk-reward in my favor. The problem is, nobody is talking about the downside when it comes to oil stocks. Thus, I think a recession would be more devastating to the shares of energy companies than the shares of other cyclicals where earnings have already been weak and investors fear the worst.

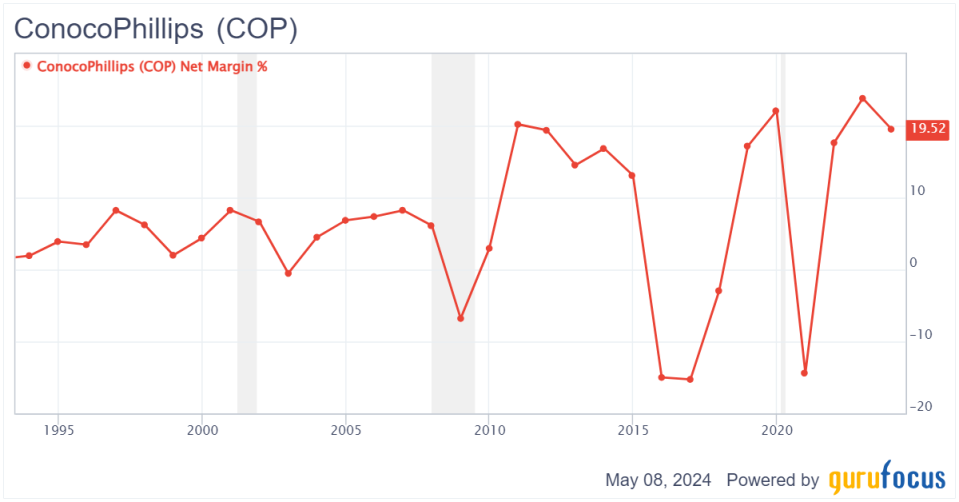

If we look at ConocoPhillips' earnings history, the cyclicality jumps off the page. ConocoPhillips' profit margins dipped into negative territory in 2002, and were deeply negative in 2008, 2016 and 2020. Recently, the company's profit margins have been hovering around all-time highs:

But we should not expect this to continue. I believe ConocoPhillips' record of reporting bottom-line losses has something to do with the location of its assets. The company has some high-cost extraction sites, such as U.S. shale and the Canadian oil sands. While these areas have geopolitical stability, they also have high labor costs, expensive equipment and sometimes low-quality oil. In 2023, ConocoPhillips expanded its position in the Canadian oil sands, becoming the sole owner of Surmont.

All this means is ConocoPhillips is vulnerable should oil prices fall like they did during the U.S. recessions of 2002, 2008 and 2020. The average West Texas Intermediate oil peak-to-trough decline during these three downturns was approximately 60%. If that were to happen again, WTI oil prices would fall below $35 per barrel, which, in my estimation, would cause ConocoPhillips to produce zero free cash flow and suspend its share buybacks.

Management's capital allocation

ConocoPhillips' CEO seems to be very cognizant of avoiding big acquisitions at the top of the cycle. However, the company has been less prudent when it comes to share buybacks, repurchasing huge swaths of stock at the top of the cycle in 2022 and 2023. I would generally prefer to see companies keep excess cash on their balance sheets or pay out special dividends when there is nothing intelligent to do. The money could have also been spent on oil exploration, as we will discuss next.

The company's oil reserves are underwhelming

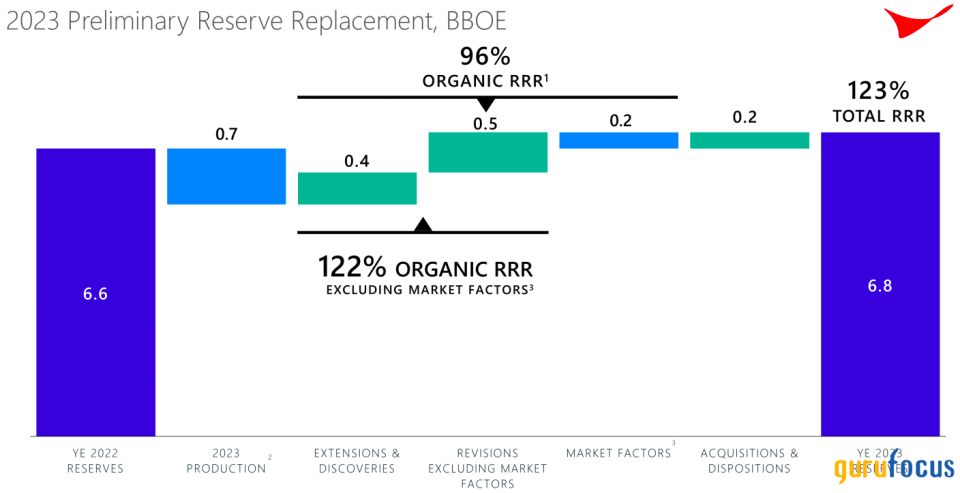

ConocoPhillips had reserves of 6.8 billion barrels of oil equivalent at the end of 2023. If we compare this to the company's 2023 production of 0.7 billion barrels, it has 9.7 years' worth of reserves, all things equal. I have analyzed a lot of oil companies, and this is definitely on the low end. I prefer it when oil companies have a reserve life of at least 13 years. Why? Because if they do not, they may have to spend a lot of money to grow their reserves or even reduce their annual production. ConocoPhillips is guiding toward spending more than depreciation and amortization on capital expenditures in 2024, and the company's underwhelming oil reserves may be a big reason why.

The valuation

The stock is currently priced richly compared to its historical price-book ratio and compared to its average earnings. Over the past 10 years, the company has averaged $4.64 billion of net income, but its market cap currently stands at $147 billion. The company's asset base has not expanded to a level that would support this valuation. The valuation seems to be supported by top-of-cycle buybacks, bullish sentiment and extrapolation of high oil prices.

The growth side of the equation is not looking very rosy, either. ConocoPhillips can allocate capital to share buybacks and acquisitions, but both options currently look unattractive. Moreover, the energy transition has persisted, which could eventually lead to a peak in fossil fuel demand. Looking at WTI oil prices, the inflation-adjusted average since 1970 has been approximately $65, which is below today's price of $81 WTI. For these reasons, I actually think ConocoPhillips' earnings per share could be lower in 10 years' time, assuming oil prices revert to the mean.

Summary

ConocoPhillips does not appear to have a cost moat, operating in relatively high-cost areas. Thus, the company has reported negative net income in four of the past 10 years. With some troubling signals for the U.S. economy flashing, I estimate this could happen again. The past three U.S. recessions have led to WTI price declines of, on average, 60%. Given ConocoPhillips' long-term demand headwinds, high price-book and high price to 10-year average earnings (roughly 32 times), I am bearish on the stock and think now is the time for caution.

This article first appeared on GuruFocus.