Yahoo Finance

Yahoo Finance Dollar’s Move Down Continues Ahead of Final GDP

The US dollar has generally lost strength against most major currencies and gold moved up over the last fortnight as a large majority of participants now expects the Federal Reserve (‘the Fed’) to cut its funds rate in March next year. A fairly strong Santa rally for many blue-chip shares has drawn attention somewhat away from currencies, although oil’s bounce has featured high momentum and the pound has been more active after lower than expected British inflation. This article summarises the latest data and sentiment affecting the US dollar then looks briefly at the charts of EURUSD and GBPUSD.

Three weeks ago, the majority of traders expecting a cut by the Fed in March had been quite small according to CME FedWatch Tool. Now, though, that’s up to nearly 70%, with only 21% of participants expecting a hold at the current 5.25-5.5% to persist into the second quarter of 2024.

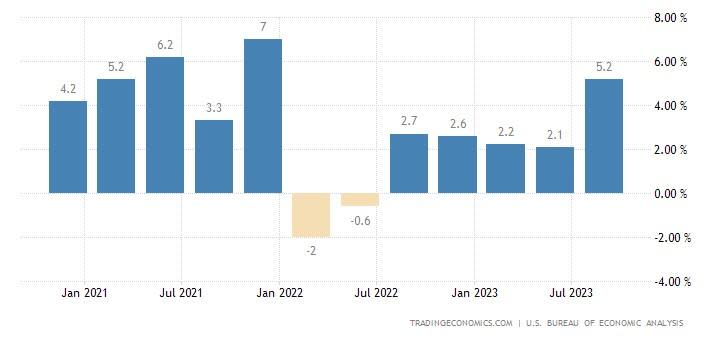

Although senior members of the Federal Open Market Committee (‘the FOMC’) pointed to slowing economic growth in recent statements and their last meeting, GDP in the USA remains strong considering the circumstances:

The second estimate for the third quarter’s change in GDP of 5.2% was higher than the consensus, while the first estimate of 4.9% was also much higher than the roughly 4-4.3% expected. Consumers’ spending remains resilient despite a long period of high inflation in focus and a more moderate job market.

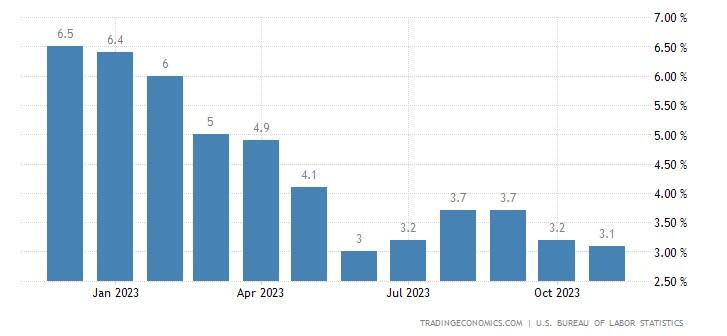

One of the big question marks for the Fed now is how much loosening would be too much. Inflation has certainly been less rampant for much of 2023:

Although the rate of non-core inflation has halved since the beginning of the year, it remains above the traditional target of 2%. The Fed has the unenviable task of walking the tightrope between at least modest economic growth if possible and preventing a resurgence of inflation after a premature pivot as happened in the 1970s.

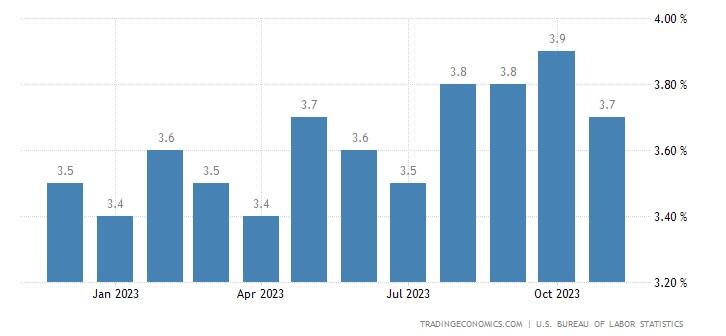

Positivity certainly comes from recent employment data, specifically the rate of unemployment. This bucked the recent trend in November and declined:

In late summer, it seemed possible that unemployment could move gradually but more-or-less consistently upward in line with high expectations for a recession. Whether last month’s decline is an outlier or suggests a sideways trend remains to be seen. The next NFP on 5 January might provide more clues.

The main release affecting the greenback today is the final figure for American third-quarter GDP at 13.30 GMT. The consensus remains 5.2%, but if the actual release differs significantly, especially higher, the majority expecting monetary loosening next quarter might decline and the dollar could regain some strength.

Euro-dollar, Daily

Volatility for EURUSD has been somewhat higher in December so far, with the strong correction from $1.10 ending quickly a bit above $1.07. The chart suggests that the uptrend is still active, with the price above the three moving averages and the 50 SMA having golden crossed the 100 about a fortnight ago. However, the price isn’t currently overbought according to the slow stochastic or Bollinger Bands.

Buying volume increased significantly last week, so it might be possible this time to see a breakout above $1.10. Second tests are usually weaker and volume around Christmas and new year is also usually lower than normal, so such a movement might not occur until January. The 50 SMA seems to be the main dynamic support at the moment, while $1.125 could be the next resistance if there is a successful breakout from $1.10. Between final GDP and Friday’s personal consumption expenditures, volatility will probably remain quite high into the end of the week.

Cable, Daily

Although the overall impression on the chart of cable is quite similar to euro-dollar, there are some important differences. Firstly there’s fundamentals, with British inflation on Tuesday having declined much more than expected: November’s non-core was 3.9% against 4.4% expected and the core figure 5.1% compared to the expectation of 5.6%.

The technical situation also seems to be somewhat more positive than for euro-dollar. The spike in buying volume about a week ago is also visible here but more pronounced. Cable has also actually reached a new high within the last week around $1.28. The next clear potential target in the medium term might be $1.30, which could provide a better ratio of risk to reward for some traders than euro-dollar. The 61.8% monthly Fibonacci retracement slightly above $1.25 is a key static area of support.

The opinions in this article are personal to the writer. They do not reflect those of Exness or FX Empire.

This article was originally posted on FX Empire