Yahoo Finance

Yahoo Finance Here's Why You Should Retain Royal Caribbean (RCL) Stock

Royal Caribbean Cruises Ltd. RCL is benefiting from pent-up demand, booking improvement and addition of new ships. However, coronavirus woes and high costs remain concerns. Let’s delve deeper.

Key Catalysts

Royal Caribbean resumed operations in limited capacity and started receiving positive reviews by customers sailing with the company. Going forward, the initiative is likely to boost its image with regard to operations under the COVID-19 environment. Ever since the last business update, 11 more ships have returned to operation. It is already operating 40 ships across its five brands, representing 65% of capacity. More than 500,000 guests have sailed across the company’s five brands since the resumption. The company anticipates more than 1 million guests to sail by the end of this year. By the end of 2021, it expects 50 out of 61 ships to resume services across its five brands, which represents nearly 100% of its core itineraries and roughly 80% of worldwide capacity.

The pandemic has significantly impacted bookings for 2021. However, booking volumes have improved since the slowdown this summer due to the Delta variant. The company received more bookings during third-quarter 2021 compared with the second quarter. New bookings for 2022 during September were robust. The company announced that sailings for 2022 are booked within historical ranges and at higher prices than 2019.

Despite the coronavirus pandemic, the company continues to add new cruises. During first-quarter 2021, it added Odyssey of the Seas to its fleet. Meanwhile, the company stated that it anticipates adding Silver Dawn to the Silversea fleet during fourth-quarter 2021. The company has two ships scheduled for delivery namely Wonder of the Seas and Celebrity Beyond in 2022. The Zacks Rank #3 (Hold) company announced that its new ship — Project Evolution — will have some of the most advanced environmental features of any cruise ship on the water or in the construction docks.

Maintaining liquidity has become a herculean task for most of the companies during the coronavirus pandemic. As of Sep 30, 2021, the company had cash and cash equivalents of approximately $3.3 billion, compared with $4.3 billion at the end of Jun 30, 2021. Although the company’s long-term debt at the end of third-quarter 2021 stands at $19.9 billion, it has no debt maturities for the remainder of 2021 and $2.2 billion for 2022. At the end of third-quarter 2020, the company had a debt-to-capital ratio of 0.7, which indicates that its debt level is manageable.

Image Source: Zacks Investment Research

Concerns

The leisure industry is currently grappling with the coronavirus pandemic and Royal Caribbean isn’t immune to the trend. The company is expected to report net loss on both GAAP and adjusted basis for the fourth quarter and the fiscal 2021. The company anticipates depreciation and amortization expenses in the range of $325 million to 330 million for fourth-quarter 2021. Net interest expenses for the third quarter are expected to be $250-$255 million. Meanwhile, capital expenditures for the remaining of 2021 are anticipated to be $600 million. China, which is closed for international travelers, will continue to hurt cruise operators.

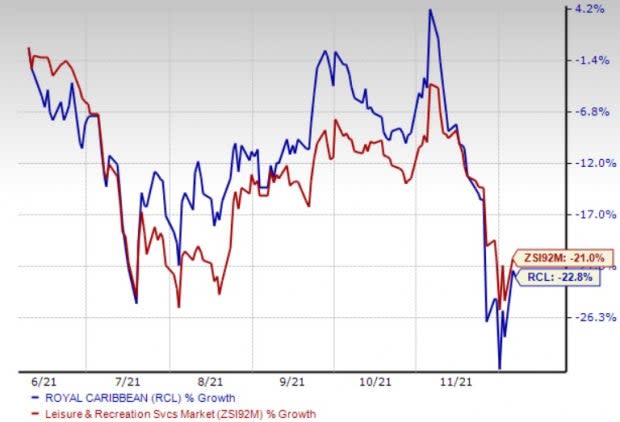

The company does not expect China to reopen until at least the Olympics in Beijing are over. Higher cash burn continues to hurt the company. Shares of the company have slumped 22.8% in the past six months, compared with the industry’s decline of 21%.

Key Picks

Some better-ranked stocks in the Consumer Discretionary sector include Hilton Grand Vacations Inc. HGV, Bluegreen Vacations Holding Corporation BVH and Camping World Holdings, Inc. CWH.

Hilton Grand Vacations sports a Zacks Rank #1 (Strong Buy). The company has a trailing four-quarter earnings surprise of 411.1%, on average. Shares of the company have jumped 14% in the past three months. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Hilton Grand Vacations’ current financial year sales and earnings per share suggests growth of 222.1% and 170.8%, respectively, from the year-ago period.

Bluegreen Vacations flaunts a Zacks Rank #1. The company has a trailing four-quarter earnings surprise of 695%, on average. Shares of the company have surged 35.5% in the past three months.

The Zacks Consensus Estimate for Bluegreen Vacations current financial year sales and earnings per share indicates growth of 27.5% and 199.3%, respectively, from the year-ago period.

Camping World carries a Zacks Rank #2 (Buy). The company has been benefiting from the launch of a fresh peer-to-peer RV rental marketplace and a mobile service marketplace. It has been investing heavily in product development.

Camping World has a trailing four-quarter earnings surprise of 70.9%, on average. Shares of the company have appreciated 5.4% in the past three months. The Zacks Consensus Estimate for CWH’s current financial year sales and earnings per share suggests growth of 25.9% and 77.6%, respectively, from the year-ago period.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Camping World (CWH) : Free Stock Analysis Report

Hilton Grand Vacations Inc. (HGV) : Free Stock Analysis Report

Bluegreen Vacations Holding Corporation (BVH) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research