Yahoo Finance

Yahoo Finance Hydro One (TSE:H) Is Paying Out A Larger Dividend Than Last Year

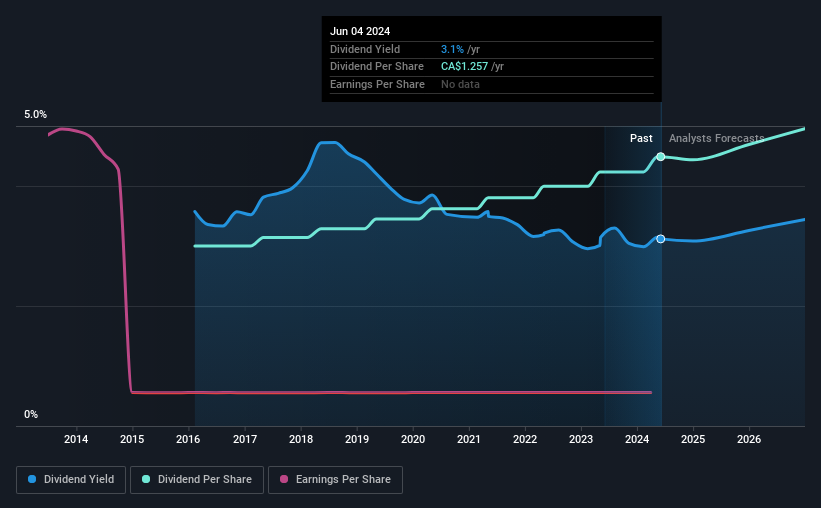

Hydro One Limited (TSE:H) has announced that it will be increasing its dividend from last year's comparable payment on the 28th of June to CA$0.3142. Even though the dividend went up, the yield is still quite low at only 3.1%.

See our latest analysis for Hydro One

Hydro One's Dividend Is Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive. Based on the last payment, Hydro One's earnings were much higher than the dividend, but it wasn't converting those earnings into cash flow. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

Over the next year, EPS is forecast to expand by 20.2%. If the dividend continues along recent trends, we estimate the payout ratio will be 30%, which is in the range that makes us comfortable with the sustainability of the dividend.

Hydro One Is Still Building Its Track Record

It is great to see that Hydro One has been paying a stable dividend for a number of years now, however we want to be a bit cautious about whether this will remain true through a full economic cycle. Since 2016, the dividend has gone from CA$0.84 total annually to CA$1.26. This means that it has been growing its distributions at 5.2% per annum over that time. Investors will likely want to see a longer track record of growth before making decision to add this to their income portfolio.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Hydro One has seen EPS rising for the last five years, at 13% per annum. While on an earnings basis, this company looks appealing as an income stock, the cash payout ratio still makes us cautious.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. This company is not in the top tier of income providing stocks.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've identified 2 warning signs for Hydro One (1 shouldn't be ignored!) that you should be aware of before investing. Is Hydro One not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.