Yahoo Finance

Yahoo Finance Is Insulet (PODD) Stock an Apt Pick for Your Portfolio Now?

Insulet Corporation PODD is primed for growth in the coming quarters as its revolutionary Omnipod 5 offering continues to successfully drive market growth. The company is making remarkable progress in terms of its key strategic imperatives to help patients in their diabetes management. Sound financial stability further instills optimism.

Meanwhile, the growing macroeconomic challenges raise concerns for Insulet’s operations, which may hinder its growth prospects. The company’s sole reliance on the Omnipod platform may become a risk if any adverse changes occur.

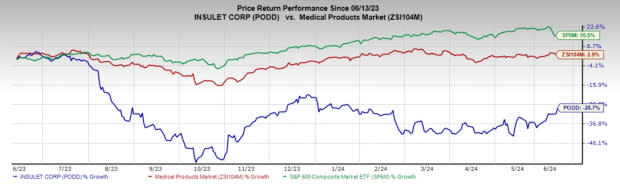

In the past year, this Zacks Rank #3 (Hold) stock has declined 28.7% compared to the 2.9% rise of the industry and the 16.5% growth of the S&P 500 composite.

The developer, manufacturer and distributor of insulin delivery systems has a market capitalization of $13.46 billion. Insulet projects a long-term estimated earnings growth rate of 17.9% compared with 11.9% of the industry. PODD’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 83%.

Let’s delve deeper.

Upsides

Omnipod 5, a New Focus: Insulet’s highly differentiated Omnipod 5 stands out as the only FDA-cleared, fully disposable pod-based AID system. The product attributes such as on-body wearable, simplicity, ease of use and broad accessibility are the key drivers of its rapid adoption and are successfully driving market growth. During the first quarter, nearly 85% of the new starts came from people previously using multiple daily injections, Insulet’s target market, while competitive conversions also remained very strong.

In 2023, Omnipod 5 was successfully launched in Germany for individuals aged two years and older with type 1 diabetes, following its debut in the United Kingdom. The success in these countries is significantly propelling the company’s growth, with more than half of the total international new customer starts coming from Omnipod 5 in the first quarter. Additionally, Insulet is on track to submit for FDA label expansion by the end of this year, which, once cleared, will meaningfully accelerate Omnipod 5 adoption among the approximate 2.5 million people with insulin-intensive type 2 diabetes.

Image Source: Zacks Investment Research

‘Awareness’ and ‘Innovation’ Strategies Bode Well: Insulet continues to broaden the market access and awareness of Omnipod through its direct-to-consumer advertising campaign and growing its presence in the U.S. pharmacy channel. The company’s approach to increasing Omnipod’s awareness among endocrinologists and primary care physicians has resulted in more healthcare providers (HCPs) writing scripts for the products.

The company began a limited market release of Omnipod 5 paired with Dexcom's G7 sensor in the United States, as well as with Abbott's Freestyle Libre 2 Plus sensor in both the United Kingdom and the Netherlands. The system will be equipped with more customer-focused innovations this year such as new sensor integrations, extending to the iPhone platform and also expanding into more geographies. Furthermore, Insulet’s FDA-cleared Omnipod GO, tailored for the type 2 market, is poised for broader adoption among HCPs and physician practices, backed by successful pilot efforts.

Strong Solvency but Leveraged Balance Sheet: Insulet’s financial position remained robust as it exited the first quarter of 2024 with cash and cash equivalents of $751 million and current debt of $39 million. This financial stability appears highly promising, especially during the prolonged period of macroeconomic issues.Although the long-term debt of $1.36 billion remained marginally in line with the previous fourth quarter, total debt-to-capital improved 2% sequentially to 63.9%.

Downsides

Economic Uncertainty Hampers Growth: The continuing worldwide macroeconomic and geopolitical uncertainty may reduce demand for Insulet’s products, intensify competition, exert pressure on prices, dent supply and lengthen the sales cycle. We are particularly cautious as growth could moderate further if the economic scenario worsens. The company continues to experience challenges stemming from the global supply chain disruption.

Sole Reliance on the Omnipod System: Insulet’s financial results continue to largely depend on the performance of its lead product — the Omnipod System. Per the company, any adverse changes in the market acceptance of the product or worsening of the factors that negatively influence the sale will dent the company’s financials majorly.

Estimate Trend

The Zacks Consensus Estimate for Insulet’s 2024 earnings per share (EPS) has moved south 0.6% to $3.11 in the past 30 days.

The Zacks Consensus Estimate for the company’s 2024 revenues is pegged at $1.98 billion. This suggests a 16.6% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Hims & Hers Health HIMS, Medpace MEDP and ResMed RMD.

Hims & Hers Health’s earnings are expected to surge 263.6% in 2024 compared with the industry’s 17.9%. HIMS’ earnings surpassed estimates in three of the trailing four quarters and missed in one, delivering an average surprise of 79.2%. Its shares have surged 161.9% against the industry’s 29.2% decline in the past year.

HIMS sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Medpace, also sporting a Zacks Rank #1 at present, has an estimated 2024 earnings growth rate of 27.1% compared with the industry’s 12.6%. Shares of MEDP have rallied 84.4% compared with the industry’s 3.7% growth over the past year.

MEDP’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 12.8%. In the last reported quarter, it delivered an earnings surprise of 30.6%.

ResMed, carrying a Zacks Rank #2 (Buy) at present, has an estimated fiscal 2024 earnings growth rate of 19.6% compared with the industry’s 11.3%. Shares of RMD have dropped 1.8% against the industry’s 2.9% growth over the past year.

RMD’s earnings surpassed estimates in three of the trailing four quarters and missed in one, delivering an average surprise of 2.8%. In the last reported quarter, it delivered an earnings surprise of 10.9%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ResMed Inc. (RMD) : Free Stock Analysis Report

Insulet Corporation (PODD) : Free Stock Analysis Report

Medpace Holdings, Inc. (MEDP) : Free Stock Analysis Report

Hims & Hers Health, Inc. (HIMS) : Free Stock Analysis Report