Yahoo Finance

Yahoo Finance Netflix Is Overvalued Amid Future Content Quality Challenges

Netflix Inc. (NASDAQ:NFLX) is one of the West's most popular online entertainment platforms. It faces the most significant threat in competition from Amazon's (NASDAQ:AMZN) Prime Video and Apple's (NASDAQ:AAPL) Apple TV+, who I believe are outperforming Netflix in the quality of content offered.

In addition, while Netflix has strong fundamentals, including great margins, its valuation is less appealing than I would like at this time. Considering the risks related to the viability of its international expansion plans, I think there are better long-term investments to be made.

Operations analysis

Netflix is a leading global streaming entertainment service. As of the last quarterly report, it had over 260 million paid memberships in more than 190 countries. The company's content strategy focuses heavily on original programming; it spent approximately $17 billion on content in 2023. A large part of its future expansion strategy involves international operations in Europe, the Middle East and Africa, Latin America and Asia-Pacific. It intends to continue to emphasize local content to drive its growth in foreign regions, which I believe is clever as it will allow the company to appeal organically in international markets rather than reworking American titles for foreign audiences.

The streaming giant faces several high-threat competitors. Based on my research, these four companies are likely to be the most competitive against Netflix over the next 10 years:

Disney+, under The Walt Disney Company (NYSE:DIS) has an extensive range of content from Disney, Pixar, Marvel, Star Wars and National Geographic. It also comes bundled with Hulu and ESPN+.

Amazon Prime Video, under Amazon, is part of the Amazon Prime service, which includes shopping, music and other services. Its substantial financial backing and integration with Amazon's ecosystem is a high threat to Netflix's offerings.

Max, under Warner Bros. Discovery Inc. (NASDAQ:WBD), offers a mix of movies, TV series and original programming. Its collaboration with Warner Bros. and other strategic partnerships allows it to offer leading exclusive content.

Apple TV+, under Apple, focuses on quality over quantity and is seamlessly integrated into its ecosystem. Its support from Apple's vast financial resources allows it to develop strong content, further strengthened by Apple's global reach.

In my personal opinion, after having used all of these services other than Max, Netflix is very well-positioned and offers relatively good quality at a low cost. However, I do not think it should be underestimated just how strong the catalog is becoming for Amazon Prime Video and Apple TV+ users, where I see a much more stringent focus on quality. Apple is the standout here, as it only has around 100 original titles, aiming to develop high-budget, award-winning originals. In contrast, as of 2023, Netflix boasted approximately 3,700 movies and 2,100 TV shows, while Amazon Prime Video has the largest content catalog among the major streaming services, offering over 5,000 movies and around 2,300 TV shows as of early 2023. However, Amazon also makes more selective investments in high-budget offerings, which, in my opinion, gives it a lead in both quality and breadth compared to Netflix in a significant way.

Financial and valuation analysis

To get a thorough understanding of each of the competitor's financial results alongside each other, please consider the data in the following table, which I have aggregated, and the 10-year price return comparison graph that follows:

Netflix has done extremely well for shareholders over the past decade, appreciating with a compound annual growth rate of 26.48%. Amazon has performed just slightly better with a CAGR of 27.26%. Apple is in third place with a CAGR of 23.69%. Both Disney and Warner Bros. Discovery's results have been much weaker, with the latter actually delivering a loss over the selected time period.

I believe the reason for these performance results are made clear by the data in my table. Disney has a remarkably low net margin, even though its recent growth has been promising. I believe investors are beginning to question the long-term viability of its business model, predominantly because it is so heavily focused on repurposing legacy content rather the developing consistent original entertainment that matches that produced by Netflix, Amazon and Apple.

In my opinion, investors need to be careful about Netflix's valuation, which is significantly higher than Apple's and just slightly lower than Amazon's. I think it is also important to remember how much more of a moat Amazon commands in physical and technology infrastructure than Netflix, whose moat is largely dependent on the quality of its internet platform and its content. Therefore, Amazon can reliably command a higher valuation for extended periods of time because of this.

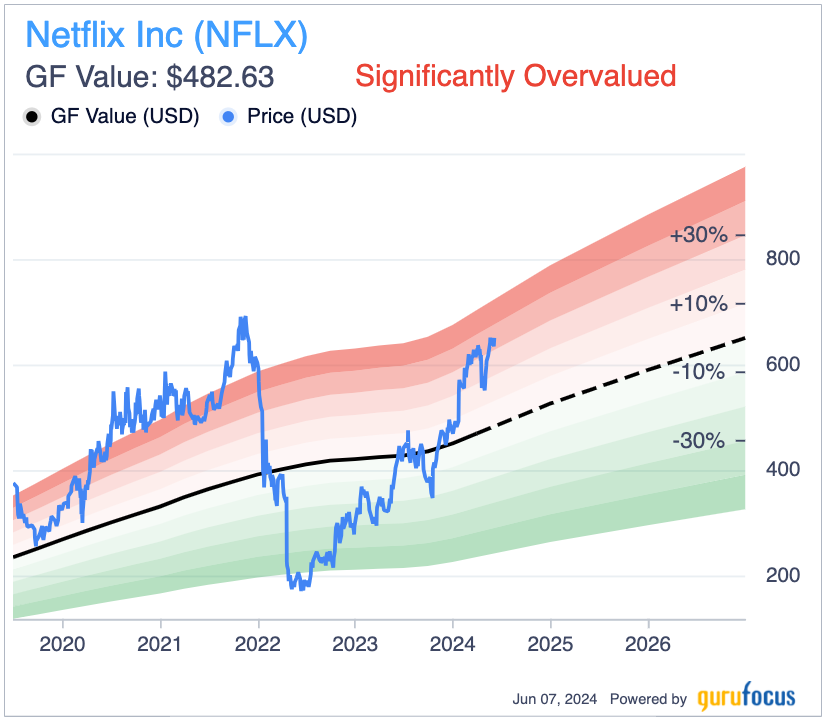

The GF Value chart shows Netflix to be significantly overvalued, meaning the stock is likely to experience downside volatility based on historical and future financial results and valuation factors.

Netflix's price-earnings ratio of 45 is significantly lower than its 10-year median of 117. Additionally, as its net income margin has increased significantly, from its its 10-year median of 8.47% to 18.42% today, investors are likely getting the stock at a reasonable valuation, even if it is significantly higher than fair value. Investing at these levels may mean losses are born for potentially two years or more before price growth stabilizes again due to a balance in the valuation. This is why I do not consider investing at the current price a good idea, despite all of the other strengths the business has going for it.

Risk analysis

Based on my own experiences with these companies and my research into their content and developments, I think there is a moderate long-term risk that is undervalued by the market at the moment for Netflix. Because the company has such a wide portfolio of content and less financial backing than Amazon and Apple's offerings, it runs the risk of losing its reputation as being desirable for online entertainment. I think cultivating allure in the creative industries is very challenging, and while Netflix has managed this already, maintaining this allure is often even harder than its initial cultivation. Netflix will need to constantly monitor what is well-received and not well-received by its customers to stay competitive. As Amazon and Apple both have an immensely deep focus on customer satisfaction and the user experience, over the long term, they might dwarf any attempts at dominance in the field by Netflix.

In addition, Netflix's international expansion plans come with challenges in talent acquisition and retention. Even though I believe the company's strategy of developing foreign films catered to each region is clever, it will need to continue to make sure it hires some of the best and most authentic creative talent in these regions to make this strategy an ongoing success. It also should not be underestimated how already saturated the markets are for online entertainment in Asia and Europe, the Middle East and Africa, as core examples. Major competitors to Netflix in Asia, which is considered to become one of the highest-growth markets in the future, include Tencent (TCEHY) Video, iQIYI (NASDAQ:IQ) (often referred to as the Netflix of China) and Viu.

Key elements

Netflix is one of the leading online entertainment companies in the world, with its most significant Western competitors being Amazon Prime Video and Apple TV+. Netflix has developed a clever expansion strategy that focuses on producing foreign films in emerging markets.

The stock is likely significantly overvalued at its current price, but the fundamentals are compelling against its major competitors. Netflix has delivered an almost equal price return CAGR over the past decade to Amazon. However, I do not consider allocating to Netflix at the current price a wise decision, as I believe it is likely the stock will experience some downside volatility over the next two years.

Netflix will likely face challenges in talent acquisition and retention in cultivating authentic international films that are competitive in markets that are already saturated by competitors. In addition, I think there is a significant risk the platform gets a reputation for lower overall quality long term as a result of less financial backing than major competitors.

Conclusion

Netflix is a strong company, and I believe it is likely to perform very well over the next two decades in terms of delivering strong price returns. However, at the present price, I think it is worth looking elsewhere to find strong growth companies that offer a more reasonable valuation. Long-term Netflix shareholders should also consider the potential complications that could occur in its international expansion strategy, which could reduce the investment's merit, alongside potential issues that may become prevalent in lower-quality content on its platform compared to larger competitors.

This article first appeared on GuruFocus.