Yahoo Finance

Yahoo Finance The past three years for PointsBet Holdings (ASX:PBH) investors has not been profitable

PointsBet Holdings Limited (ASX:PBH) shareholders should be happy to see the share price up 14% in the last month. But only the myopic could ignore the astounding decline over three years. Indeed, the share price is down a whopping 96% in the last three years. So we're relieved for long term holders to see a bit of uplift. The thing to think about is whether the business has really turned around. While a drop like that is definitely a body blow, money isn't as important as health and happiness.

Since shareholders are down over the longer term, lets look at the underlying fundamentals over the that time and see if they've been consistent with returns.

View our latest analysis for PointsBet Holdings

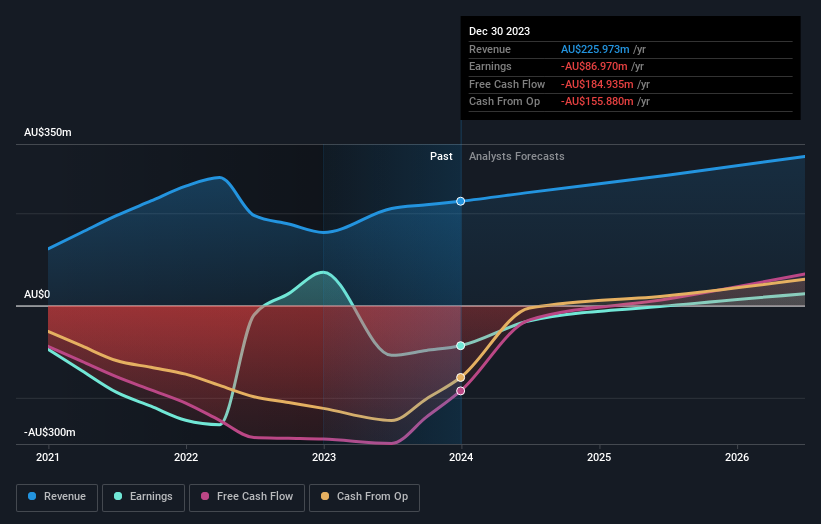

PointsBet Holdings isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. When a company doesn't make profits, we'd generally hope to see good revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In the last three years, PointsBet Holdings saw its revenue grow by 6.9% per year, compound. That's not a very high growth rate considering it doesn't make profits. But the share price crash at 25% per year does seem a bit harsh! We generally don't try to 'catch the falling knife'. Before considering a purchase, take a look at the losses the company is racking up.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

We consider it positive that insiders have made significant purchases in the last year. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. You can see what analysts are predicting for PointsBet Holdings in this interactive graph of future profit estimates.

What About The Total Shareholder Return (TSR)?

We've already covered PointsBet Holdings' share price action, but we should also mention its total shareholder return (TSR). The TSR attempts to capture the value of dividends (as if they were reinvested) as well as any spin-offs or discounted capital raisings offered to shareholders. We note that PointsBet Holdings' TSR, at -81% is higher than its share price return of -96%. When you consider it hasn't been paying a dividend, this data suggests shareholders have benefitted from a spin-off, or had the opportunity to acquire attractively priced shares in a discounted capital raising.

A Different Perspective

It's nice to see that PointsBet Holdings shareholders have received a total shareholder return of 84% over the last year. That gain is better than the annual TSR over five years, which is 5%. Therefore it seems like sentiment around the company has been positive lately. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. It's always interesting to track share price performance over the longer term. But to understand PointsBet Holdings better, we need to consider many other factors. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with PointsBet Holdings , and understanding them should be part of your investment process.

PointsBet Holdings is not the only stock insiders are buying. So take a peek at this free list of small cap companies at attractive valuations which insiders have been buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.