Yahoo Finance

Yahoo Finance Reasons Why Lemonade (LMND) Stock is an Attractive Pick Now

Lemonade, Inc. LMND is well-poised to gain from higher net added customers, growth in overall average policy value, expanded geographic footprint, growth in premiums placed with third-party insurance companies and a solid capital position.

Growth Projections

The Zacks Consensus Estimate for Lemonade’s 2024 earnings per share indicates a year-over-year increase of 13.5%. The consensus estimate for revenues is pegged at $517.09 million, implying a year-over-year improvement of 20.3%.

The consensus estimate for 2025 earnings per share and revenues indicates an increase of 18.3% and 29.3%, respectively, from the corresponding 2024 estimates.

Earnings Surprise History

Lemonade has a decent surprise history. Its earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 12.82%.

Zacks Rank & Price Performance

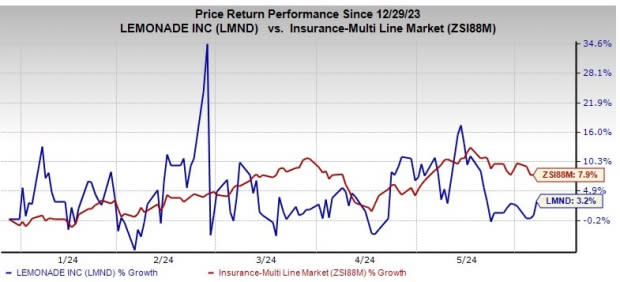

LMND currently carries a Zacks Rank #2 (Buy). Year to date (YTD), the stock has gained 3.2% compared with the industry’s growth of 7.9%.

Image Source: Zacks Investment Research

Business Tailwinds

Higher net added customers year over year, expanded geographic footprint and product offerings are likely to boost gross written premium.

In-force premium is likely to have been aided by an increase in customer base as well as an improvement in premium per customer.

The increasing prevalence of multiple policies per customer, growth in the overall average policy value and continued shift in the mix of underlying products toward higher value policies are likely to drive premium per customer year.

For the second quarter of 2024, Lemonade expects an in-force premium between $839 million and $841 million and a gross earned premium in the range of $197-$199 million.

LMND anticipates revenues between $118 million and $120 million for the second quarter of 2024.

For 2024, the company expects an in-force premium between $940 million and $944 million and a gross earned premium in the band of $818-$822 million.

For 2024, revenues are expected in the range of $511-$515 million.

Diversification of the company's investment portfolio with higher returns and lower investment expenses are likely to drive net investment income.

Commission and Other Income is expected to increase on the back of growth in premiums placed with third-party insurance companies and sublease income from the New York and San Francisco office space.

The insurer boasts a solid capital position. Its existing cash and cash equivalents will be sufficient to meet the working capital, liquidity and capital expenditure needs for at least the next 12 months.

Other Stocks to Consider

Some other top-ranked stocks from the multi-line insurance industry are EverQuote, Inc. EVER, Old Republic International Corporation ORI and Radian Group Inc. RDN, each carrying a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

EverQuote’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 65.16%. Shares of EVER have surged 90.5% YTD.

The Zacks Consensus Estimate for EVER’s 2024 and 2025 earnings implies year-over-year growth of 102.6% and 362.50%, respectively.

Old Republic International has a solid track record of beating earnings estimates in three of the trailing four quarters and missing in one, the average being 6.61%. Shares of ORI have gained 4.3% YTD.

The Zacks Consensus Estimate for ORI’s 2024 and 2025 earnings implies year-over-year growth of 3.8% and 4.4%, respectively.

Radian has a solid track record of beating earnings estimates in each of the trailing four quarters, the average being 22.79%. Shares of RDN have climbed 9.1% YTD.

The Zacks Consensus Estimate for RDN’s 2024 and 2025 revenues implies year-over-year growth of 8.2% and 4.9%, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Radian Group Inc. (RDN) : Free Stock Analysis Report

EverQuote, Inc. (EVER) : Free Stock Analysis Report

Old Republic International Corporation (ORI) : Free Stock Analysis Report

Lemonade, Inc. (LMND) : Free Stock Analysis Report