Yahoo Finance

Yahoo Finance These 3 Value Stocks Are Absurdly Cheap Right Now

Value investing often ends up leading investors into just one or two out-of-favor sectors. You can't create a diversified portfolio going that route. So it's important to broaden your horizons, and at times your view of what constitutes value. Here are three stocks from vastly different industries that all look absurdly cheap right now: Twitter (NYSE: TWTR) in the technology space, ExxonMobil (NYSE: XOM) in energy, and Abbvie (NYSE: ABBV) in pharmaceuticals.

Believe it or not, Twitter is a value

Brian Stoffel (Twitter): I'm not your traditional value investor. Five stocks constitute over 50% of my real-life holdings. One isn't profitable, and the average P/E of the other four stocks is north of 50! With that as a backdrop, of all the stocks I own, Twitter appears to be the best value play right now.

Image source: Getty Images.

Before you roll your eyes, consider this: The company may not ever reach the same user base as Facebook -- and that's OK. CEO Jack Dorsey has largely accepted this, and narrowed Twitter's workforce and scope to match this reality. That has resulted in a much more profitable venture: While "monetizable daily active users" (mDAU) were up 9% in the fourth quarter of 2018, non-GAAP net income jumped a remarkable 73%.

Twitter is wrestling with a lot of issues right now -- none more so than how to police abusive behavior without enforcing a nanny-state that tramples on the free speech rights of its users. That's a herculean task that few have ever faced before and none -- including Facebook -- have ever managed. It also has investors pessimistic.

But that pessimism has created opportunity. Twitter is the undeniable source for live, in-the-moment events. It has signed over 100 partnerships as a result. And over the past 12 months, it generated $1.34 billion in cash from operations -- and free cash flow of $856 million. The company currently has a P/E below 19.

It might not sound like value to most, but remember that free cash flow grew by 55% last year. And that was despite capital expenditures jumping 73%. The fastest-growing companies will often never be considered to have value stocks, but with Twitter, you might be getting the next best thing: growth at a very reasonable price.

Act now before investors catch on

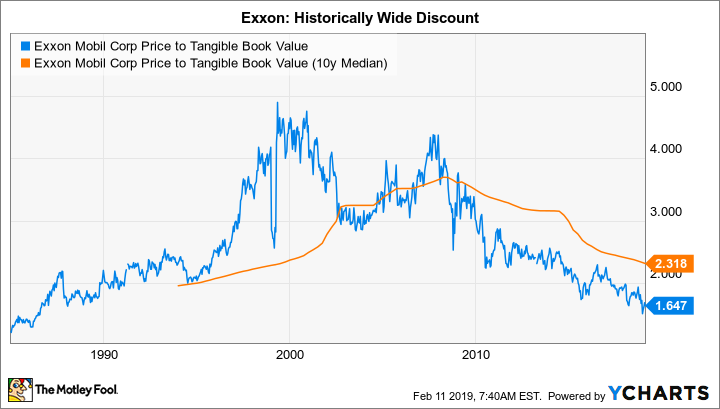

Reuben Gregg Brewer (ExxonMobil Corporation): The shares of integrated energy giant ExxonMobil are trading near 30-year lows based on price to tangible book value (PTBV). Its current PTVB, meanwhile, is nearly 30% below its 10-year average for the metric. For reference, peer Chevron, also trading at a multiyear-low PTVB, is only 10% below its 10-year average for this valuation metric. Exxon looks absurdly cheap right now. Which helps explain the impressive 4.4% dividend yield.

Investors are clearly worried, and perhaps rightly so. In recent years, Exxon's production has fallen, and its return on capital employed (which tracks how well it puts shareholder money to work) has dropped into the middle of its peer group. But the oil giant has a plan to get back on track, with a long-term goal of roughly doubling earnings by 2025. That goal, meanwhile, only requires that oil sell for around $50 to $60 a barrel.

XOM Price to Tangible Book Value data by YCharts.

Early results are starting to look pretty encouraging. For example, production increased sequentially between the second and third quarters and between the third and fourth quarters. That's a notable shift from the steady drift lower over the last few years. And that upturn was driven by just one of the company's long-term production growth drivers (onshore U.S. oil drilling). Its ratio of return on capital employed, meanwhile, has started to tick up again as Exxon has moved to take greater control of its big growth projects.

Not only does Exxon look cheap, but it also looks like it's at a key inflection point. Once investors catch on to that, Exxon's discount will likely narrow...and that big dividend will shrink. Now is the time to do a deep dive.

A big pharma that's a big bargain

Keith Speights (AbbVie): I'd call a stock that trades for only 8.5 times expected earnings inexpensive. If the stock also was likely to generate average annual earnings growth of close to 10% over the next five years, I'd say it was a bargain. And if the stock also paid out a dividend that yielded over 5%, I'd jump at the chance to buy it. One stock that meets all of these criteria is AbbVie.

There's usually a reason that a stock has an attractive valuation. In AbbVie's case, investors are worried about what will happen to the company's fortunes with its top-selling drug, Humira, facing competition from biosimilars. I don't think those concerns should make long-term investors afraid of AbbVie, though.

For one thing, Humira won't be threatened by biosimilars in the U.S. market until 2023. Humira appears likely to remain the world's best-selling drug at least through 2024. That gives AbbVie plenty of time for its other products and pipeline candidates to step up.

Cancer drugs Imbruvica and Venclexta continue to enjoy strong momentum. Orilissa, which has already won approval for managing endometriosis pain and could secure another indication in treating uterine fibroids, has blockbuster potential. AbbVie also should have huge winners on the way with immunology drugs risankizumab and upadacitinib.

AbbVie believes that it will more than offset the anticipated sales declines for Humira. With its bargain valuation and attractive dividend, I think this big pharma stock is a solid pick right now

More From The Motley Fool

Brian Stoffel owns shares of Twitter. Keith Speights owns shares of AbbVie and Chevron. Reuben Gregg Brewer owns shares of ExxonMobil. The Motley Fool owns shares of and recommends Twitter. The Motley Fool has a disclosure policy.