Yahoo Finance

Yahoo Finance Should You Add UBER to Your Portfolio Ahead of Q1 Earnings?

Uber Technologies UBER, a leading ride-hailing company, is set to report first-quarter 2024 results on May 8, before market open. Ahead of its earnings, investors may be deliberating on whether to purchase the stock before May 8 or wait for a better entry point.

Impressive Price Performance

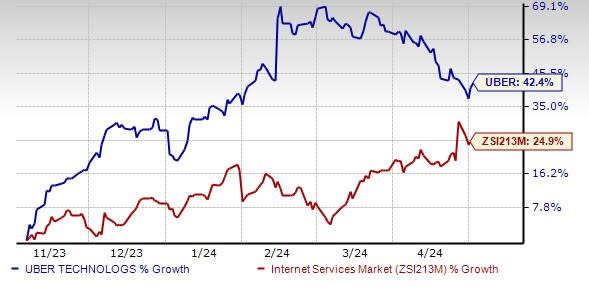

Driven by its efforts to diversify and expand its ride-hailing and delivery businesses, the company has performed impressively on the bourses of late. The stock has appreciated 42.4% over the past six months, handily surpassing its industry’s 24.9% growth.

Image Source: Zacks Investment Research

Upbeat Gross Bookings Likely to Aid UBER’s Q1 Earnings

With economic activities returning to normal levels in the post-pandemic scenario, people are traveling to work and other places as before. UBER’s Mobility business has been seeing buoyant demand. With customer traffic picking up, gross bookings from the unit are likely to have been impressive, in turn aiding first-quarter results. We expect gross bookings from the Mobility segment in the March quarter to grow 27.4% on a year-over-year basis.

Uber’s Delivery business is also expected to have performed well in the to-be-reported quarter. We expect gross bookings from the Delivery segment in the March quarter to grow 13% on a year-over-year basis. Total trips are expected to soar 23.6% year over year in the March quarter, per our model.

Favorable Estimate Revisions & Style Score

The Zacks Consensus Estimate for first-quarter earnings has been revised 5% upward over the past 60 days, reflecting investors’ confidence in the stock.

The stock’s Momentum Score of A further highlights its attractiveness.

What the Zacks Model Unveils

Our proven model does not conclusively predict an earnings beat for UBER this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is not the case here.

UBER sports a Zacks Rank #1 at present but its Earnings ESP is -5.46%.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Fundamental Strength

For long-term investors a single quarter’s results are not so important. They would rather base their investment decision on the underlying fundamentals. UBER scores impressively on that front, driven by its strong operating model.

Diversification is imperative for big companies to reduce risks and UBER has excelled in this area. It has engaged in numerous strategic acquisitions, geographic and product diversifications and innovations. Even though Uber’s primary business is ride-sharing, it has diversified into food delivery and freight over time.

Uber’s endeavors to expand into the international markets are commendable and provide it with the benefits of geographical diversification. Prudent investments enable it to extend services and solidify its comprehensive offerings. Its focus on disciplined spending and cost-cutting measures also bodes well as far as bottom-line growth is concerned.

Strong Growth Prospects

The Zacks Consensus Estimate for 2024 earnings is pegged at $1.23, indicating 41.4% growth from the 2023 actuals. The company’s long-term (3-5 years) earnings growth rate is an impressive 51.8%, higher than its industry’s 22.8%.

Thus, we believe investors should add UBER stock to their portfolios ahead of its earnings release on May 8 for healthy returns. Its current Zacks Rank supports our thesis.

Other Tech Stocks to Consider

Crexendo (CXDO) provides cloud communication platforms and services, as well as video collaboration and managed IT services. The stock sports a Zacks Rank #1.

The Zacks Consensus Estimate for 2024 earnings has moved 35.3% north in the past 60 days and is currently pegged at 23 cents per share. CXDO surpassed the Zacks Consensus Estimate for earnings in three of the past four quarters (missing the mark once), the average beat being 204.2%.

Alphabet GOOGL, which currently sports a Zacks Rank #1, is being well-served by its a deepening focus on generative AI technology. Its robust cloud division is aiding substantial revenue growth.

The Zacks Consensus Estimate for its 2024 earnings has moved north by 11.8% in the past 60 days and is currently pegged at $7.57 per share. Alphabet surpassed the Zacks Consensus Estimate for earnings in each of the past four quarters, with the average beat being 11.34%.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Crexendo Inc. (CXDO) : Free Stock Analysis Report

Uber Technologies, Inc. (UBER) : Free Stock Analysis Report