Yahoo Finance

Yahoo Finance Align Technology (ALGN) Q1 Earnings Beat, Margins Contract

Align Technology, Inc. ALGN delivered first-quarter 2023 adjusted earnings per share (EPS) of $1.82, down 19.1% from the year-ago earnings. However, the EPS exceeded the Zacks Consensus Estimate by 7.7% in the first quarter.

GAAP EPS for the quarter was $1.14, reflecting a 33% decline year over year.

Revenues

Revenues declined 3.1% year over year to $943.1 million in the quarter but beat the Zacks Consensus Estimate by 3.8%. Revenues were impacted by the unfavorable foreign exchange of approximately $34.9 million year over year.

At the constant exchange rate or CER, total revenues in the first quarter dropped 3.6% year over year.

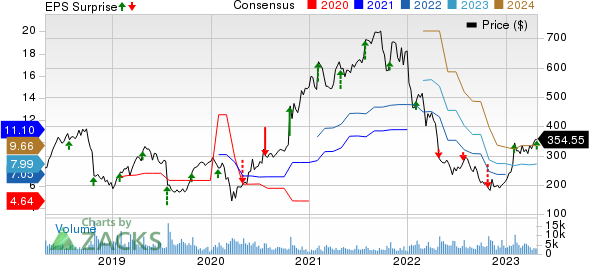

Align Technology, Inc. Price, Consensus and EPS Surprise

Align Technology, Inc. price-consensus-eps-surprise-chart | Align Technology, Inc. Quote

Segments in Detail

In the first quarter, revenues in the Clear Aligner segment were down 2.5% year over year to $789.8 million. Revenues were unfavorably impacted by lower volumes and lower Average Selling Price (ASP), including a foreign exchange headwind of approximately $29.1 million (or 3.6%) year over year. This was partially offset by higher non-case revenues.

Total Clear Aligner shipments during the quarter amounted to 575,395, down 3.9% year over year.

Revenues from Imaging Systems & CAD/CAM Services were down 6.2% to $153.3 million in the quarter. Lower scanner volumes were partially offset by higher services revenues from the larger installed base of scanners sold and increased non-system revenues related to the company’s certified preowned and leasing and rental programs and favorable ASPs. Revenues witnessed an unfavorable currency impact of 3.6% year over year.

Margins

The gross profit in the first quarter was $660.7 million, reflecting a 6.7% decline year over year. The gross margin in the quarter under review contracted 284 basis points (bps) year over year to 70.1% due to a 7.1% increase in the cost of net revenues.

During the quarter, Align Technology witnessed a 0.01% increase in SG&A expenses to $439.7 million and a 21.8% rise in research and development expenses to $87.4 million. The company continues to strategically prioritize investments in go-to-market activities and R&D to drive growth.

The operating income in the quarter under review was $133.5 million, highlighting a decline of 32.6%. The operating margin contracted 620 bps to 14.2%.

Financial Details

Align Technology exited the first quarter of 2023 with cash and cash equivalents of $832.4 million compared with the $942 million recorded at the end of 2022.

Cumulative net cash provided by operating activities at the end of the first quarter was $199.9 million compared with $30.5 million a year ago.

The company repurchased nearly 942 thousand shares during the quarter for a total purchase price of $290.0 million. This completes Align Technology’s existing 2021 $1 billion Stock Repurchase Program, the $200.0 million Accelerated Share Repurchase ("ASR") program from the fourth quarter of 2022 and a $250.0 million ASR program from the first quarter of 2023.

Currently, $1.0 billion is available for repurchases under ALGN’s $1.0 billion Stock Repurchase Program, authorized in the first quarter of 2023, to succeed the 2021 $1 billion program.

Full-Year Guidance

Align Technology reaffirmed its 2023 outlook, which was originally announced during its fourth-quarter 2022 earnings call.

The company expects to report a 2023 GAAP operating margin of slightly more than 16% and an adjusted operating margin of slightly higher than 20% (unchanged from the previous guidance). ALGN’s GAAP operating margin for 2022 was 17.2%, while the adjusted operating margin was 21.5%.

For 2023, the company expects investments in capital expenditures to exceed $200 million (unchanged). Capital expenditures are primarily related to building construction and improvements and additional manufacturing capacity to support Align Technology’s international expansion as well.

For the second quarter of 2023, ALGN anticipates revenues to be in the range of $980 million-$1000 million. The Zacks Consensus Estimate for the same is pegged at $946.5 million.

Align Technology anticipates its adjusted gross margin to remain flat to slightly rise from the first quarter and the adjusted operating margin to be up by approximately 1 point sequentially.

Our Take

Align Technology exited the first quarter of 2023 with an earnings and revenue beat. The company’s Clear Aligner non-case revenues increased year over year, driven by continued growth from the Invisalign Doctor subscription program and sales of Vivera Retainers. ALGN’s recent launch of the Invisalign Comprehensive three and three product was also well received in the market and holds potential for faster revenue recognition than traditional Invisalign comprehensive products.

On the flip side, the year-over-year performance was sluggish. The quarter also witnessed a significant foreign exchange impact.

The contraction of both margins is worrisome. Align Technology’s operating expenses reported during the quarter increased due to higher incentive compensations and continued investments in sales and R&D activities. This was partially offset by controlled spending on advertising and marketing as part of ALGN’s efforts to manage costs efficiently.

Recently, Align Technology announced a $75 million equity investment in Heartland Dental, a multidisciplinary DSO with GDP and ortho practices across the United States. The collaboration underpins the company’s efforts to accelerate the adoption of digital orthodontics and restorative dentistry.

Zacks Rank and Key Picks

Align Technology currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the broader medical space that have announced quarterly results are Insulet PODD, Avanos Medical AVNS and Henry Schein HSIC.

Insulet, sporting a Zacks Rank #1 (Strong Buy), reported a fourth-quarter 2022 adjusted EPS of 55 cents, beating the Zacks Consensus Estimate by 129.2%. Revenues of $370 million outpaced the consensus estimate by 11.9%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Insulet has an estimated earnings growth rate of 57.8% for the next year. PODD’s earnings surpassed estimates in three of the trailing four quarters and missed the same in one, the average being 59.8%.

Avanos Medical, carrying a Zacks Rank #2 (Buy), reported a fourth-quarter 2022 adjusted EPS of 60 cents, which beat the Zacks Consensus Estimate by 25%. Revenues of $218 million outpaced the consensus estimate by 1.1%.

Avanos Medical has an earnings yield of 5.55% compared to the industry’s -6.88%. AVNS’ earnings surpassed estimates in all the trailing four quarters, the average being 11.01%.

Henry Schein reported fourth-quarter 2022 adjusted earnings of $1.21 per share, which matched the Zacks Consensus Estimate. Revenues of $3.37 billion surpassed the Zacks Consensus Estimate by 0.4%. It currently has a Zacks Rank #2.

Henry Schein has an earnings yield of 6.28% compared with the industry’s 4.55%. HSIC’s earnings surpassed estimates in three of the trailing four quarters and matched the same in one, the average surprise being 2.97%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Align Technology, Inc. (ALGN) : Free Stock Analysis Report

Henry Schein, Inc. (HSIC) : Free Stock Analysis Report

Insulet Corporation (PODD) : Free Stock Analysis Report

AVANOS MEDICAL, INC. (AVNS) : Free Stock Analysis Report