Yahoo Finance

Yahoo Finance Asana's (NYSE:ASAN) Correction is Unsurprising Given the Parabolic Rise in 2021

This article first appeared on Simply Wall St News.

Extreme valuations often bring the growth companies into peculiar situations. Optimism is contagious, often causing multi-bagger parabolic moves, yet prices rarely stay up there for long.

Such is a case with Asana, Inc. (NYSE: ASAN), a growth stock that had a valuation over US$30b, before crashing over 50% in a matter of weeks, as the decelerating revenue spooked the investors.

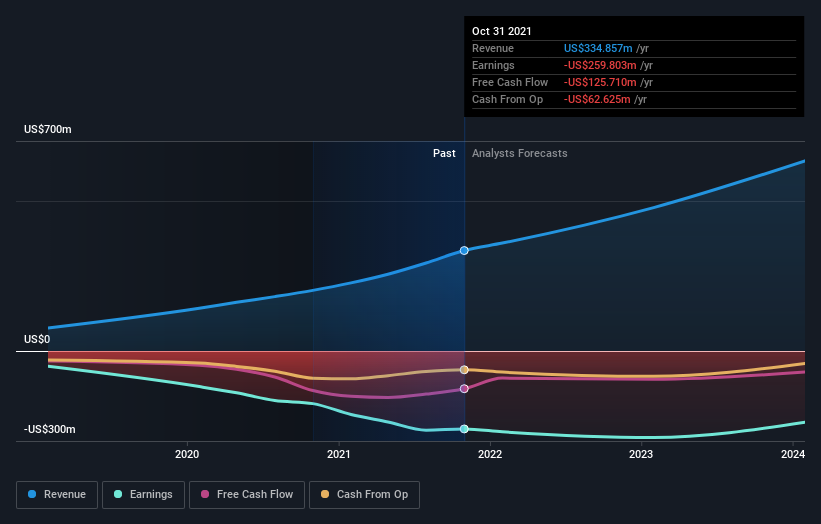

Check out our latest analysis for Asana

Q3 Earnings Results

Non-GAAP EPS: -US$0.23 (beat by US$0.04)

GAAP EPS: -US$0.37 (beat by US$0.03)

Revenue: US$100.34m (beat by US$6.44m)

For Q4, the company sees revenue between US$104.5 and US$105.5m, vs. a consensus of US$98.73m. CEO Dustin Moskovitz praised the fact that the revenue surpassed US$100m for the first time, pointing out the 96% Y/Y growth for customers spending US$5,000 or more and positive momentum with large customers (spending over US$50,000) for the third consecutive quarter.

However, 2 growth metrics showed a slowdown, which seems to have spooked the markets. First, the third quarter revenue slowed to 70% on a Y/Y basis, compared to 72% in Q2. Furthermore, Q3 billings grew 56% on the Y/Y basis, significantly lower than 81% from the second quarter.

Analyst Ittai Kidron of Oppenheimer argued that this view could be misleading, given: "the changing mix of monthly and annual subscriptions, as well as the impact of large deals. "Mr.Kidron keeps an outperform rating and a US$115 price target on Asana.

A Handle on the Debt

Despite being unprofitable, Asana has reasonable control over its financial health, as its short-term assets exceed its short-term and long-term liabilities. Therefore, cash burn is not a reason for concern.

The current debt is just over US$35m, which is minuscule given the multi-billion dollar market cap.

What kind of growth will Asana generate?

Investors looking for growth in their portfolio may want to consider the company's prospects before buying its shares. Although value investors would argue that it's the intrinsic value relative to the price that matters the most, a more compelling investment thesis would be high growth potential at a reasonable price.

Though in the case of Asana, it is expected to deliver a relatively unexciting earnings growth of 3.7%, which doesn't help build up its investment thesis. Growth doesn't appear to be the main reason for a buy decision for the company, at least in the near term.

What this means for you:

Are you a shareholder? Shareholders may be asking a different question at this current price – should I sell? If you believe ASAN should trade below its current price, selling high and buying it back up again when its price falls towards its real value can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you've been keeping an eye on ASAN for a while, this significant drop might sound the alarms. While some analysts believe the correction is an overreaction from the market, keep in mind that the broad market is still experiencing a correction and can drag the stock further down. Always keep the bigger picture about the sector and the overall market in mind.

If you'd like to know more about Asana as a business, it's important to be aware of any risks it's facing. Case in point: We've spotted 3 warning signs for Asana you should be aware of.

If you are no longer interested in Asana, you can use our free platform to see our list of over 50 other stocks with high growth potential.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.