Yahoo Finance

Yahoo Finance Aterian's (NASDAQ:ATER) Stock Dilution is Not Worth The Risk

This article first appeared on Simply Wall St News.

Although summertime is generally seen as a calmer period of the stock market, those rules do not apply in the high-growth small-cap universe. During the last quarter, Aterian, Inc.'s(NASDAQ: ATER)price went as low as US$3.04 and as high as US$19.10.

Yet, short interest remains elevated. This article will look at the latest developments, as well as examine the state of the balance sheet.

For more information, check out our latest analysis for Aterian

Platform Launch and a Lender Deal

Aterian just announced a beta version launch of its affiliate marketing platform. The platform "DealMojo" connects Amazon sellers with parties interested in promoting their products. Aterian claims their partnership network with over 300 monthly visitors will help drive the sales and invite interested sellers to sign-up for the service.

Meanwhile, the company reached a deal on debt repayment with its lender, High Trail. Under the new refinancing terms, the company will pay US$66.3m plus interest in shares. The remaining US$25m will mature in April 2023.

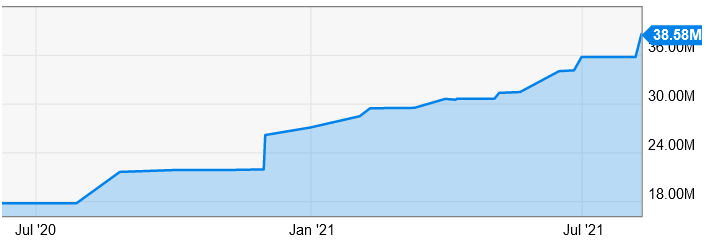

If you examine the chart below, you'll notice that the number of shares outstanding more than doubled over the last 14 months. As per the new deal, Aterian cannot issue new shares until November 1, 2021.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't quickly pay it off, either by raising capital or with its cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing.

However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet.

By replacing dilution, though, debt can be an excellent tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels together.

What Is Aterian's Net Debt?

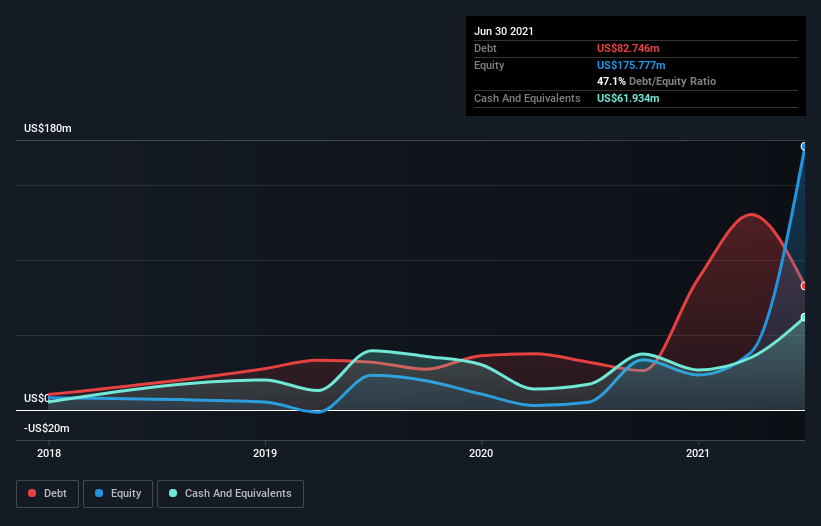

As you can see below, at the end of June 2021, Aterian had US$82.7m of debt, up from US$31.9m a year ago. Click the image for more detail.

On the flip side, it has US$61.9m in cash leading to net debt of about US$20.8m.

How Healthy Is Aterian's Balance Sheet?

We can see from the most recent balance sheet that Aterian had liabilities of US$161.7m falling due within a year and liabilities of US$21.6m due beyond that. Offsetting these obligations, it had cash of US$61.9m as well as receivables valued at US$16.3m due within 12 months.

So its liabilities total US$105.1m more than the combination of its cash and short-term receivables.

Aterian has a market capitalization of US$481.4m, so it could very likely raise cash to ease its balance sheet if the need arose.

But we should closely examine whether it can manage its debt without dilution. There's no doubt that we learn most about debt from the balance sheet. But ultimately, the future profitability of the business will decide if Aterian can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Aterian reported revenue of US$217m, which is a gain of 43%, although it did not report any earnings before interest and tax. With any luck, the company will be able to grow its way to profitability.

Let the Buyer Beware

Despite the top-line growth, Aterian still had earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost US$29m at the EBIT level. Considering that, the liabilities mentioned above do not give us much confidence that the company should be using so much debt, especially through repeated dilution.

Quite frankly, we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that it bled US$18m in negative free cash flow over the last twelve months.

So suffice it to say we do consider the stock to be risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, Aterian has 2 warning signs (and 1 which is a bit concerning) we think you should know about.

It's often better to focus on companies that are free from net debt. You can access our free list of such companies (all with a track record of profit growth).

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com