Yahoo Finance

Yahoo Finance Barclays goes after Chase's hottest credit card with fresh yearly bonuses

Barclays (BCS) announced a new credit card today called the Arrival Premier, and it has a completely fresh strategy that could shake up the world of uber high-end credit cards.

There hasn’t been a “hot” new credit card in this category since Chase released the Sapphire Reserve card in 2016. Even after the Sapphire Reserve card’s bonus was slashed from a whopping 100,000 points — worth over $1,000 — to 50,000, it was a good deal for many people, earning back its $450 a year cost and much more.

American Express (AXP) attempted to usurp Chase’s card superiority with a new bonus for its Platinum card holders last April, but its offerings did not compare to Chase’s Sapphire Reserve.

In the world of credit cards, “churning” is very popular, and is something credit card companies do not like. Churning is when consumers get a new credit card a few times a year, spend until the requirements for a hefty sign-up bonus is met, and then put the card in a drawer and move on to the next one. Pulling this can often ding someone’s credit score by a few points, but occasionally doing this is a popular ploy for the disciplined individual looking to take advantage of big bonuses.

Barclays Arrival PremierObviously, banks don’t like this, because they don’t want customers to take the money and run, like a mouse that carefully removes the cheese from the trap. (Not that a card is tantamount to a mouse trap, but you get the idea.) Avoiding this dynamic is where Barclays’ new strategy comes in.

Instead of offering a standard bonus of, say, 50,000 points for signing up and spending $4,000 in three months, Barclays’ rewards loyalty by giving a bonus of 25,000 miles if you spend $25,000 in a year (you still get 15,000 if you spend $15,000).

This annual recurring bonus is on top of 2x miles per every dollar spent on regular purchases. As with the Chase’s Sapphire Reserve, the card offers reimbursements for Global Entry, lounge access at airports, waived foreign transaction fees, and travel cancellation and accident/delay insurance.

The Arrival Premier costs $150 per year, which is identical to the Chase Sapphire Reserve card if you subtract the annual $300 travel credit (money you get back if you spend $300 on taxis, flights, ferries or anything travel related) from Chase’s $450 sticker price.

Churners and consumers who travel — the Arrival Premier is chiefly a travel card after all — can calculate whether it’s advantageous to try this card or switch from the Sapphire Reserve. (For churners, it would mean a big commitment.)

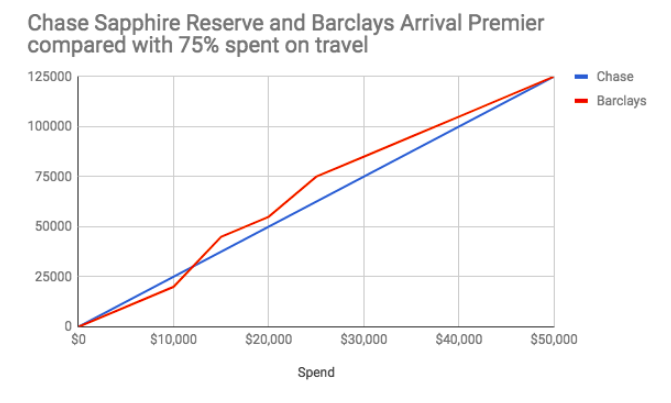

So what’s better, this new Barclays card or the Sapphire Reserve? It depends on two things, how much you spend and how much of it is on travel, which Chase rewards to the tune of 3X. Spending $15,000 on 100% travel would mean 45,000 miles for Barclays and 45,000 points for Chase. (For simplicity’s sake, the value is similar for a Barclays mile and a Chase point, though Sapphire Reserve holders’ points are 50% more valuable when used through Chase’s travel portal.)

Of course, you probably don’t do that, which is where Barclays shows its advantage, despite the high thresholds to qualify for the bonuses. If you spend any less than 75% on travel, Barclays may be advantageous in the long run. That percent may be a little lower given the redemption advantages through Chase’s portal, but after four years of maximum bonuses, you’d have doubled Chase’s hefty signup no matter what.

Below is a graph of how it works, minus Chase’s initial bonus and redeeming differences.

In the end, Barclays really gives Chase a run for its money and in the process may have solved the credit card loyalty problem.

Update: A previous version neglected to note that the 3X on the Chase card only applies to travel and dining categories.

—

Ethan Wolff-Mann is a writer at Yahoo Finance. Follow him on Twitter @ewolffmann. Confidential tip line: FinanceTips[at]oath[.com].

Read more

Online-only savings accounts are banking’s best-kept secret

Passive investing has changed one of the biggest retirement debates