Yahoo Finance

Yahoo Finance The biggest winners from the Fed regulatory relief proposal

Some of the nation’s largest banks are excited about the Federal Reserve’s decision to loosen post-crisis regulations put in place by the Dodd-Frank Act.

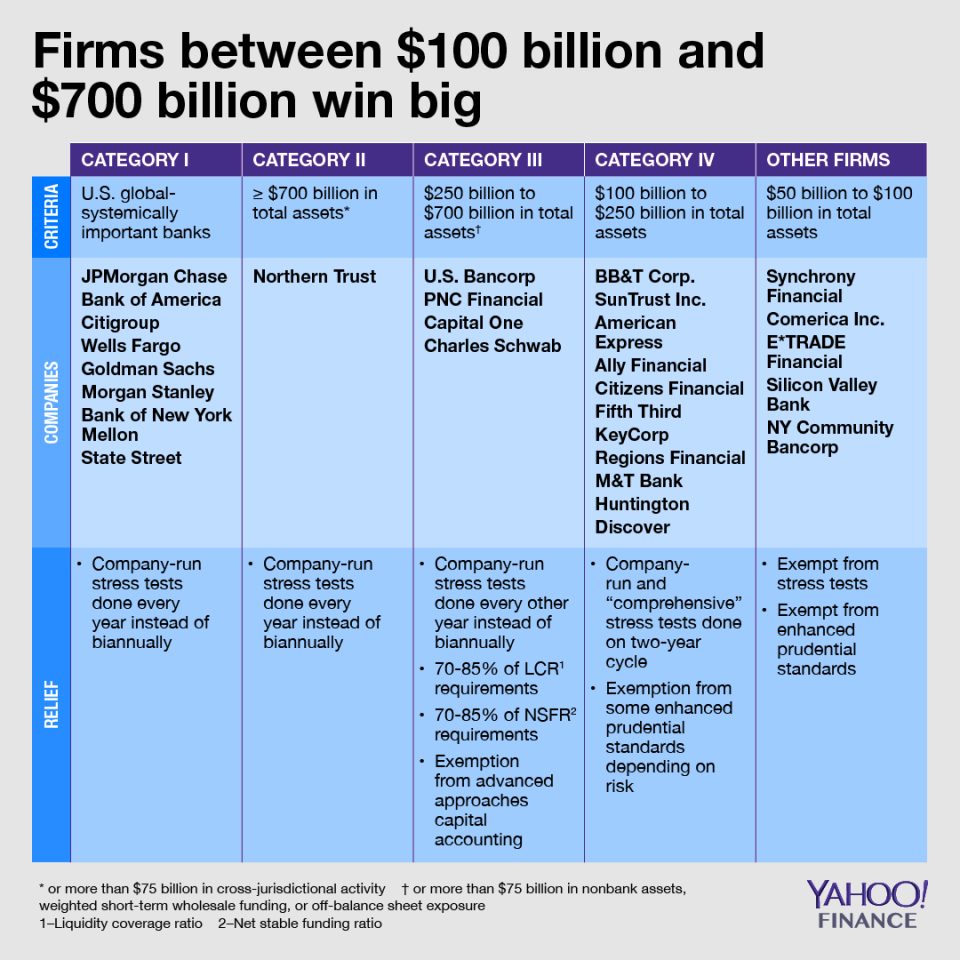

On Wednesday, the Fed followed through on legislation passed in May that would roll back some regulations on banks with less than $250 billion in total assets, but went above and beyond by extending regulatory relief to banks up to $700 billion in size.

As a result, U.S. Bancorp (USB), PNC Financial (PNC), Capital One (COF), and Charles Schwab (SCHW) will benefit from lower liquidity and funding requirements. The four companies total $1.47 trillion of total assets; for comparison, Wells Fargo (WFC) is a $1.88 trillion bank. Wells Fargo, JPMorgan Chase (JPM), Bank of America (BAC), Citigroup (C) and the four other globally-systemic banks will not see a reduction in their liquidity and capital requirements under the new regime.

“We appreciate that the banking agencies’ proposal acknowledges the real differences between the business model and risk profiles of Main Street banks, like PNC, and globally systemically important banks,” PNC spokesperson Marcey Zwiebel said.

A spokesperson for U.S. Bank said the proposal “strikes a good balance.” Charles Schwab declined to comment and Capital One did not respond to requests for comment.

‘Clear differentiation’

In May, President Donald Trump signed legislation requiring the bank regulators to roll back some post-crisis regulations on firms with between $50 billion and $250 billion in total assets. But Randal Quarles, the head of the Fed’s supervisory functions, has telegraphed an interest in pulling back red tape on the largest banks that are not globally systemic.

“I can see reason to apply a clear differentiation,” Quarles told Congress in early October.

Under the Fed’s proposal, the 29 largest U.S.-based banks and thrifts would be divided up into four categories based on their asset size and other factors like international activity and off-balance sheet exposure.

The smallest of the 29 — covering the likes of BB&T (BBT), SunTrust (STI) and American Express (AXP) — are in “category IV” and benefit from less frequent stress testing. Congress also gave the Fed the mandate to tailor its application of “enhanced prudential standards” like resolution planning and risk committees.

The bill did not require the Fed to remove regulatory requirements on “category III” banks, but the proposal did so anyway. All banks above $50 billion will have their company-run stress tests done at least every year instead of biannually.

Under former Fed Chair Janet Yellen, bank regulators implemented a liquidity coverage ratio that requires firms to hold a certain amount of high-quality liquid assets. The Fed also introduced a requirement for banks to have a certain amount of longer-term, stable sources of funding in a separate rule called the “net stable funding ratio.”

The new proposal, which will solicit public comment before going final, would decrease both regulatory requirements to somewhere between 70% and 85% of existing standards.

Jeremy Kress, a former Fed staffer who now teaches at the University of Michigan, told Yahoo Finance that he fears that the changes would weaken key safeguards against shocks to the financial system.

“It was more extreme than I expected,” said Kress. “[Their] actions tell me the Fed was not satisfied with how far the Senate bill went.”

But others feel the post-crisis requirements were set too high and are restrictive to banks’ businesses. Doug Landy, an attorney who represents banks with law firm Milbank, Tweed, Hadley and McCloy, said banks are beyond well-positioned in terms of liquidity and saw the proposal as a modest effort to reduce compliance costs.

“Those institutions have done a good job at insuring their funding,” Landy said.

The Fed did, however, draw a line with Northern Trust (NTRS). The bank, which has only $123.9 billion, was placed into an exclusive “category II” bucket where it will continue to face full-force liquidity and funding requirements due to a high global exposure from its payments activity.

A lingering question is how the Fed will regulate the U.S.-based subsidiaries of large foreign banks. The American arms of HSBC and TD Group, for example, are comparable in size to U.S. Bancorp, but the Fed said it would address the regulation of those banks in future rule-making.

Brian Cheung is a reporter covering the banking industry and the intersection of finance and policy for Yahoo Finance. You can follow him on Twitter @bcheungz.

Read more:

Midterms unlikely to halt Trump administration’s regulatory rollbacks.

Fed Vice Chair Quarles prefers ‘more gradual’ rate hikes

Prudential Financial to shed its post-crisis ‘too big to fail’ label