Yahoo Finance

Yahoo Finance Church & Dwight (CHD) Gains on Brand Strength Amid High Costs

Church & Dwight Co., Inc. CHD has established a robust position in the staple universe. The company’s success is attributed to robust consumer demand, bolstered by consistent innovation, new product launches and strategic acquisitions.

These upsides, along with efficient pricing and productivity gains, have been working well for the company. Encouragingly, management expects volumes to continue driving growth in 2024. However, elevated marketing costs and manufacturing cost inflation are a concerning factor.

Factors Driving CHD’s Growth

Church & Dwight has been benefiting from the favorable consumer demand for its brands. The company’s regular innovation, product introductions and acquisitions have helped it curate a solid portfolio. The company boasts 14 power brands, out of which THERABREATH, VITAFUSION, HERO, ARM &HAMMER, WATERPIK, BATISTE and OXICLEAN generate 70% of its revenues and profits. In 2023, the company’s domestic brands saw consumption growth in 10 of 17 categories.

Brand strength, efficient pricing and productivity gains have been working well. This was evident in its fourth-quarter 2023 results, wherein the top and bottom lines increased year over year and beat the Zacks Consensus Estimate. Organic sales increased 5.3% due to gains from volumes to the tune of 1.3%, a favorable product mix and pricing of 4%.

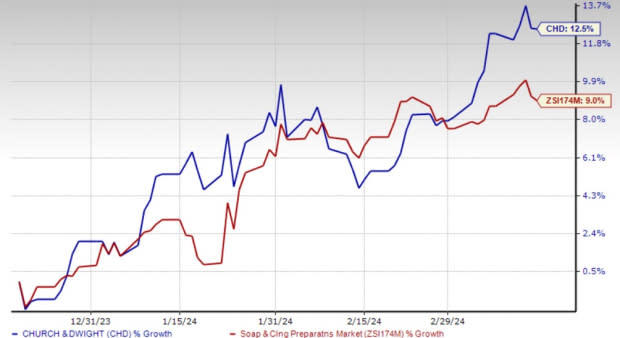

Image Source: Zacks Investment Research

Another factor working for Church & Dwight is the online channel. Global online sales, as a percentage of total consumer sales, stood at 20% in 2023. Carryover product pricing, mix, favorable volume and productivity are likely to remain drivers in 2024.

Church & Dwight expects 2024 reported and organic sales growth of 4-5%. For the first quarter of 2024, Church & Dwight expects a nearly 4% increase in reported organic sales.

Contributions from prudent buyouts have been adding to the company’s strength. Church & Dwight recently completed its latest buyout of the Hero Mighty Patch brand (or Hero) and other acne treatment products.

In December 2021, the company concluded the buyout of TheraBreath, a leading brand in the mouthwash category, which marks its 14th power brand. THERABREATH mouthwash and the HERO brand delivered impressive consumption growth and grew market share in the fourth quarter of 2023 and are expected to generate robust growth in 2024.

Cost Woes Prevail

Church & Dwight’s gross margin was partly hurt by manufacturing cost inflation in the fourth quarter of 2023. In 2024, the company expects to witness a rise in manufacturing costs, mainly due to capacity-related investments, a rise in third-party manufacturing expenses and moderate commodity inflation. The company has been undertaking increased marketing to fuel brand awareness, especially for new products and acquired brands. During the fourth quarter, marketing expenses increased by $29.3 million year over year to $219 million. As a percentage of net sales, the figure rose 100 bps to 14.3%.

Management expects marketing as a percentage of net sales to be around 11% in 2024 compared with 10.9% in 2023. In the first quarter of 2024, though management expects to witness gross margin expansion, it expects marketing expenses to increase. Consequently, it expects adjusted EPS of 85 cents for the quarter, flat year over year.

That said, the company projects 2024 adjusted earnings per share (EPS) growth of 7-9%, which includes a 1% drag associated with the MEGALAC business. Excluding the MEGALAC impact, adjusted EPS is likely to increase 8-10%.

Shares of this Zacks Rank #3 (Hold) company have rallied 12.5% in the past three months, outperforming the industry’s growth of 9%.

Solid Staple Picks

The Chef’s Warehouse CHEF, which engages in the distribution of specialty food products, currently carries a Zacks Rank #2 (Buy). CHEF has a trailing four-quarter earnings surprise of 3.2%, on average. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for The Chef’s Warehouse’s current fiscal-year sales and earnings suggests growth of 8.7% and 4.7%, respectively, from the year-ago reported numbers.

Vital Farms Inc. VITL offers a range of produced pasture-raised foods. It currently carries a Zacks Rank #2. VITL has a trailing four-quarter average earnings surprise of 155.4%.

The Zacks Consensus Estimate for Vital Farms’ current financial-year sales and earnings suggests growth of 20.2% and 28.8%, respectively, from the year-ago reported numbers.

Utz Brands Inc. UTZ manufactures a diverse portfolio of salty snacks, currently carrying a Zacks Rank #2. UTZ has a trailing four-quarter earnings surprise of 2.6% on average.

The Zacks Consensus Estimate for Utz Brands’ current financial-year earnings suggests growth of 19.3% from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Church & Dwight Co., Inc. (CHD) : Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF) : Free Stock Analysis Report

Vital Farms, Inc. (VITL) : Free Stock Analysis Report

Utz Brands, Inc. (UTZ) : Free Stock Analysis Report