Yahoo Finance

Yahoo Finance Cost Reduction Plans to Fuel Dean Foods, Soft Volumes Hurt

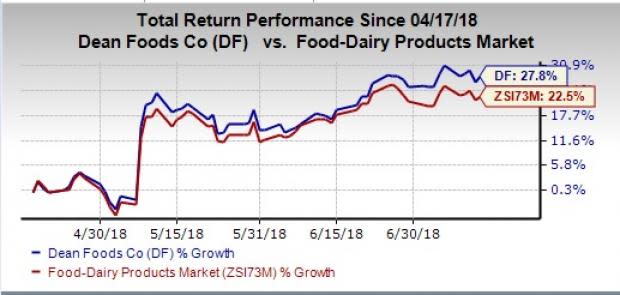

Dean Foods Company DF is likely to continue gaining from its cost-reduction initiatives, along with focus on core business as well as product diversification. While the company has been grappling with lower product volumes and loss of share in U.S. fluid milk volumes, strength of the aforementioned factors has helped this Zacks Rank #3 (Hold) stock to rally as much as 28% in the past three months. This also fares better than the industry’s growth of 22.5%.

Cost-Productivity, Portfolio Diversification: Major Strengths

Dean Foods remains committed toward boosting operational excellence via execution of the enterprise-wide cost productivity program, aimed at generating additional savings in 2018 and beyond. This productivity program mainly revolves around three major areas, namely enhancement of supply-chain network, optimization of spending across all key categories to ensure greater efficiency and integration of operating model along with minimization of general and administrative expenses. Notably, Dean Foods has completed the initial phase of reducing general and administrative expenses and is on track to start the next phase that focuses on rightsizing network to match volumes.

Further, the company continues to make efforts to achieve the lowest cost position in the industry. Under the OpEx 2020 cost productivity plan introduced in 2017, the company had targeted annual productivity of $80-$100 million. In 2018, the company expects to save more than this targeted range. Driven by these efforts, the total landed cost had decreased by more than $4 million year over year in the first quarter, even amid stronger-than-anticipated freight inflation.

Moving to efforts to strengthen portfolio, Dean Foods focuses on enhancing its core businesses as well as diversifying portfolio by moving beyond the pure milk products. While the company is on track with the growth of its core dairy-related business with products like ice cream, flavored milk and sour cream; it is also vouching for opportunities in foodservice and other beverages. Moreover, we applaud the company’s efforts to grow in the organic space, which is evident from its deals with Good Karma and Organic Valley Fresh milk brands, along with the acquisition of Uncle Matt's Organic juices.

What’s Hurting Dean Foods?

Dean Foods has long been grappling with lower product volumes and loss of share in U.S. fluid milk volumes, which have been largely impacting its top line. Although volume and mix results were in-line with the company’s expectations in first-quarter 2018, adjusted gross profit declined 4% year over year, mainly due to soft volume and greater mix of private label products. Further, adjusted operating income decreased 11.1% in the first quarter. For the second quarter, management anticipates reduction in volumes from two large customers.

Further, Dean Foods’ business remains heavily dependent on commodities such as raw milk, soybeans, diesel fuel and others, the prices of which often fluctuate. The company anticipates Class 1 raw milk costs to rise as it progresses into 2018, while it expects rates in the second half of the year to remain flat with the 2017 levels. We believe that adverse fluctuations in raw material prices pose threats to Dean Foods’ operating results.

Nevertheless, savings from management’s aggressive cost-productivity program are likely to cushion input inflation and volume deleverage throughout its operational phase. That said, we expect Dean Foods’ to sustain its solid run.

Check Out These Solid Food Stocks

MEDIFAST INC MED, a Zacks Rank #1 (Strong Buy) stock, has delivered positive earnings surprises in the past three quarters. You can see the complete list of today’s Zacks #1 Rank stocks here.

Lamb Weston Holdings LW, with long-term earnings per share growth rate of 12.2%, flaunts a Zacks Rank #2 (Buy).

B&G Foods BGS, with a Zacks Rank #2, delivered positive earnings surprise in the last reported quarter and has gained 31.5% in the past three months.

Wall Street’s Next Amazon

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Click for details >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dean Foods Company (DF) : Free Stock Analysis Report

MEDIFAST INC (MED) : Free Stock Analysis Report

Lamb Weston Holdings Inc. (LW) : Free Stock Analysis Report

To read this article on Zacks.com click here.