Yahoo Finance

Yahoo Finance DDH1 (ASX:DDH) Has Announced That It Will Be Increasing Its Dividend To A$0.0265

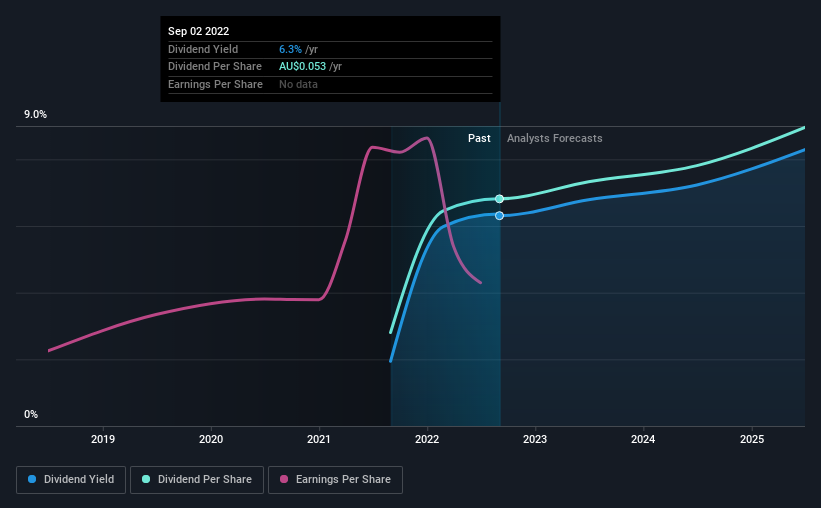

DDH1 Limited's (ASX:DDH) periodic dividend will be increasing on the 7th of October to A$0.0265, with investors receiving 22% more than last year's A$0.0218. Even though the dividend went up, the yield is still quite low at only 6.3%.

View our latest analysis for DDH1

DDH1's Dividend Is Well Covered By Earnings

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. Based on the last dividend, DDH1 is earning enough to cover the payment, but then it makes up 112% of cash flows. While the company may be more focused on returning cash to shareholders than growing the business at this time, we think that a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

Looking forward, earnings per share is forecast to rise by 85.3% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 39%, which is in the range that makes us comfortable with the sustainability of the dividend.

DDH1 Is Still Building Its Track Record

It's not possible for us to make a backward looking judgement just based on a short payment history. This doesn't mean that the company can't pay a good dividend, but just that we want to wait until it can prove itself.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. DDH1 has seen EPS rising for the last five years, at 12% per annum. The company is paying out a lot of its cash as a dividend, but it looks okay based on the payout ratio.

We should note that DDH1 has issued stock equal to 26% of shares outstanding. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

In Summary

Overall, we always like to see the dividend being raised, but we don't think DDH1 will make a great income stock. While DDH1 is earning enough to cover the payments, the cash flows are lacking. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 3 warning signs for DDH1 that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here