Yahoo Finance

Yahoo Finance This Dividend Stock Just Upped Its Payout 7.8% by Keeping It Simple

Atmos Energy (NYSE: ATO) is the product of more than 250 separate entities that slowly came together over a period of over 100 years. Major expansions occurred in 1987, with the purchase of Western Kentucky Gas, and in 2000 with the acquisition of Louisiana Gas Service and LGS Natural Gas from Citizens Utilities (now Frontier Communications).

Image source: Atmos Energy.

Today, Atmos has emerged as one of the largest regulated distributors of natural gas in the U.S., servicing well over 1,400 communities and 3 million customers. If this sounds like a simple business, that's because it is. And this simplicity has led to spectacular results for investors:

Its dividend, which currently yields 2.28%, has been steadily increased for 34 years.

Atmos shares increased over 140% over the past five years, and the company aims to return shareholders 8% to 10% per year over the long term. One of the ways the company plans to do this is by focusing on what it truly excels at: guaranteeing the timely delivery of natural gas for its customers.

Focused on strengths

Around two-thirds of Atmos customers are homes; 28% are businesses, and the balance industrial and "other" clients. The company services its clients through six individual operating utility divisions extending across eight states: Colorado-Kansas, West Texas, "Mid-Tex," Louisiana, Mississippi, and Kentucky/Mid-States.

Division | Service Areas | Communities Served | Customer Meters |

|---|---|---|---|

Mid-Tex | Texas, including the Dallas/Fort Worth metroplex | 550 | 1,672,581 |

Louisiana | Louisiana | 270 | 359,920 |

Kentucky/Mid-States | Kentucky, Tennessee, and Virginia | 230 | 353,411 |

West Texas | Amarillo, Lubbock, and Midland region | 80 | 311,188 |

Mississippi | Mississippi | 110 | 270,754 |

Colorado-Kansas | Colorado and Kansas | 170 | 253,551 |

Data source: Atmos Energy 10-K filing.

For financial reporting purposes, Atmos has three operating segments.

Its distribution segment (the largest) is a regulated natural gas distributor. Its pipeline and storage segment manages the midstream assets of the Atmos Pipeline-Texas subsidiary, as well as satellite gas transmission operations in Louisiana. The final segment was natural gas marketing; this division was sold to CenterPoint Energy in January 2017.

By selling its marketing division, the company is simplifying its business even further so that it can focus on being the best regulated natural gas distributor that it can be.

Being all it can be

The rates that Atmos charges its 3 million customers are set by the regulating body for the region in question -- typically the state in which a customer resides. These agreements, which guarantee the company a rate of return, are also non-exclusive -- another natural gas company could ride into town.

This may sound troubling, but the capital requirements of building natural gas infrastructure act as a barrier to entry. Also, as Atmos' natural gas rates are set by regulators, prices are set at levels that are beneficial for all stakeholders. States know that utilities need to make a profit, so Atmos gets a decent return on investment, and its customers are assured a steady flow of reasonably priced natural gas.

In fact, this way of doing business has worked out well for Atmos. The company regularly seeks with regulators to increase the prices it charges customers.

The following table shows Atmos Energy's regulated annual operating income increases over the past three years:

Rate Action | 2017 | 2016 | 2015 |

|---|---|---|---|

Annual formula rate mechanisms | $90.42 million | $114.97 million | $113.70 million |

Rate case filings | $12.96 million | $7.71 million | $711,000 |

Other rate-making activity | $784,000 | ($183,000) | $78,000 |

Total increase in operating income | $104.17 million | $122.50 million | $114.49 million |

Data source: Atmos Energy 10-K filing. Dollar figures are to the nearest thousand.

Ancillary business divisions can often be a distraction. By focusing on its regulated distribution business, Atmos ensures consistent profit growth. The only other factor that could hinder its plans to generate 8-10% annual returns is a consistent supply of natural gas. Fortunately, Atmos has this factor handled as well.

Ensuring commitments are met

So where does Atmos get its natural gas? The company noted in its recent 10-K filing that its gas comes from a wide variety of sources. These include independent producers, marketers, competitors, and even open-market purchases. This is meaningful for investors because it means Atmos doesn't rely on any one source to fulfill its obligations as a natural gas distributor.

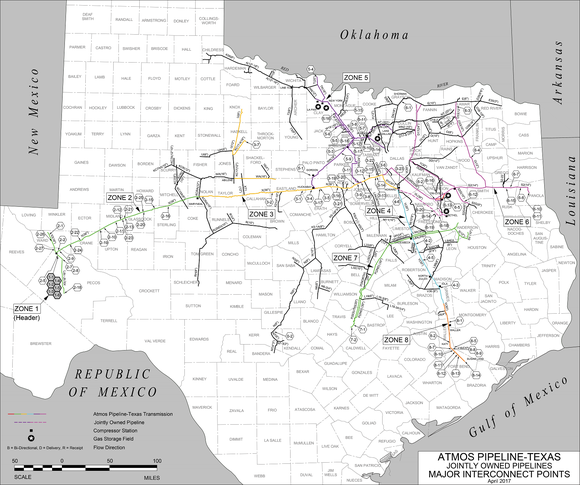

Lastly, it's worth noting that (as is often the case in the complex energy marketplace), Atmos often purchases natural gas from regions where it doesn't have the infrastructure necessary to get it to its customers. This is where its pipeline and storage segment comes in. One of the key tasks this segment handles is the management of agreements with 38 pipeline transportation companies. It purchases gas from far away, arranges to transport it, and then stores it.

The pipeline and storage segment is vital outside Texas. Atmos' Mid-Tex division relies on the company's flagship distribution asset, the Atmos Pipeline-Texas network:

Image source: Atmos Energy.

Atmos' recent results have been a continuation of the company's long history of steady growth.

Looking ahead, management expects earnings per share in fiscal year 2018 to fall between $3.75 and $3.95 per share. This modest growth is expected to allow an increase in the dividend next year, to $1.94 per share. Interested investors should note that this marks a 7.8% payout increase over the fiscal-year 2017 payout. In the fiscal-year 2017 conference call, CEO Mike Haefner noted that he and his team were targeting long-term annual growth in EPS of 6% to 8% per year.

Follow the "K.I.S.S." rule to dividend growth

Atmos Energy is a prime example of the "K.I.S.S." rule. An abbreviation for "Keep it simple, stupid!" widely espoused by everyone's favorite billionaire investor, Warren Buffett, the philosophy essentially boils down to keeping a business as simple as possible. The more complicated its operations, or even a product, the higher the likelihood that even the executives won't understand what's going on.

Atmos knows exactly what it is, and it knows exactly what it is doing. As one of the largest regulated natural gas distributors in the U.S., it needs to meet its supply agreements with its 3 million customers, and ensure a reasonable return to its investors. With over a century of investing in the assets necessary to ensure both these commitments are met, Atmos Energy isn't just a business success story, it's an intriguing stock for Foolish investors.

More From The Motley Fool

Sean O'Reilly owns shares of Atmos Energy. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.